Exam 11: Monopolistic Competition

Exam 1: Economics: Foundations and Models145 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System151 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply159 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes127 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods141 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply149 Questions

Exam 7: Comparative Advantage and the Gains From International Trade125 Questions

Exam 8: Consumer Choice and Behavioral Economics154 Questions

Exam 9: Technology, Production, and Costs169 Questions

Exam 10: Firms in Perfectly Competitive Markets153 Questions

Exam 11: Monopolistic Competition140 Questions

Exam 12: Oligopoly: Firms in Less Competitive Markets130 Questions

Exam 13: Monopoly and Antitrust Policy146 Questions

Exam 14: The Markets for Labour and Other Factors of Production149 Questions

Exam 15: Public Choice, Taxes, and the Distribution of Income134 Questions

Exam 16: Pricing Strategy132 Questions

Exam 17: Firms, the Stock Market, and Corporate Governance137 Questions

Select questions type

For a monopolistically competitive firm, marginal revenue

Free

(Multiple Choice)

4.8/5  (32)

(32)

Correct Answer: Verified

Verified

C

Is a monopolistically competitive firm allocatively efficient?

Free

(Multiple Choice)

4.9/5 (26)

Correct Answer:Verified

C

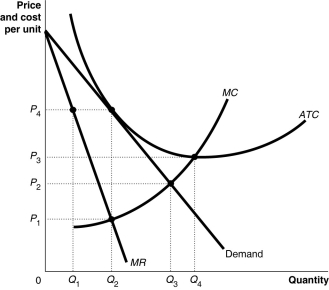

Figure 11.6

-Refer to Figure 11.6.What is the monopolistic competitor's profit maximizing output?

-Refer to Figure 11.6.What is the monopolistic competitor's profit maximizing output?

Free

(Multiple Choice)

4.9/5 (35)

Correct Answer:Verified

B

How does the long run equilibrium of a monopolistically competitive industry differ from that of a perfectly competitive industry?

(Multiple Choice)

4.8/5 (26)

A successful trademark is one that becomes a generic name for a product, for example, "Kleenex" has become a generic term for tissues.

(True/False)

4.9/5 (34)

If the demand curve for a firm is downward-sloping, its marginal revenue curve

(Multiple Choice)

4.7/5 (44)

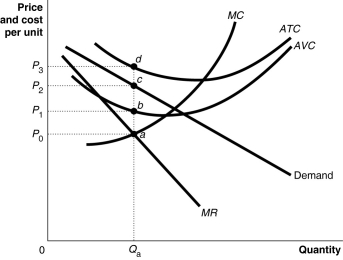

Figure 11.3

Figure 11.3 shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 11.3.What is the area that represents the total revenue made by the firm?

Figure 11.3 shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 11.3.What is the area that represents the total revenue made by the firm?

(Multiple Choice)

4.9/5 (41)

Unique to New Brunswick, Beausoleil oysters are known for their perfect, petite shells and are described by Rowan Jacobsen's Geography of Oysters as "ideal starter oysters, with the delightful yeasty aroma of Champagne or rising bread dough." Suppose the following table represents cost and revenue data for a New Brunswick oyster concern.

Dozen Oysters Sold per Day Price (P) Total Revenue (TR) Marginal Revenue (MR) Total Cost (TC) Marginal Cost (MC) Total Cost ( Profit 0 \ 15 \ 0 \@cdots \ 12 \ldots \ldots -\ 12 1 14 14 \ 14 18 \ 6 \ 18.00 -4 2 13 26 12 20 2 10.00 6 3 12 36 10 21 1 7.00 15 4 11 44 8 23 2 5.75 21 5 10 50 6 26 3 5.20 24 6 9 54 4 30 4 5.00 24 7 8 56 2 35 5 5.00 21 8 7 56 0 42 7 5.25 14 9 6 54 -2 52 10 5.78 2 10 5 50 -4 78 16 7.80 -28

Illustrate this data by graphing the demand, MR, MC, and ATC curves.Identify the profit-maximizing price and quantity, and show the area representing the total profit received.

(Essay)

4.9/5 (33)

A monopolistically competitive industry that earns economic profits in the short run will be able to expand its market share even if the market size remains constant.

(True/False)

4.9/5 (32)

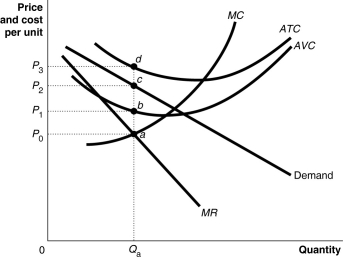

Figure 11.7

Figure 11.7 shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 11.7.If the diagram represents a typical firm in the designer watch market, what is likely to happen in the long run?

Figure 11.7 shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 11.7.If the diagram represents a typical firm in the designer watch market, what is likely to happen in the long run?

(Multiple Choice)

4.8/5 (43)

Which of the following characteristics is common to monopolistic competition and perfect competition?

(Multiple Choice)

4.9/5 (28)

If a monopolistically competitive firm breaks even, the firm

(Multiple Choice)

4.7/5 (37)

Table 11.3

Quantity Price (dollars) Total Revenue (dollars) Total Variable Cost (dollars) Total Cost (dollars) 0 \ 21 \ 0 \ 0 \ 50 1 20 20 16 66 2 19 38 31 81 3 18 54 45 95 4 17 68 59 109 5 16 80 75 125 6 15 90 93 143 7 14 98 112 162 8 13 104 140 190 9 12 108 180 230 10 11 110 230 280

Table 11.3 shows the demand and cost schedules for a monopolistically competitive firm.

-Refer to Table 11.3.If this firm continues to produce, what is likely to happen to the product's price in the long run?

(Multiple Choice)

5.0/5 (38)

Which of the following is true for a firm with a downward-sloping demand curve for its product?

(Multiple Choice)

4.7/5 (39)

Table 11.3

Quantity Price (dollars) Total Revenue (dollars) Total Variable Cost (dollars) Total Cost (dollars) 0 \ 21 \ 0 \ 0 \ 50 1 20 20 16 66 2 19 38 31 81 3 18 54 45 95 4 17 68 59 109 5 16 80 75 125 6 15 90 93 143 7 14 98 112 162 8 13 104 140 190 9 12 108 180 230 10 11 110 230 280

Table 11.3 shows the demand and cost schedules for a monopolistically competitive firm.

-Refer to Table 11.3.What are the profit-maximizing/loss-minimizing output level and price?

(Multiple Choice)

4.8/5 (36)

When a monopolistically competitive firm cuts its price to increase its sales, it experiences a loss in revenue due to the

(Multiple Choice)

4.9/5 (39)

Some of the advantages Netflix had over companies like Blockbuster and Wal-Mart in successfully competing in the mail order DVD rental business include all of the following except

(Multiple Choice)

4.8/5 (31)

Recent research has shown that the first firm to enter a market often does not have a long-term advantage over later entrants into the market.The textbook used which of the following examples to illustrate this?

(Multiple Choice)

4.8/5 (43)

If marginal revenue is negative then the revenue lost from receiving a lower price on all the units that could have been sold at the original price is smaller than the additional revenue from selling one more unit of the good.

(True/False)

4.8/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)