Exam 11: Systematic Risk and the Equity Risk Premium

Exam 1: Corporate Finance and the Financial Manager91 Questions

Exam 2: Introduction to Financial Statement Analysis122 Questions

Exam 3: The Valuation Principle: the Foundation of Financial Decision Making120 Questions

Exam 4: The Time Value of Money101 Questions

Exam 5: Interest Rates118 Questions

Exam 6: Bonds122 Questions

Exam 7: Valuing Stocks122 Questions

Exam 8: Investment Decision Rules137 Questions

Exam 9: Fundamentals of Capital Budgeting107 Questions

Exam 10: Risk and Return in Capital Markets101 Questions

Exam 11: Systematic Risk and the Equity Risk Premium102 Questions

Exam 12: Determining the Cost of Capital106 Questions

Exam 13: Risk and the Pricing of Options112 Questions

Exam 14: Raising Equity Capital104 Questions

Exam 15: Debt Financing109 Questions

Exam 16: Capital Structure113 Questions

Exam 17: Payout Policy101 Questions

Exam 18: Financial Modelling and Pro Forma Analysis124 Questions

Exam 19: Working Capital Management122 Questions

Exam 20: Short Term Financial Planning105 Questions

Exam 21: Risk Management108 Questions

Exam 22: International Corporate Finance108 Questions

Exam 23: Leasing86 Questions

Exam 24: Mergers and Acquisitions81 Questions

Exam 25: Corporate Governance52 Questions

Select questions type

Suppose you have $10,000 in cash to invest.You decide to sell short $5000 worth of Kinston stock and invest the proceeds from your short sale plus your $10,000 into one-year Treasury bills earning 5%.At the end of the year,you decide to liquidate your portfolio.Kinston Industries has the following realized returns:  The return on your portfolio is closest to:

The return on your portfolio is closest to:

Free

(Multiple Choice)

4.8/5  (30)

(30)

Correct Answer: Verified

Verified

C

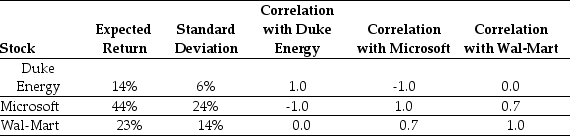

Use the table for the question(s) below.

Consider the following expected returns, volatilities, and correlations:

-The expected return of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

-The expected return of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

Free

(Multiple Choice)

4.8/5 (31)

Correct Answer:Verified

C

The Capital Asset Pricing Model asserts that the ________ return is equal to the risk-free rate plus a risk premium for systematic risk.

Free

(Multiple Choice)

4.7/5 (42)

Correct Answer:Verified

B

Suppose you buy 50 shares of RBC at $90 per share,and 70 shares of TD at $78 per share.If RBC's stock goes up to $94 per share and TD's stock falls to $72 per share,what is your portfolio return?

(Multiple Choice)

5.0/5 (38)

Use the information for the question(s) below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT) at $50 per share, 200 shares of Lowes (LOW) at $30 per share, and 100 shares of Ball Corporation (BLL) at $40 per share.

-The weight of Abbott Labs in your portfolio is:

(Multiple Choice)

4.8/5 (38)

RBC stock has a beta of 0.85,while TD stock has a beta of 1.21.The risk-free rate is 1.5%,and the expected return on a portfolio with 50% weight in RBC and the remainder in TD is 9.74%.What is the market risk premium?

(Multiple Choice)

4.8/5 (37)

Barrick Gold Corp stock has a beta of 2.1.If the risk-free rate is 2.6%,and expected market return is 9%,what is the expected return of Barrick Gold Corp stock,according to the CAPM?

(Multiple Choice)

4.9/5 (29)

A portfolio has three stocks - 300 shares of Yahoo (YHOO),300 Shares of General Motors (GM),and 100 shares of Standard and Poor's Index Fund (SPY).If the price of YHOO is $20,the price of GM is $30,and the price of SPY is $150,calculate the portfolio weight of YHOO and GM.

(Multiple Choice)

4.7/5 (32)

A stock market comprises 2000 shares of stock A and 2000 shares of stock B.The share prices for stocks A and B are $20 and $10,respectively.What proportion of the market portfolio is comprised of each stock?

(Multiple Choice)

4.8/5 (35)

If you build a large enough portfolio,you can diversify away all ________ risk,but you will be left with ________ risk.

(Multiple Choice)

4.9/5 (36)

When the returns of two stocks are negatively correlated,but not perfectly negatively correlated,then

(Multiple Choice)

4.8/5 (26)

CIBC stock has a beta of 1.2.If the risk-free rate is 1.8%,and the market risk premium is 6.5%,what is the expected return of CIBC stock,according to the CAPM?

(Multiple Choice)

4.9/5 (30)

For each 1% change in the market portfolio's excess return,the investment's excess return is expected to change by ________ percent due to risks that it has in common with the market.

(Multiple Choice)

4.8/5 (44)

Use the information for the question(s) below.

Suppose you have $10,000 in cash and you decide to borrow another $10,000 at a 6% interest rate to invest in the stock market. You invest the entire $20,000 in an exchange-traded fund (ETF) with a 12% expected return and a 20% volatility.

-The expected return on your of your investment is closest to:

(Multiple Choice)

4.8/5 (41)

If you build a large enough portfolio,you can diversify away all the risks of a portfolio.

(True/False)

4.8/5 (36)

What role does the correlation of two assets play in computation of the expected return of the two asset portfolio?

(Essay)

4.9/5 (33)

Stocks that have a higher volatility will always have a higher beta.

(True/False)

4.8/5 (36)

Your portfolio has 50% of its value invested in Bombardier and the remainder invested in Lululemon.Bombardier stock has a volatility of 25%,while Lululemon stock has a volatility of 10%.If the correlation between Bombardier and Lululemon is -0.1,what is the standard deviation of your portfolio?

(Multiple Choice)

4.8/5 (32)

Your portfolio contains $20,000 of Air Canada stock,which has a beta of 1.4,and $30,000 of WestJet stock,which has a beta of 1.8.What is the beta of your portfolio?

(Multiple Choice)

4.9/5 (25)

Blackberry stock has a beta of 1.7.If the risk-free rate is 2.1%,and the market risk premium is 7%,what is the expected return of Blackberry stock,according to the CAPM?

(Multiple Choice)

4.7/5 (27)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)