Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting

Exam 1: Economics: Foundations and Models234 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System258 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply242 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes208 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods263 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care171 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance264 Questions

Exam 9: Comparative Advantage and the Gains From International Trade188 Questions

Exam 10: Consumer Choice and Behavioral Economics300 Questions

Exam 11: Technology, Production, and Costs328 Questions

Exam 12: Firms in Perfectly Competitive Markets296 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting274 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets259 Questions

Exam 15: Monopoly and Antitrust Policy279 Questions

Exam 16: Pricing Strategy261 Questions

Exam 17: The Markets for Labor and Other Factors of Production281 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Select questions type

In the short run, a profit-maximizing firm's decision to produce should be guided by whether

(Multiple Choice)

4.8/5  (44)

(44)

A monopolistically competitive firm that earns economic profits in the short run will be able to expand its market share even if the market size remains constant.

(True/False)

4.9/5 (34)

Suppose a monopolistically competitive firm's output where marginal revenue equals marginal cost is 66 units and the price corresponding to this quantity is $18.If the average total cost at this output is $16.55, then its total profit is

(Multiple Choice)

4.8/5 (34)

The Jeans Store sells 7 pairs of jeans per day when it charges $100 per pair.It sells 8 pairs of jeans per day at a price of $90 per pair.The marginal revenue of the eighth pair of jeans is

(Multiple Choice)

4.8/5 (45)

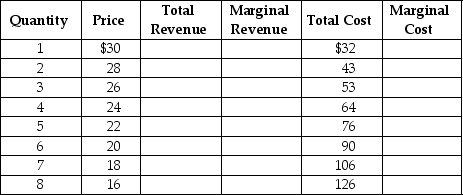

The table below shows the demand and cost data facing "Velvet Touches," a monopolistically competitive producer of velvet throw pillows.

Use the data to answer the following questions.

a.Complete the Total Revenue (TR), Marginal Revenue (MR), and Marginal Cost (MC)columns above.

b.What are the profit-maximizing price and quantity for Velvet Touches?

c.Is the firm making a profit or a loss? How much is the profit or loss? Show your work.

d.Is this firm operating in the long run or in the short run? Explain your answer.

e.If the firm's profit or loss is typical of all firms in the market for throw pillows, what is likely to happen in the future? Will there be more firms or will some existing firms leave the industry? Explain your answer.

f.What will happen to the typical firm's profit or loss after all entry/exit adjustments?

Use the data to answer the following questions.

a.Complete the Total Revenue (TR), Marginal Revenue (MR), and Marginal Cost (MC)columns above.

b.What are the profit-maximizing price and quantity for Velvet Touches?

c.Is the firm making a profit or a loss? How much is the profit or loss? Show your work.

d.Is this firm operating in the long run or in the short run? Explain your answer.

e.If the firm's profit or loss is typical of all firms in the market for throw pillows, what is likely to happen in the future? Will there be more firms or will some existing firms leave the industry? Explain your answer.

f.What will happen to the typical firm's profit or loss after all entry/exit adjustments?

(Essay)

4.8/5 (36)

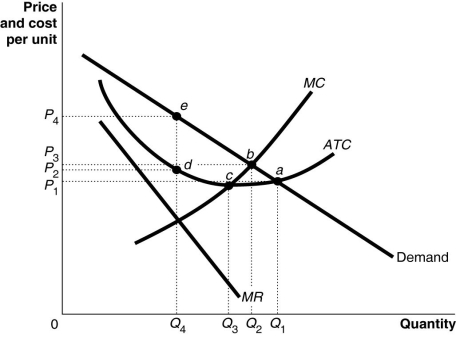

Figure 13-13

-Refer to Figure 13-13.If the diagram represents a typical firm in the market, what is likely to happen in the long run?

-Refer to Figure 13-13.If the diagram represents a typical firm in the market, what is likely to happen in the long run?

(Multiple Choice)

4.9/5 (39)

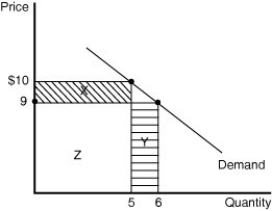

Figure 13-3

-Refer to Figure 13-3.What is the marginal revenue of the sixth unit of output?

-Refer to Figure 13-3.What is the marginal revenue of the sixth unit of output?

(Multiple Choice)

4.9/5 (33)

A major difference between monopolistic competition and perfect competition is

(Multiple Choice)

4.8/5 (39)

A monopolistically competitive firm should lower its price if its marginal revenue exceeds its marginal cost.

(True/False)

4.9/5 (37)

Which of the following characteristics is common to monopolistic competition and perfect competition?

(Multiple Choice)

4.9/5 (43)

Sparkle, one of many firms in the market for toothpaste, is in long-run equilibrium.Sparkle has a small market share and has been in business for a long time.

a.Identify the market structure in which Sparkle operates.Explain your answer.

b.What is Sparkle's profit or loss? Explain your answer.If you cannot determine the profit or loss, explain what information is missing.

c.Draw a diagram showing Sparkle's demand curve, marginal revenue curve, average total cost curve, and marginal cost curve.Label your diagram.

(Essay)

4.8/5 (29)

A monopolistically competitive firm that earns economic profits in the short run will face a more elastic demand curve in the long run.

(True/False)

4.9/5 (39)

Which of the following is the best example of a firm that competes in a monopolistically competitive market?

(Multiple Choice)

4.8/5 (38)

What is the difference between zero accounting profit and zero economic profit?

(Essay)

4.8/5 (40)

What is meant by "excess capacity"? How does it relate to consumer utility?

(Essay)

4.8/5 (43)

Although advertising raises the price of a monopolistic competitor's product, it does confer a benefit to consumers.Which of the following is a benefit to consumers?

(Multiple Choice)

4.9/5 (41)

The ability to engage in product differentiation is one of the factors a manager or owner of a firm can control in order to create value for consumers.

(True/False)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)