Exam 6: Audit Responsibilities and Objectives

Exam 1: The Demand for Audit and Other Assurance Services80 Questions

Exam 2: The CPA Profession101 Questions

Exam 3: Audit Reports170 Questions

Exam 4: Professional Ethics149 Questions

Exam 5: Legal Liability149 Questions

Exam 6: Audit Responsibilities and Objectives181 Questions

Exam 7: Audit Evidence166 Questions

Exam 8: Audit Planning and Materiality172 Questions

Exam 9: Assessing the Risk of Material Misstatement110 Questions

Exam 10: Fraud Auditing139 Questions

Exam 11: Internal Control and Coso Framework152 Questions

Exam 12: Assessing Control Risk and Reporting on Internal Controls104 Questions

Exam 13: Overall Audit Strategy and Audit Program119 Questions

Exam 14: Audit of the Sales and Collection Cycle: Tests of Controls140 Questions

Exam 15: Audit Sampling for Tests of Controls and Substantive Tests of Transactions151 Questions

Exam 16: Completing the Tests in the Sales and Collection Cycle: Accounts Receivable131 Questions

Exam 17: Audit Sampling for Tests of Details of Balances130 Questions

Exam 18: Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable146 Questions

Exam 19: Completing the Tests in the Acquisition and Payment Cycle: Verification of Selected Accounts128 Questions

Exam 20: Audit of the Payroll and Personnel Cycle130 Questions

Exam 21: Audit of the Inventory and Warehousing Cycle146 Questions

Exam 22: Audit of the Capital Acquisition and Repayment Cycle110 Questions

Exam 23: Audit of Cash and Financial Instruments146 Questions

Exam 24: Completing the Audit155 Questions

Exam 25: Other Assurance Services123 Questions

Exam 26: Internal and Governmental Financial Auditing and Operational Auditing98 Questions

Select questions type

The most important general ledger account included in and affecting several cycles is the

(Multiple Choice)

4.8/5  (38)

(38)

________ deals with potential overstatement and ________ deals with understatements (unrecorded transactions).

(Multiple Choice)

4.8/5 (30)

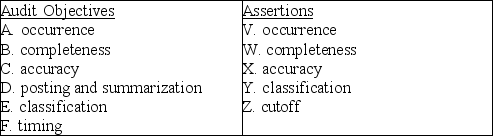

Below are five audit procedures, all of which are tests of transactions associated with the audit of the sales and collection cycle. Also, below are the six general transaction-related audit objectives and the five management assertions. For each audit procedure, indicate (1) its audit objective, and (2) the management assertion being tested.

1. Vouch recorded sales from the sales journal to the file of bills of lading.

(1) ________

(2) ________

2. Compare dates on the bill of lading, sales invoices, and sales journal to test for delays in recording sales transactions.

(1) ________

(2) ________

3. Account for the sequence of prenumbered bills of lading and sales invoices.

(1) ________

(2) ________

4. Trace from a sample of prelistings of cash receipts to the cash receipts journal, testing for names, amounts, and dates.

(1) ________

(2) ________

5. Examine customer order forms for credit approval by the credit manager.

(1) ________

(2) ________

1. Vouch recorded sales from the sales journal to the file of bills of lading.

(1) ________

(2) ________

2. Compare dates on the bill of lading, sales invoices, and sales journal to test for delays in recording sales transactions.

(1) ________

(2) ________

3. Account for the sequence of prenumbered bills of lading and sales invoices.

(1) ________

(2) ________

4. Trace from a sample of prelistings of cash receipts to the cash receipts journal, testing for names, amounts, and dates.

(1) ________

(2) ________

5. Examine customer order forms for credit approval by the credit manager.

(1) ________

(2) ________

(Short Answer)

4.8/5 (38)

The Sarbanes-Oxley Act requires the auditor to certify the quarterly and the annual financial statements required to be filed by publicly listed firms with the Securities and Exchange Commission.

(True/False)

4.8/5 (35)

For publicly listed companies, the auditor also issues which of the following reports in addition to a report containing the auditor's opinion?

(Multiple Choice)

4.8/5 (39)

Direct, written communication with the client's customers to identify whether a receivable exists is an example of a(n)

(Multiple Choice)

4.8/5 (30)

An audit generally provides no assurance that illegal acts that do not have a direct effect on the financial statements will be detected.

(True/False)

4.8/5 (37)

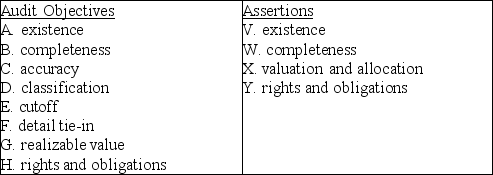

Below are five audit procedures, all of which are tests of balances associated with the audit of accounts receivable. Also, below are the eight general balance-related audit objectives and the four management assertions. For each audit procedure, indicate (1) its audit objective, and (2) the management assertion being tested.

1. Obtain an aged listing of accounts receivable. For a sample of individual customers on the listing, agree the customer's name, amount, and other information with the corresponding information in the accounts receivable master file.

(1) ________

(2) ________

2. Examine details of sales for five days before and five days after year-end to determine whether sales have been recorded in the proper period.

(1) ________

(2) ________

3. Assess the reasonableness of the balance in the allowance for doubtful accounts.

(1) ________

(2) ________

4. Inquire as to whether any accounts receivable have been factored or sold during the period.

(1) ________

(2) ________

5. Inquire as to whether there are any receivables from related parties.

(1) ________

(2) ________

1. Obtain an aged listing of accounts receivable. For a sample of individual customers on the listing, agree the customer's name, amount, and other information with the corresponding information in the accounts receivable master file.

(1) ________

(2) ________

2. Examine details of sales for five days before and five days after year-end to determine whether sales have been recorded in the proper period.

(1) ________

(2) ________

3. Assess the reasonableness of the balance in the allowance for doubtful accounts.

(1) ________

(2) ________

4. Inquire as to whether any accounts receivable have been factored or sold during the period.

(1) ________

(2) ________

5. Inquire as to whether there are any receivables from related parties.

(1) ________

(2) ________

(Short Answer)

4.9/5 (35)

Other than inquiring of management about policies they have established to prevent illegal acts and whether management knows of any laws or regulations that the company has violated, the auditor should not search for illegal acts that do not have a direct effect on the financial statements unless there is reason to believe they may exist.

(True/False)

4.8/5 (35)

It is not difficult for the auditor to quantify a measure of materiality while performing the audit.

(True/False)

4.7/5 (38)

The annual reports of many public companies include a statement about management's responsibilities and relationship with the CPA firm.

(True/False)

4.9/5 (30)

Which of the following statements is true of a public company's financial statements?

(Multiple Choice)

4.9/5 (37)

The profession has developed professional judgment frameworks that illustrate an effective decision-making process.

(True/False)

4.8/5 (38)

Management makes the following assertions about account balances:

(Multiple Choice)

4.8/5 (30)

Which of the following management assertions is not associated with classes of transactions and events?

(Multiple Choice)

4.8/5 (30)

The presentation and disclosure-related audit objectives are identical to the management assertions for presentation and disclosure.

(True/False)

4.8/5 (39)

Rights and obligations are the only balance-related assertion without a similar transaction-related assertion.

(True/False)

5.0/5 (26)

When developing the audit objectives, the first step is to divide the financial statements into cycles.

(True/False)

4.8/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)