Exam 17: Audit Sampling for Tests of Details of Balances

Exam 1: The Demand for Audit and Other Assurance Services80 Questions

Exam 2: The CPA Profession101 Questions

Exam 3: Audit Reports170 Questions

Exam 4: Professional Ethics149 Questions

Exam 5: Legal Liability149 Questions

Exam 6: Audit Responsibilities and Objectives181 Questions

Exam 7: Audit Evidence166 Questions

Exam 8: Audit Planning and Materiality172 Questions

Exam 9: Assessing the Risk of Material Misstatement110 Questions

Exam 10: Fraud Auditing139 Questions

Exam 11: Internal Control and Coso Framework152 Questions

Exam 12: Assessing Control Risk and Reporting on Internal Controls104 Questions

Exam 13: Overall Audit Strategy and Audit Program119 Questions

Exam 14: Audit of the Sales and Collection Cycle: Tests of Controls140 Questions

Exam 15: Audit Sampling for Tests of Controls and Substantive Tests of Transactions151 Questions

Exam 16: Completing the Tests in the Sales and Collection Cycle: Accounts Receivable131 Questions

Exam 17: Audit Sampling for Tests of Details of Balances130 Questions

Exam 18: Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable146 Questions

Exam 19: Completing the Tests in the Acquisition and Payment Cycle: Verification of Selected Accounts128 Questions

Exam 20: Audit of the Payroll and Personnel Cycle130 Questions

Exam 21: Audit of the Inventory and Warehousing Cycle146 Questions

Exam 22: Audit of the Capital Acquisition and Repayment Cycle110 Questions

Exam 23: Audit of Cash and Financial Instruments146 Questions

Exam 24: Completing the Audit155 Questions

Exam 25: Other Assurance Services123 Questions

Exam 26: Internal and Governmental Financial Auditing and Operational Auditing98 Questions

Select questions type

MUS has the statistical simplicity of attributes sampling, yet provides a statistical result expressed as a percentage.

(True/False)

4.8/5  (29)

(29)

When the sample selection is done using probability proportional to size sample selection (PPS),

(Multiple Choice)

4.8/5 (38)

The method used to measure the estimated total misstatement amount in a population when there is both a recorded value and an audited value for each item in the sample is

(Multiple Choice)

4.7/5 (39)

Calculating the sample size using monetary unit sampling depends on which of the following factors?

(Multiple Choice)

4.7/5 (31)

If an auditor desires a greater level of assurance in auditing a balance, the acceptable risk of incorrect acceptance

(Multiple Choice)

4.9/5 (37)

Which of the following does not have to be considered in determining the initial sample size of a test of details?

(Multiple Choice)

4.7/5 (32)

The auditor is concerned with the audited value rather than the misstatement amount of each item in the sample when using

(Multiple Choice)

5.0/5 (36)

To address sampling risk, auditors can use either nonstatistical or statistical methods for tests of controls, substantive tests of transactions, and test of details of balances.

(True/False)

4.9/5 (35)

Which of the following conditions would lead to a larger sample size?

(Multiple Choice)

4.8/5 (31)

Which of the following is not a problem with monetary unit selection?

(Multiple Choice)

4.8/5 (43)

To determine the sampling interval, the population is divided by the confidence factor.

(True/False)

4.8/5 (37)

The final step in the evaluation of the audit results is the decision to

(Multiple Choice)

4.8/5 (30)

As the amount of misstatements expected in the population approaches tolerable misstatement, the planned sample size will

(Multiple Choice)

4.8/5 (43)

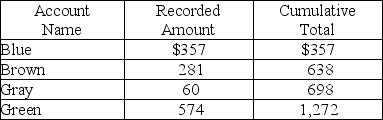

An accounts receivable population contains a total of four customers. The accounts, the amounts, and the cumulative total are shown below. Monetary unit sampling is to be used.  Based on the information above, the population size is

Based on the information above, the population size is

(Multiple Choice)

4.7/5 (35)

If the misstatement bound exceeds tolerable misstatement, the population is considered acceptable.

(True/False)

4.9/5 (35)

Tests for rates of occurrence are appropriately used in all but which of the following situations?

(Multiple Choice)

4.8/5 (38)

The auditor's principal objective when using a sample of tests of details of balances is whether the

(Multiple Choice)

4.7/5 (38)

In monetary unit sampling, the relationship between tolerable misstatement size and required sample size is

(Multiple Choice)

4.8/5 (37)

If no exceptions were found in the substantive tests of transactions,

(Multiple Choice)

4.9/5 (42)

The acceptable risk of incorrect rejection is important only when there is a ________ cost to increasing the sample size.

(Multiple Choice)

4.7/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)