Exam 11: Audit Sampling Part Four: Completion and Communication

Exam 1: Assurance and Auditing: An Overview47 Questions

Exam 2: The Structure of the Profession17 Questions

Exam 3: Ethics, Independence and Corporate Governance40 Questions

Exam 4: The Legal Liability of Auditors Part Two: Planning and Risk24 Questions

Exam 5: Overview of Elements of the Financial Report Audit Process72 Questions

Exam 6: Planning, Understanding the Entity and Evaluating Business Risk44 Questions

Exam 7: Assessing Specific Business Risk29 Questions

Exam 8: Understanding and Assessing Internal Control Part Three: Tests of Control and Tests of Details79 Questions

Exam 9: Tests of Controls59 Questions

Exam 10: Substantive Tests of Transactions and Balances84 Questions

Exam 11: Audit Sampling Part Four: Completion and Communication65 Questions

Exam 12: Completion and Review29 Questions

Exam 13: The Auditors Reporting Obligations Part Five: Other Assurance Services57 Questions

Exam 14: Internal Auditing25 Questions

Exam 15: Auditing and Assurance Services in the Public Sector21 Questions

Exam 16: Other Assurance Services and Advanced Topics40 Questions

Select questions type

How would decreases in tolerable misstatement and assessed level of control risk affect the sample size in a substantive test of details?

Free

(Multiple Choice)

4.7/5  (38)

(38)

Correct Answer: Verified

Verified

D

An auditor is planning the confirmation of accounts receivable. The total of debit balances in the aged trial balance of receivables is $2 million. The auditor has decided that the tolerable misstatement (basic precision) for this sampling application is $50 000, the risk of incorrect acceptance is five per cent and zero error is expected. There are 2500 customer balances. The auditor has the following statistical tables available. The auditor decides to use dollar-unit sampling.(Use the following table to determine your answer.) Number of risk of incorrect acceptance:

The auditor's estimated sample size is approximately:

The auditor's estimated sample size is approximately:

Free

(Multiple Choice)

4.8/5 (40)

Correct Answer:Verified

A

An advantage of using statistical sampling techniques is that such techniques:

Free

(Multiple Choice)

4.8/5 (35)

Correct Answer:Verified

D

An auditor plans to examine the supporting documentation for a sample of 20 payments as prescribed by the client's internal control procedures. For one of the payments in the chosen sample of 20, the supporting documentation cannot be found. The auditor should:

(Multiple Choice)

4.7/5 (39)

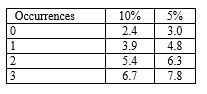

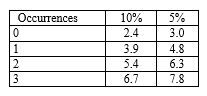

An auditor uses sampling tables to determine planned sample size for a test of controls. If they specify a risk of assessing control risk too low of five per cent and a tolerable deviation rate of six per cent and expects no deviations, the planned sample size should be: (Use the following table to determine your answer.)

Number of factors for sampling risks of:

(Multiple Choice)

4.9/5 (40)

The auditor has decided to use systematic selection of cash payments when testing the control that cheque payments are supported by a supplier's invoice, a purchase requisition and a goods received note. Each cheque comprises a sampling unit. There are 5000 cheques drawn (numbered 1-5000) and the total amount of cash payments is $10 million. The sample size is 20 and the random start is 127. Given this information, the sample interval is:

(Multiple Choice)

4.8/5 (35)

If the size of the sample to be used in a particular test of controls has not been determined by utilising statistical concepts, but the sample has been chosen in accordance with random selection procedures:

(Multiple Choice)

4.9/5 (39)

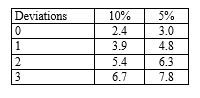

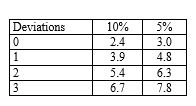

If an auditor is evaluating a sample for a test of controls of 50 items and specifies a risk of assessing control risk too low of five per cent and finds one deviation, the approximate achieved maximum deviation rate, (rounded to the nearest one per cent) is: (Use the following table to determine your answer.)

Number of factors for sampling risks of:

(Multiple Choice)

4.9/5 (27)

Which of the following best describes the distinguishing feature of statistical sampling compared with non-statistical sampling?

(Multiple Choice)

4.9/5 (39)

Using statistical sampling to assist in verifying the year-end accounts payable balance, an auditor has accumulated the following data:

Using the ratio estimation technique, the auditor's estimate of the year-end accounts payable balance would be:

Using the ratio estimation technique, the auditor's estimate of the year-end accounts payable balance would be:

(Multiple Choice)

4.9/5 (33)

Using statistical sampling to assist in verifying the year-end accounts payable balance, an auditor has accumulated the following data:

Using the ratio estimation technique, the auditor's estimate of the year-end accounts payable balance would be:

Using the ratio estimation technique, the auditor's estimate of the year-end accounts payable balance would be:

(Multiple Choice)

4.9/5 (32)

The auditor has decided to use systematic selection of cash payments when testing the control that cheque payments are supported by a supplier's invoice, a purchase requisition and a goods received note. Each cheque comprises a sampling unit. There are 5000 cheques drawn (numbered 1-5000) and the total amount of cash payments is $10 million. The sample size is 20 and the random start is 127. Given this information, the second item selected will be item no:

(Multiple Choice)

4.9/5 (40)

When planning a sample for a substantive test of balances, an auditor should consider tolerable misstatement for the sample.This consideration should:

(Multiple Choice)

4.8/5 (32)

An auditor is planning the confirmation of accounts receivable. The total of debit balances in the aged trial balance of receivables is $2 million. The auditor has decided that the tolerable misstatement (basic precision) for this sampling application is $50 000, the risk of incorrect acceptance is five per cent and zero error is expected. There are 2500 customer balances. The auditor has the following statistical tables available. The auditor decides to use dollar-unit sampling.Number of risk of incorrect acceptance:  Assume a sample size of 100. The sampling interval for dollar-unit sampling using the systematic selection method

Is approximately:

Assume a sample size of 100. The sampling interval for dollar-unit sampling using the systematic selection method

Is approximately:

(Multiple Choice)

4.9/5 (39)

An auditor selecting a sample may use any of the following methods except:

(Multiple Choice)

4.7/5 (44)

Which of the following factors does an auditor generally most need to consider in planning a particular audit sample for a test of controls?

(Multiple Choice)

4.9/5 (32)

Which of the following best illustrates the concept of sampling risk?

(Multiple Choice)

4.8/5 (40)

In determining the sample size for a test of controls, an auditor should consider the likely rate of deviations, desired confidence level and the:

(Multiple Choice)

4.8/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)