Exam 11: Audit Sampling Part Four: Completion and Communication

Exam 1: Assurance and Auditing: An Overview47 Questions

Exam 2: The Structure of the Profession17 Questions

Exam 3: Ethics, Independence and Corporate Governance40 Questions

Exam 4: The Legal Liability of Auditors Part Two: Planning and Risk24 Questions

Exam 5: Overview of Elements of the Financial Report Audit Process72 Questions

Exam 6: Planning, Understanding the Entity and Evaluating Business Risk44 Questions

Exam 7: Assessing Specific Business Risk29 Questions

Exam 8: Understanding and Assessing Internal Control Part Three: Tests of Control and Tests of Details79 Questions

Exam 9: Tests of Controls59 Questions

Exam 10: Substantive Tests of Transactions and Balances84 Questions

Exam 11: Audit Sampling Part Four: Completion and Communication65 Questions

Exam 12: Completion and Review29 Questions

Exam 13: The Auditors Reporting Obligations Part Five: Other Assurance Services57 Questions

Exam 14: Internal Auditing25 Questions

Exam 15: Auditing and Assurance Services in the Public Sector21 Questions

Exam 16: Other Assurance Services and Advanced Topics40 Questions

Select questions type

Which of the following is appropriate in the selection of a statistical sample?

(Multiple Choice)

4.9/5  (32)

(32)

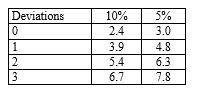

An auditor planning tests of controls specifies a risk of assessing control risk too low of five per cent and a tolerable deviation rate of six per cent and expects one deviation. For these specifications, the planned sample size should be: (Use the following table to determine your answer.)

Number of factors for sampling risks of:

(Multiple Choice)

4.8/5 (35)

The accounting department reports that the balance of accounts receivable is $210 000. You are willing to accept that balance if it is within $15 000 of the actual balance. Using a variables sampling plan, you compute a 95 per cent confidence interval of $208 000 to $225 000. You would therefore:

(Multiple Choice)

4.8/5 (38)

Based on a five per cent risk of assessing control risk too low, how would an auditor interpret a computed upper deviation rate of seven per cent?

(Multiple Choice)

4.8/5 (30)

An auditor is planning the confirmation of accounts receivable. The total of debit balances in the aged trial balance of receivables is $4 million. The auditor has decided that the tolerable misstatement (basic precision) for this sampling application is $50 000, the risk of incorrect acceptance is five per cent and zero error is expected. There are 2500 customer balances. The auditor decides to use dollar-unit sampling and determines a sample size of 100. The sampling interval for dollar-unit sampling using the systematic selection method is approximately:

(Multiple Choice)

4.9/5 (46)

When selecting items for testing, the auditor concentrates their selection on high dollar value items. This approach is:

(Multiple Choice)

4.8/5 (42)

Dollar-unit sampling is said to eliminate the need to stratify the sample because:

(Multiple Choice)

4.8/5 (27)

All of the following are true for dollar-unit sampling except:

(Multiple Choice)

4.8/5 (30)

As a result of tests of controls, an auditor found that they had assessed control risk as too low (their planned reliance on internal control was too high). This assessment occurred because the deviation rate in the sample was:

(Multiple Choice)

4.8/5 (34)

Which of the following would be an improper technique when using statistical sampling in an audit of accounts receivable?

(Multiple Choice)

4.8/5 (45)

The tolerable deviation rate for a test of controls is generally:

(Multiple Choice)

4.9/5 (30)

An auditor is preparing to sample a client's customer receivables for overstatement. A statistical sampling method that automatically provides stratification when using systematic selection (in that all items greater than the sample interval will be selected) is:

(Multiple Choice)

4.9/5 (34)

An advantage of using statistical over non-statistical sampling methods in tests of controls is that the statistical methods:

(Multiple Choice)

4.9/5 (40)

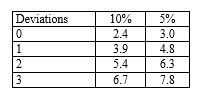

An auditor planning tests of controls specifies a risk of assessing control risk too low of 10 per cent and a tolerable deviation rate of six per cent and expects no deviations. For these specifications, the planned sample size should be: (Use the following table to determine your answer.)

Number of factors for sampling risks of:

(Multiple Choice)

4.8/5 (33)

In assessing sampling risk, the risk of incorrect rejection and the risk of assessing control risk too high relate to the:

(Multiple Choice)

4.9/5 (36)

The tolerable deviation rate for tests of controls necessary to justify assessing control risk at less than maximum depends primarily on which of the following?

(Multiple Choice)

4.8/5 (30)

Sarah Jones, an auditor, believes the industry-wide occurrence rate of client billing errors is three per cent and has established a tolerable deviation rate of five per cent. In the review of client invoices to test that the invoice is properly checked and authorised, Jones should use:

(Multiple Choice)

4.8/5 (39)

Which of the following best illustrates the concept of sampling risk?

(Multiple Choice)

4.9/5 (34)

How would increases in tolerable misstatement and assessed level of control risk affect the sample size in a substantive test of details?

(Multiple Choice)

4.8/5 (34)

Which of the following sampling methods would be used to estimate a numerical measurement of a population, such as a dollar value?

(Multiple Choice)

4.8/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)