Exam 11: Audit Sampling Part Four: Completion and Communication

Exam 1: Assurance and Auditing: An Overview47 Questions

Exam 2: The Structure of the Profession17 Questions

Exam 3: Ethics, Independence and Corporate Governance40 Questions

Exam 4: The Legal Liability of Auditors Part Two: Planning and Risk24 Questions

Exam 5: Overview of Elements of the Financial Report Audit Process72 Questions

Exam 6: Planning, Understanding the Entity and Evaluating Business Risk44 Questions

Exam 7: Assessing Specific Business Risk29 Questions

Exam 8: Understanding and Assessing Internal Control Part Three: Tests of Control and Tests of Details79 Questions

Exam 9: Tests of Controls59 Questions

Exam 10: Substantive Tests of Transactions and Balances84 Questions

Exam 11: Audit Sampling Part Four: Completion and Communication65 Questions

Exam 12: Completion and Review29 Questions

Exam 13: The Auditors Reporting Obligations Part Five: Other Assurance Services57 Questions

Exam 14: Internal Auditing25 Questions

Exam 15: Auditing and Assurance Services in the Public Sector21 Questions

Exam 16: Other Assurance Services and Advanced Topics40 Questions

Select questions type

Which of the following is a distinguishing feature between statistical sampling and non-statistical sampling?

(Multiple Choice)

4.9/5  (39)

(39)

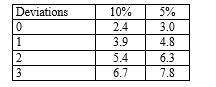

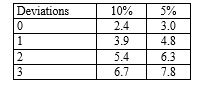

If an auditor is evaluating a sample for a test of controls of 50 items and specifies a risk of assessing control risk too low of 10 per cent and finds two deviations, the approximate maximum deviation rate (rounded to the nearest one per cent) is: (Use the following table to determine your answer.)

Number of factors for sampling risks of:

(Multiple Choice)

4.9/5 (43)

An underlying feature of random selection of items is that each:

(Multiple Choice)

4.8/5 (36)

An auditor planning tests of controls specifies a risk of assessing control risk too low of 10 per cent and a tolerable deviation rate of eight per cent and expects one deviation. For these specifications, the planned sample size should be in which range: (Use the following table to determine your answer.)

Number of factors for sampling risks of:

(Multiple Choice)

4.8/5 (33)

Stratified sampling is a statistical technique that may be more efficient than unstratified sampling because it usually:

(Multiple Choice)

4.9/5 (32)

When performing a test of controls with respect to control over cash disbursements, an auditor may use a systematic sampling technique with a start at any randomly selected item. The biggest disadvantage of this type of sampling is that the items in the population:

(Multiple Choice)

4.9/5 (40)

An account balance is $300 000 and there are 80 items in the account, six of which have balances that equal or exceed $15 000. The auditor plans to use a dollar-unit sampling plan with systematic sample selection. To ensure that all accounts with balances of at least $15 000 are selected, the sampling interval should be:

(Multiple Choice)

4.8/5 (42)

An auditor is using the probability proportional to size selection method. Using this method, the chance of selecting a $100 account balance compared to selecting a $500 account balance is:

(Multiple Choice)

4.8/5 (40)

Sam Shoe, an auditor, is planning substantive tests of additions to property. There are 75 additions and he plans to vouch all those over $10 000, of which there are 15 and apply analytical tests to the remaining balance. The audit approach may be described most precisely as:

(Multiple Choice)

4.8/5 (38)

A sample selection procedure that is beneficial for helping ensure that items are continuously sampled over the period of interest is:

(Multiple Choice)

4.8/5 (34)

The auditor selects all items above $10 000, which comprise 10 per cent of the items in the population and tests 100 per cent of these items. The auditor does not test items below $10 000. The misstatements found in audit testing total $20 000. Which of the following statements is false?

(Multiple Choice)

4.8/5 (31)

An auditor selects a sample of 50 for a test of controls and finds two transactions are not processed in accordance with the controls. The tolerable deviation rate was specified as six per cent. Using the extrapolation approach specified in the auditing standards, the sample results:

(Multiple Choice)

4.8/5 (39)

When performing a test of controls with respect to control over cash receipts, an auditor may use a systematic sampling technique with a start at any randomly selected item. The biggest disadvantage of this type of sampling is that the items in the population:

(Multiple Choice)

4.7/5 (30)

Joe Costa, an auditor, is planning tests of controls over cash receipts. There are 7000 receipts and he plans to vouch 30 picked haphazardly from the cash receipts journal for the period 1 January to 30 September 20X0. This audit approach may be described most precisely as:

(Multiple Choice)

4.8/5 (43)

If auditors conducting attribute sampling found that the client deviated from a prescribed control in six of the first 10 items examined, the auditor is most likely to:

(Multiple Choice)

4.8/5 (31)

Alicia Wong, an auditor, is planning confirmation of accounts receivable. There are 500 customer balances and based on the condition of the accounting records and her past experience with the client, she plans to send 50 confirmation requests to customers she selected from the aged trial balance of accounts receivable. Alicia plans to evaluate confirmation responses qualitatively and by multiplying the average error in the 50 responses by 500. This audit approach may be described most precisely as:

(Multiple Choice)

4.9/5 (39)

For dollar-unit sampling, the number of individual accounts tested is:

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)