Exam 15: Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

Exam 1: Cost Management and Strategy79 Questions

Exam 2: Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map70 Questions

Exam 3: Basic Cost Management Concepts98 Questions

Exam 4: Job Costing118 Questions

Exam 5: Activity-Based Costing and Customer Profitability Analysis149 Questions

Exam 6: Process Costing106 Questions

Exam 7: Cost Allocation: Departments, Joint Products, and By-Products96 Questions

Exam 8: Cost Estimation120 Questions

Exam 9: Short-Term Profit Planning: Cost-Volume-Profit CVP Analysis105 Questions

Exam 10: Strategy and the Master Budget146 Questions

Exam 11: Decision Making With a Strategic Emphasis137 Questions

Exam 12: Strategy and the Analysis of Capital Investments167 Questions

Exam 13: Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing94 Questions

Exam 14: Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures178 Questions

Exam 15: Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management167 Questions

Exam 16: Operational Performance Measurement: Further Analysis of Productivity and Sales134 Questions

Exam 17: The Management and Control of Quality146 Questions

Exam 18: Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard130 Questions

Exam 19: Strategic Performance Measurement: Investment Centers and Transfer Pricing151 Questions

Exam 20: Management Compensation, Business Analysis, and Business Valuation108 Questions

Select questions type

Megan, Inc. uses the following standard costs per unit for one of its products: Direct labor (2.0 hrs. @ $5.00/hr.) = $10.00; overhead (2.0 hrs. @ $2.50/hr.) = $5.00. The flexible budget for overhead is $120,000 plus $1.00 per direct labor hour (DLH). Actual data for the past month show total overhead costs of $225,000, total fixed overhead of $123,000, 85,000 hours worked, and 40,000 units produced.

The fixed overhead production volume variance for Megan, Inc. for the past month (to the nearest whole dollar) was:

(Multiple Choice)

4.9/5  (33)

(33)

A standard costing system will produce the same income as an actual costing system when end-of-period standard cost variances are assigned:

(Multiple Choice)

4.7/5 (27)

Dillard, Inc., has developed the following standard cost data based on a denominator volume of 60,000 direct labor hours (DLHs). Budgeted fixed overhead is $360,000 and budgeted variable overhead is $180,000 at this level of activity. Required:

Determine (to the nearest dollar each) all variances for direct materials, direct labor, and factory overhead. Use a 4-variance breakdown (decomposition) of the total overhead variance for the period. Assume that the direct materials price variance is calculated at point of production, not point of purchase. Note: this problem requires knowledge from Chapter 14.

Required:

Determine (to the nearest dollar each) all variances for direct materials, direct labor, and factory overhead. Use a 4-variance breakdown (decomposition) of the total overhead variance for the period. Assume that the direct materials price variance is calculated at point of production, not point of purchase. Note: this problem requires knowledge from Chapter 14.

(Essay)

4.8/5 (33)

Zero Company's standard factory overhead application rate is $3.75 per direct labor hour (DLH), calculated at 90% capacity = 900 standard DLHs. In December, the company operated at 80% of capacity, or 800 standard DLHs. Budgeted factory overhead at 80% of capacity is $3,150, of which $1,350 is fixed overhead. For December, the actual factory overhead cost incurred was $3,800 for 840 actual DLHs, of which $1,300 was for fixed factory overhead.

If Zero Company uses a two-way breakdown (decomposition) of the total overhead variance, what is the total factory overhead flexible-budget variance for December (to the nearest whole dollar)?

(Multiple Choice)

4.9/5 (39)

The following budget data pertain to the Machining Department of Yolkenverst Co.: The company prepared the budget at 85% of the maximum capacity level. The department uses machine hours as the basis for applying standard factory overhead costs to production (outputs).

The standard fixed overhead application rate for the Machining Department (to two decimal places) is:

The company prepared the budget at 85% of the maximum capacity level. The department uses machine hours as the basis for applying standard factory overhead costs to production (outputs).

The standard fixed overhead application rate for the Machining Department (to two decimal places) is:

(Multiple Choice)

4.8/5 (32)

The following information for the past year is available from Thinnews Co., a company that uses machine hours to apply standard factory overhead cost to outputs: Actual total factory overhead cost incurred \ 24,000 Actual fixed overhead cost incurred \ 10,000 Budgeted fixed overhead cost \ 11,000 Actual machine hours 5,000 Standard machine hours allowed for the units manufactured 4,800 Denominator volume-machine hours 5,500 Standard variable overhead rate per machine hour \ 3.00 Under a two-variance breakdown (decomposition) of the total factory overhead variance, the fixed overhead production volume variance, to the nearest whole dollar, is:

(Multiple Choice)

4.8/5 (35)

Neptune Inc. uses a standard cost system and has the following information for the most recent month, April: Actual direct labor hours (DLHs) worked 17,000 Standard DLHs allowed for good output produced this period 18,000 Actual total factory overhead costs incurred \ 45,400 Budgeted fixed factory overhead costs \ 10,800 Denominator activity level, in direct labor hours (DLHs) 15,000 Total factory overhead application rate per standard DLH \ 2.70 The total factory overhead spending variance in April for Neptune, Inc., to the nearest whole dollar, was:

(Multiple Choice)

4.8/5 (43)

Management is currently deciding whether to investigate a cost variance that was identified by the accounting system. To help address this question, you have generated the following data:

Possible States of Nature:

1. The underlying operation is in control (i.e., is operating normally).

2. The underlying operation is out of control (and therefore is in need of an intervention)

Possible Decisions/Courses of Action:

1. Investigate the variance (to determine its underlying cause(s)).

2. Do not investigate the variance.

Estimated Costs and Probabilities:

1. Cost of investigating the variance = I = $1,500.

2. Cost of correcting an out-of-control process (if the process is found to be out of control) = C = $6,000.

3. Losses from not correcting an out-of-control process = L = $50,000.

4. Probability, p, of the process being out of control = 15%

Required:

1. Given the above information, what is the expected value of investigating the reported variance? (Show calculation, and round answer to nearest whole dollar.)

2. Prepare a payoff table that summarizes the states of nature (i.e., possible outcomes) and the decision alternatives (i.e., management actions). Your table should include cells for combinations of management actions and states of nature, plus cells to represent the expected value of each management action. Which decision is recommended based on information in your payoff table?

3. Given the above information, what is the probability level, p, for an out-of-control process (i.e., a nonrandom variance) that would make management indifferent between investigating and not investigating the variance? Round your answer to four (4) decimal places, e.g., 0.0456134 = 0.0456.

a. In what sense can this probability be considered a breakeven probability? (Demonstrate this by calculating the expected value of each management action, based on the break-even probability, p, you calculated.) Round final answers to the nearest whole numbers.

b. What is the correct management action if the probability of an out-of-control process is greater than the break-even probability, p? Show all calculations.

(Essay)

4.9/5 (36)

Which of the following statement is true regarding choice of the denominator volume level in conjunction with the process of allocating fixed manufacturing costs to production?

(Multiple Choice)

4.9/5 (33)

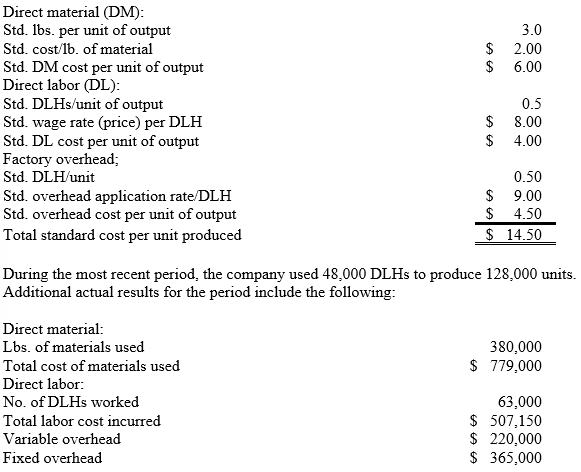

ABN Corp. has the following information about its standards and production activity in May: Required:

Calculate and show underlying calculations for each of the following variances:

1. Variable overhead flexible-budget (FB) variance, to the nearest whole dollar.

2. Fixed overhead spending variance, to the nearest whole dollar.

3. Fixed overhead production volume variance, to the nearest whole dollar.

4. Provide a short discussion/interpretation of each of the above-three variances.

Required:

Calculate and show underlying calculations for each of the following variances:

1. Variable overhead flexible-budget (FB) variance, to the nearest whole dollar.

2. Fixed overhead spending variance, to the nearest whole dollar.

3. Fixed overhead production volume variance, to the nearest whole dollar.

4. Provide a short discussion/interpretation of each of the above-three variances.

(Essay)

4.9/5 (34)

Bluecap Co. uses a standard cost system and flexible budgets for control purposes. The following budgeted information pertains to 2019: Denominator volume-number of units 8,000 Denominator volume-percent of capacity 80\% Denominator volume-standard direct labor hours (DLHs) 24,000 Budgeted variable factory overhead cost at denominator volume \1 03,200 Total standard factory overhead rate per DLH \ 15.10 During 2019, Bluecap worked 28,000 DLHs and manufactured 9,600 units. The actual factory overhead cost for the year was $14,000 greater than the flexible budget amount for the units produced, of which $6,000 was due to fixed factory overhead. In preparing a budget for 2020 Bluecap decided to raise the level of operation to 90% of capacity (a level it considers to be "practical capacity"), to manufacture 9,000 units at a budgeted total of 27,000 DLHs.

The standard variable overhead application rate per direct labor hour in 2019 for Bluecap Co., to two decimal places, was:

(Multiple Choice)

4.9/5 (35)

Gerhan Company's flexible budget for the units manufactured in May shows $15,640 of total factory overhead; this output level represents 70% of available capacity. During May, the company applied overhead to production at the rate of $3.00 per direct labor hour (DLH), based on a denominator volume level of 6,120 DLHs, which represents 90% of available capacity. The company used 5,000 DLHs and incurred $16,500 of total factory overhead cost during May, including $6,800 for fixed factory overhead.

What is the variable factory overhead spending variance (to the nearest whole dollar) in May, assuming Gerhan uses a four-variance breakdown (decomposition) of the total overhead variance?

(Multiple Choice)

4.7/5 (34)

The difference in each period between total variable overhead cost incurred and the standard variable overhead cost for the period based on the actual quantity of the cost driver used to apply variable overhead cost is the:

(Multiple Choice)

4.8/5 (36)

Bluecap Co. uses a standard cost system and flexible budgets for control purposes. The following budgeted information pertains to 2019: Denominator volume-number of units 8,000 Denominator volume-percent of capacity 80\% Denominator volume-standard direct labor hours (DLHs) 24,000 Budgeted variable factory overhead cost at denominator volume \1 03,200 Total standard factory overhead rate per DLH \ 15.10 During 2019, Bluecap worked 28,000 DLHs and manufactured 9,600 units. The actual factory overhead cost for the year was $14,000 greater than the flexible budget amount for the units produced, of which $6,000 was due to fixed factory overhead. In preparing a budget for 2020 Bluecap decided to raise the level of operation to 90% of capacity (a level it considers to be "practical capacity"), to manufacture 9,000 units at a budgeted total of 27,000 DLHs.

The variable overhead spending variance in 2019 for Bluecap Co. (to the nearest whole dollar) was:

(Multiple Choice)

4.9/5 (27)

When a company uses absorption costing, there is the potential for income manipulation based on choice of the denominator volume for setting the fixed overhead allocation rate. In which case is this manipulation-potential manifested?

(Multiple Choice)

5.0/5 (39)

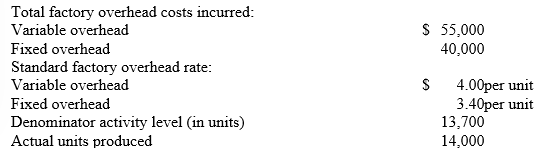

Ben Simon Corp. has the following information about its standards and production activity for the month of November: Required:

Calculate (to the nearest whole dollar) and show supporting calculations for each of the following variances:

1. Variable overhead flexible-budget variance.

2. Fixed overhead spending variance.

3. Fixed overhead production volume variance.

Required:

Calculate (to the nearest whole dollar) and show supporting calculations for each of the following variances:

1. Variable overhead flexible-budget variance.

2. Fixed overhead spending variance.

3. Fixed overhead production volume variance.

(Essay)

4.8/5 (40)

The following information for the past year is available from Thinnews Co., a company that uses machine hours to apply standard factory overhead cost to outputs: Actual total factory overhead cost incurred \ 24,000 Actual fixed overhead cost incurred \ 10,000 Budgeted fixed overhead cost \ 11,000 Actual machine hours 5,000 Standard machine hours allowed for the units manufactured 4,800 Denominator volume-machine hours 5,500 Standard variable overhead rate per machine hour \ 3.00 The variable overhead spending variance, to the nearest whole dollar, is:

(Multiple Choice)

4.8/5 (38)

Gerhan Company's flexible budget for the units manufactured in May shows $15,640 of total factory overhead; this output level represents 70% of available capacity. During May, the company applied overhead to production at the rate of $3.00 per direct labor hour (DLH), based on a denominator volume level of 6,120 DLHs, which represents 90% of available capacity. The company used 5,000 DLHs and incurred $16,500 of total factory overhead cost during May, including $6,800 for fixed factory overhead.

What is the factory overhead efficiency variance (to the nearest whole dollar) for Gerhan Company in May, under the assumption that the company uses a two-variance breakdown (decomposition) of the total overhead variance?

(Multiple Choice)

4.7/5 (36)

Which of the following factors is not usually important when deciding whether to investigate a variance?

(Multiple Choice)

4.9/5 (35)

A manufacturing company that uses standard costs and flexible budgets can break the total variable overhead cost variance into:

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)