Exam 13: Return, Risk, and the Security Market Line

Exam 1: Introduction to Corporate Finance61 Questions

Exam 2: Financial Statements, Taxes, and Cash Flow99 Questions

Exam 3: Working With Financial Statements111 Questions

Exam 4: Long-Term Financial Planning and Growth103 Questions

Exam 5: Introduction to Valuation: The Time Value of Money68 Questions

Exam 6: Discounted Cash Flow Valuation132 Questions

Exam 7: Interest Rates and Bond Valuation128 Questions

Exam 8: Stock Valuation119 Questions

Exam 9: Net Present Value and Other Investment Criteria112 Questions

Exam 10: Making Capital Investment Decisions108 Questions

Exam 11: Project Analysis and Evaluation106 Questions

Exam 12: Some Lessons From Capital Market History98 Questions

Exam 13: Return, Risk, and the Security Market Line108 Questions

Exam 14: Cost of Capital101 Questions

Exam 15: Raising Capital91 Questions

Exam 16: Financial Leverage and Capital Structure Policy98 Questions

Exam 17: Dividends and Dividend Policy104 Questions

Exam 18: Short-Term Finance and Planning110 Questions

Exam 19: Cash and Liquidity Management101 Questions

Exam 20: Credit and Inventory Management97 Questions

Exam 21: International Corporate Finance99 Questions

Exam 22: Behavioral Finance: Implications for Financial Management45 Questions

Exam 23: Risk Management: An Introduction to Financial Engineering71 Questions

Exam 24: Options and Corporate Finance106 Questions

Exam 25: Option Valuation86 Questions

Exam 26: Mergers and Acquisitions79 Questions

Exam 27: Leasing72 Questions

Select questions type

Which one of the following is a risk that applies to most securities?

(Multiple Choice)

4.9/5  (30)

(30)

Which one of the following statements is correct concerning unsystematic risk?

(Multiple Choice)

4.9/5 (37)

The intercept point of the security market line is the rate of return which corresponds to:

(Multiple Choice)

4.7/5 (29)

Explain how the beta of a portfolio can equal the market beta if 50 percent of the portfolio is invested in a security that has twice the amount of systematic risk as an average risky security.

(Essay)

4.8/5 (28)

The returns on the common stock of New Image Products are quite cyclical. In a boom economy, the stock is expected to return 32 percent in comparison to 14 percent in a normal economy and a negative 28 percent in a recessionary period. The probability of a recession is 25 percent while the probability of a boom is 10 percent. What is the standard deviation of the returns on this stock?

(Multiple Choice)

4.8/5 (35)

Which of the following statements concerning risk are correct?

I. Nondiversifiable risk is measured by beta.

II. The risk premium increases as diversifiable risk increases.

III. Systematic risk is another name for nondiversifiable risk.

IV. Diversifiable risks are market risks you cannot avoid.

(Multiple Choice)

4.7/5 (26)

Which one of the following indicates a portfolio is being effectively diversified?

(Multiple Choice)

5.0/5 (45)

A news flash just appeared that caused about a dozen stocks to suddenly drop in value by about 20 percent. What type of risk does this news flash represent?

(Multiple Choice)

4.9/5 (38)

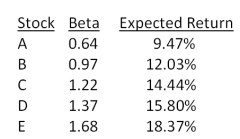

Which one of the following stocks is correctly priced if the risk-free rate of return is 3.7 percent and the market risk premium is 8.8 percent?

(Multiple Choice)

4.8/5 (32)

You want your portfolio beta to be 0.95. Currently, your portfolio consists of $4,000 invested in stock A with a beta of 1.47 and $3,000 in stock B with a beta of 0.54. You have another $9,000 to invest and want to divide it between an asset with a beta of 1.74 and a risk-free asset. How much should you invest in the risk-free asset?

(Multiple Choice)

4.8/5 (35)

Which one of the following measures the amount of systematic risk present in a particular risky asset relative to the systematic risk present in an average risky asset?

(Multiple Choice)

4.9/5 (35)

Total risk is measured by _____ and systematic risk is measured by _____.

(Multiple Choice)

4.7/5 (28)

The capital asset pricing model (CAPM) assumes which of the following?

I. a risk-free asset has no systematic risk.

II. beta is a reliable estimate of total risk.

III. the reward-to-risk ratio is constant.

IV. the market rate of return can be approximated.

(Multiple Choice)

4.9/5 (39)

Which one of the following will be constant for all securities if the market is efficient and securities are priced fairly?

(Multiple Choice)

4.9/5 (36)

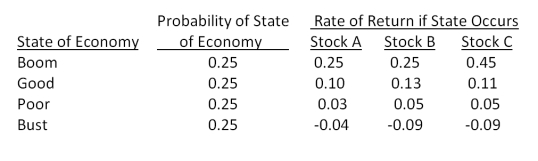

Your portfolio is invested 26 percent each in Stocks A and C, and 48 percent in Stock B. What is the standard deviation of your portfolio given the following information?

(Multiple Choice)

4.9/5 (24)

Steve has invested in twelve different stocks that have a combined value today of $121,300. Fifteen percent of that total is invested in Wise Man Foods. The 15 percent is a measure of which one of the following?

(Multiple Choice)

4.9/5 (31)

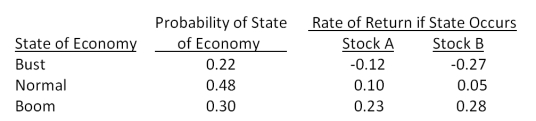

Suppose you observe the following situation:  Assume the capital asset pricing model holds and stock A's beta is greater than stock B's beta by 0.21. What is the expected market risk premium?

Assume the capital asset pricing model holds and stock A's beta is greater than stock B's beta by 0.21. What is the expected market risk premium?

(Multiple Choice)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)