Exam 13: Return, Risk, and the Security Market Line

Exam 1: Introduction to Corporate Finance61 Questions

Exam 2: Financial Statements, Taxes, and Cash Flow99 Questions

Exam 3: Working With Financial Statements111 Questions

Exam 4: Long-Term Financial Planning and Growth103 Questions

Exam 5: Introduction to Valuation: The Time Value of Money68 Questions

Exam 6: Discounted Cash Flow Valuation132 Questions

Exam 7: Interest Rates and Bond Valuation128 Questions

Exam 8: Stock Valuation119 Questions

Exam 9: Net Present Value and Other Investment Criteria112 Questions

Exam 10: Making Capital Investment Decisions108 Questions

Exam 11: Project Analysis and Evaluation106 Questions

Exam 12: Some Lessons From Capital Market History98 Questions

Exam 13: Return, Risk, and the Security Market Line108 Questions

Exam 14: Cost of Capital101 Questions

Exam 15: Raising Capital91 Questions

Exam 16: Financial Leverage and Capital Structure Policy98 Questions

Exam 17: Dividends and Dividend Policy104 Questions

Exam 18: Short-Term Finance and Planning110 Questions

Exam 19: Cash and Liquidity Management101 Questions

Exam 20: Credit and Inventory Management97 Questions

Exam 21: International Corporate Finance99 Questions

Exam 22: Behavioral Finance: Implications for Financial Management45 Questions

Exam 23: Risk Management: An Introduction to Financial Engineering71 Questions

Exam 24: Options and Corporate Finance106 Questions

Exam 25: Option Valuation86 Questions

Exam 26: Mergers and Acquisitions79 Questions

Exam 27: Leasing72 Questions

Select questions type

You would like to combine a risky stock with a beta of 1.68 with U.S. Treasury bills in such a way that the risk level of the portfolio is equivalent to the risk level of the overall market. What percentage of the portfolio should be invested in the risky stock?

(Multiple Choice)

4.9/5  (32)

(32)

The expected risk premium on a stock is equal to the expected return on the stock minus the:

(Multiple Choice)

4.9/5 (44)

Which of the following are examples of diversifiable risk?

I. earthquake damages an entire town

II. federal government imposes a $100 fee on all business entities

III. employment taxes increase nationally

IV. toymakers are required to improve their safety standards

(Multiple Choice)

4.7/5 (39)

You have $10,000 to invest in a stock portfolio. Your choices are Stock X with an expected return of 13 percent and Stock Y with an expected return of 8 percent. Your goal is to create a portfolio with an expected return of 12.4 percent. All money must be invested. How much will you invest in stock X?

(Multiple Choice)

4.9/5 (26)

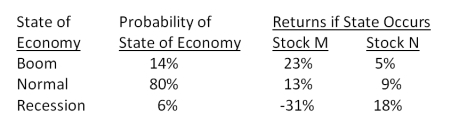

What is the expected return on a portfolio comprised of $6,200 of stock M and $4,500 of stock N if the economy enjoys a boom period?

(Multiple Choice)

4.9/5 (33)

Which of the following statements are correct concerning diversifiable risks?

I. Diversifiable risks can be essentially eliminated by investing in thirty unrelated securities.

II. There is no reward for accepting diversifiable risks.

III. Diversifiable risks are generally associated with an individual firm or industry.

IV. Beta measures diversifiable risk.

(Multiple Choice)

4.9/5 (40)

The expected return on a portfolio considers which of the following factors?

I. percentage of the portfolio invested in each individual security

II. projected states of the economy

III. the performance of each security given various economic states

IV. probability of occurrence for each state of the economy

(Multiple Choice)

4.8/5 (46)

Which one of the following events would be included in the expected return on Sussex stock?

(Multiple Choice)

4.8/5 (31)

You own a stock that you think will produce a return of 11 percent in a good economy and 3 percent in a poor economy. Given the probabilities of each state of the economy occurring, you anticipate that your stock will earn 6.5 percent next year. Which one of the following terms applies to this 6.5 percent?

(Multiple Choice)

4.9/5 (37)

What is the standard deviation of the returns on a stock given the following information?

(Multiple Choice)

5.0/5 (39)

Which one of the following is represented by the slope of the security market line?

(Multiple Choice)

4.8/5 (34)

How many diverse securities are required to eliminate the majority of the diversifiable risk from a portfolio?

(Multiple Choice)

4.9/5 (49)

A stock with an actual return that lies above the security market line has:

(Multiple Choice)

4.7/5 (38)

Explain the difference between systematic and unsystematic risk. Also explain why one of these types of risks is rewarded with a risk premium while the other type is not.

(Essay)

4.9/5 (27)

The expected return on JK stock is 15.78 percent while the expected return on the market is 11.34 percent. The stock's beta is 1.62. What is the risk-free rate of return?

(Multiple Choice)

4.7/5 (32)

The common stock of Jensen Shipping has an expected return of 16.3 percent. The return on the market is 10.8 percent and the risk-free rate of return is 3.8 percent. What is the beta of this stock?

(Multiple Choice)

4.8/5 (40)

A portfolio beta is a weighted average of the betas of the individual securities which comprise the portfolio. However, the standard deviation is not a weighted average of the standard deviations of the individual securities which comprise the portfolio. Explain why this difference exists.

(Essay)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)