Exam 18: Portfolio Performance Evaluation

Exam 1: Investments: Background and Issues55 Questions

Exam 2: Asset Classes and Financial Instruments59 Questions

Exam 3: Securities Markets60 Questions

Exam 4: Managed Funds and Other Investment Companies60 Questions

Exam 5: Risk and Return: Past and Prologue58 Questions

Exam 6: Efficient Diversification56 Questions

Exam 7: Capital Pricing and Arbitrage Pricing Theory59 Questions

Exam 8: The Efficient Market Hypothesis and Behavioral Finance60 Questions

Exam 9: Bond Prices and Yields58 Questions

Exam 10: Managing Bond Portfolios60 Questions

Exam 11: Equity Valuation60 Questions

Exam 12: Macroeconomic and Industry Analysis58 Questions

Exam 13: Financial Statement Analysis55 Questions

Exam 14: Options and Risk Management60 Questions

Exam 15: Futures and Risk Management60 Questions

Exam 16: Investors and the Investment Process60 Questions

Exam 17: Hedge Funds60 Questions

Exam 18: Portfolio Performance Evaluation54 Questions

Select questions type

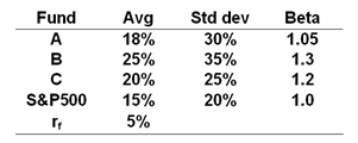

The risk-free rate, average returns, standard deviations and betas for three funds and the S&P500 are given below.  What is the M2 measure for Portfolio B?

What is the M2 measure for Portfolio B?

(Multiple Choice)

4.8/5  (35)

(35)

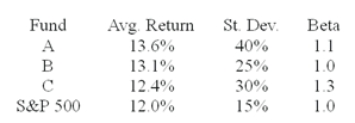

The average returns, standard deviations and betas for three funds are given below along with data for the S&P 500 index. The risk-free return during the sample period is 6%.  You wish to evaluate the three mutual funds using the Sharpe measure for performance evaluation. The fund with the highest Sharpe measure of performance is ________.

You wish to evaluate the three mutual funds using the Sharpe measure for performance evaluation. The fund with the highest Sharpe measure of performance is ________.

(Multiple Choice)

4.7/5 (29)

Portfolio performance is often decomposed into various subcomponents such as the return due to ________.

I. broad asset allocation across security classes

II. sector weightings within equity markets

III. security selection with a given sector

The decision that contributes most to the fund performance is:

(Multiple Choice)

4.7/5 (39)

A passive benchmark portfolio is ________.

I. a portfolio where the asset allocation across broad asset classes is neutral and not determined by forecasts of performance of the different asset classes

II. one where an indexed portfolio is held within each asset class

III. often called the bogey

(Multiple Choice)

4.9/5 (35)

Probably the biggest problem with evaluating portfolio performance of actively managed funds is the assumption that ________.

(Multiple Choice)

4.9/5 (42)

The market timing form of active portfolio management relies on ________ forecasting and the security selection form of active portfolio management relies on ________ forecasting.

(Multiple Choice)

4.8/5 (40)

What is the contribution of asset allocation to relative performance?

(Multiple Choice)

4.9/5 (30)

Which one of the following performance measures is the Sharpe measure?

(Multiple Choice)

4.8/5 (37)

Consider the theory of active portfolio management. Shares A and B have the same beta and non-systematic risk. Share A has higher positive alpha than share B. You should want ________ in your active portfolio.

(Multiple Choice)

4.9/5 (34)

A fund has excess performance of 1.5%. In looking at the fund's investment breakdown you see that the fund overweighed equities relative to the benchmark and the average return on the fund's equity portfolio was slightly lower than the equity benchmark return. The excess performance for this fund is probably due to ________.

(Multiple Choice)

4.9/5 (49)

Portfolio managers Paul Martin and Kevin Krueger each manage $1 000 000 funds. Paul Martin has perfect foresight and the call option value of his perfect foresight is $150 000. Kevin Krueger is an imperfect forecaster and correctly predicts 50% of all bull markets and 70% of all bear markets. The correct measure of timing ability for Kevin Krueger is ________.

(Multiple Choice)

4.8/5 (38)

A portfolio generates an annual return of 13%, a beta of 0.7 and a standard deviation of 17%. The market index return is 14% and has a standard deviation of 21%. What is Jensen's alpha of the portfolio if the risk-free rate is 5%?

(Multiple Choice)

4.7/5 (35)

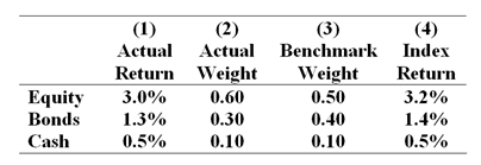

The table presents the actual return of each sector of the manager's portfolio in column (1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral sector allocations in column (3) and the returns of sector indexes in column (4).  What was the bogey's return in the month?

What was the bogey's return in the month?

(Multiple Choice)

4.9/5 (41)

If an investor is a successful market timer, his distribution of monthly portfolio returns will ________.

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)