Exam 18: Portfolio Performance Evaluation

Exam 1: Investments: Background and Issues55 Questions

Exam 2: Asset Classes and Financial Instruments59 Questions

Exam 3: Securities Markets60 Questions

Exam 4: Managed Funds and Other Investment Companies60 Questions

Exam 5: Risk and Return: Past and Prologue58 Questions

Exam 6: Efficient Diversification56 Questions

Exam 7: Capital Pricing and Arbitrage Pricing Theory59 Questions

Exam 8: The Efficient Market Hypothesis and Behavioral Finance60 Questions

Exam 9: Bond Prices and Yields58 Questions

Exam 10: Managing Bond Portfolios60 Questions

Exam 11: Equity Valuation60 Questions

Exam 12: Macroeconomic and Industry Analysis58 Questions

Exam 13: Financial Statement Analysis55 Questions

Exam 14: Options and Risk Management60 Questions

Exam 15: Futures and Risk Management60 Questions

Exam 16: Investors and the Investment Process60 Questions

Exam 17: Hedge Funds60 Questions

Exam 18: Portfolio Performance Evaluation54 Questions

Select questions type

In performance measurement the bogey portfolio is designed to ________.

(Multiple Choice)

4.9/5  (37)

(37)

Which one of the following averaging methods is the preferred method of constructing returns series for use in evaluating portfolio performance?

(Multiple Choice)

4.8/5 (40)

Active portfolio management consists of ________.

I. market timing

II. security selection

III. sector selection within given markets

IV. indexing

(Multiple Choice)

4.7/5 (40)

The critical variable in the determination of the success of the active portfolio is the share's ________.

(Multiple Choice)

5.0/5 (38)

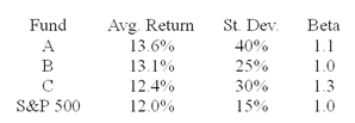

The average returns, standard deviations and betas for three funds are given below along with data for the S&P 500 index. The risk-free return during the sample period is 6%.  You wish to evaluate the three mutual funds using the Jensen measure for performance evaluation. The fund with the highest Jensen measure of performance is ________.

You wish to evaluate the three mutual funds using the Jensen measure for performance evaluation. The fund with the highest Jensen measure of performance is ________.

(Multiple Choice)

4.9/5 (30)

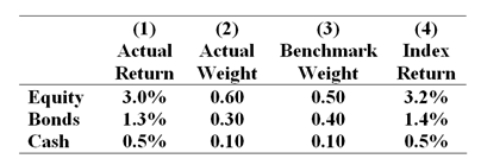

The table presents the actual return of each sector of the manager's portfolio in column (1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral sector allocations in column (3) and the returns of sector indexes in column (4).  What was the manager's return in the month?

What was the manager's return in the month?

(Multiple Choice)

4.8/5 (31)

Active portfolio managers try to construct a risky portfolio with ________.

(Multiple Choice)

4.9/5 (34)

An attribution analysis will NOT likely contain which of the following components?

(Multiple Choice)

4.7/5 (40)

Your return will generally be higher using the ________ if you time your transactions poorly and your return will generally be higher using the ________ if you time your transactions well.

(Multiple Choice)

4.8/5 (36)

Morningstar's RAR produce results which are similar but not identical to ________.

(Multiple Choice)

4.9/5 (30)

The contribution of security selection within asset classes to the total excess return was ________.

(Multiple Choice)

4.8/5 (32)

Consider the Sharpe and Treynor performance measures. When a pension fund is large and well diversified in total and it has many managers, the ________ measure is better for evaluating individual managers while the ________ measure is better for evaluating the manager of a small fund with only one manager responsible for all investments that may not be fully diversified.

(Multiple Choice)

4.9/5 (40)

Assume you purchased a rental property for $100 000 and sold it one year later for $115 000 (there was no mortgage on the property). At the time of the sale, you paid $3 000 in commissions and $1 000 in taxes. If you received $10 000 in rental income (all received at the end of the year), what annual rate of return did you earn?

(Multiple Choice)

4.9/5 (42)

Which one of the following is largely based on forecasts of macroeconomic factors?

(Multiple Choice)

4.7/5 (35)

What was the manager's over- or under-performance for the month?

(Multiple Choice)

4.8/5 (46)

A portfolio generates an annual return of 13%, a beta of 0.7 and a standard deviation of 17%. The market index return is 14% and has a standard deviation of 21%. What is the Sharpe measure of the portfolio if the risk-free rate is 5%?

(Multiple Choice)

4.8/5 (42)

The correct measure of timing ability is ________ for a portfolio manager who correctly forecasts 55% of bull markets and 55% of bear markets.

(Multiple Choice)

4.9/5 (34)

The M2 measure of portfolio performance was developed by ________.

(Multiple Choice)

4.8/5 (38)

The ________ calculates the reward-to-risk trade-off by dividing the average portfolio excess return by the portfolio beta.

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)