Exam 7: Futures and Options on Foreign Exchange

Exam 1: Globalization and the Multinational Firm99 Questions

Exam 2: International Monetary System100 Questions

Exam 3: Balance of Payments100 Questions

Exam 4: Corporate Governance Around the World100 Questions

Exam 5: The Market for Foreign Exchange100 Questions

Exam 6: International Parity Relationships and Forecasting Foreign Exchange Rates100 Questions

Exam 7: Futures and Options on Foreign Exchange100 Questions

Exam 8: Management of Transaction Exposure100 Questions

Exam 9: Management of Economic Exposure100 Questions

Exam 10: Management of Translation Exposure81 Questions

Exam 11: International Banking and Money Market101 Questions

Exam 12: International Bond Market99 Questions

Exam 13: International Equity Markets99 Questions

Exam 14: Interest Rate and Currency Swaps95 Questions

Exam 15: International Portfolio Investment101 Questions

Exam 16: Foreign Direct Investment and Cross-Border Acquisitions100 Questions

Exam 17: International Capital Structure and the Cost of Capital99 Questions

Exam 18: International Capital Budgeting101 Questions

Exam 19: Multinational Cash Management98 Questions

Exam 20: International Trade Finance100 Questions

Exam 21: International Tax Environment and Transfer Pricing100 Questions

Select questions type

The current spot exchange rate is $1.55 = €1.00 and the three-month forward rate is $1.60 = €1.00.Consider a three-month American call option on €62,500 with a strike price of $1.50 = €1.00.Immediate exercise of this option will generate a profit of

(Multiple Choice)

4.8/5  (30)

(30)

Comparing "forward" and "futures" exchange contracts,we can say that

(Multiple Choice)

4.9/5 (48)

Draw the tree for a put option on $20,000 with a strike price of £10,000.The current exchange rate is £1.00 = $2.00 and in one period the dollar value of the pound will either double or be cut in half.The current interest rates are i$ = 3% and are i£ = 2%.

(Multiple Choice)

4.9/5 (39)

For European currency options written on euro with a strike price in dollars,what of the effect of an increase in the exchange rate S(€/$)?

(Multiple Choice)

4.9/5 (40)

Suppose you observe the following 1-year interest rates,spot exchange rates and futures prices.Futures contracts are available on €10,000.How much risk-free arbitrage profit could you make on 1 contract at maturity from this mispricing?

(Multiple Choice)

4.8/5 (36)

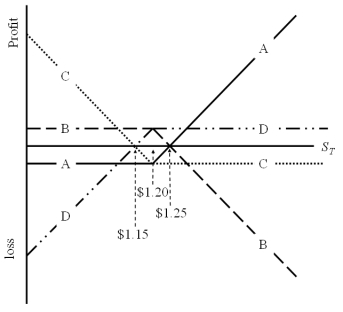

Which of the lines is a graph of the profit at maturity of writing a call option on €62,500 with a strike price of $1.20 = €1.00 and an option premium of $3,125?

(Multiple Choice)

4.9/5 (26)

For European currency options written on euro with a strike price in dollars,what of the effect of an increase r€?

(Multiple Choice)

4.9/5 (41)

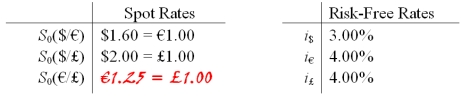

Find the Black-Scholes price of a six-month call option written on €100,000 with a strike price of $1.00 = €1.00.The current exchange rate is $1.25 = €1.00; The U.S.risk-free rate is 5% over the period and the euro-zone risk-free rate is 4%.The volatility of the underlying asset is 10.7 percent.

(Multiple Choice)

4.8/5 (30)

If the call finishes out-of-the-money what is your replicating portfolio cash flow?

(Essay)

4.9/5 (47)

Consider a 1-year call option written on £10,000 with an exercise price of $2.00 = £1.00.The current exchange rate is $2.00 = £1.00; The U.S.risk-free rate is 5% over the period and the U.K.risk-free rate is also 5%.In the next year,the pound will either double in dollar terms or fall by half (i.e.u = 2 and d = ½).If you write 1 call option,what is the value today (in dollars)of the hedge portfolio?

(Multiple Choice)

4.7/5 (34)

Consider an option to buy €12,500 for £10,000. In the next period, the euro can strengthen against the pound by 25% (i.e. each euro will buy 25% more pounds) or weaken by 20%.

Big hint: don't round, keep exchange rates out to at least 4 decimal places.  -Calculate the hedge ratio.

-Calculate the hedge ratio.

(Essay)

4.8/5 (40)

Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On the other hand, the euro could depreciate against the pound by 20 percent.

Big hint: don't round, keep exchange rates out to at least 4 decimal places.  -Calculate the hedge ratio.

-Calculate the hedge ratio.

(Essay)

4.8/5 (38)

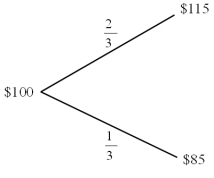

Find the value of a call option written on €100 with a strike price of $1.00 = €1.00.In one period there are two possibilities: the exchange rate will move up by 15% or down by 15% .The U.S.risk-free rate is 5% over the period.The risk-neutral probability of dollar depreciation is 2/3 and the risk-neutral probability of the dollar strengthening is 1/3.

(Multiple Choice)

4.9/5 (36)

Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On the other hand, the euro could depreciate against the pound by 20 percent.

Big hint: don't round, keep exchange rates out to at least 4 decimal places.

-Find the risk neutral probability of an "up" move.

(Essay)

4.9/5 (33)

For European options,what of the effect of an increase in St?

(Multiple Choice)

4.9/5 (42)

Comparing "forward" and "futures" exchange contracts,we can say that

(Multiple Choice)

4.9/5 (46)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)