Exam 14: Interest Rate and Currency Swaps

Exam 1: Globalization and the Multinational Firm99 Questions

Exam 2: International Monetary System100 Questions

Exam 3: Balance of Payments100 Questions

Exam 4: Corporate Governance Around the World100 Questions

Exam 5: The Market for Foreign Exchange100 Questions

Exam 6: International Parity Relationships and Forecasting Foreign Exchange Rates100 Questions

Exam 7: Futures and Options on Foreign Exchange100 Questions

Exam 8: Management of Transaction Exposure100 Questions

Exam 9: Management of Economic Exposure100 Questions

Exam 10: Management of Translation Exposure81 Questions

Exam 11: International Banking and Money Market101 Questions

Exam 12: International Bond Market99 Questions

Exam 13: International Equity Markets99 Questions

Exam 14: Interest Rate and Currency Swaps95 Questions

Exam 15: International Portfolio Investment101 Questions

Exam 16: Foreign Direct Investment and Cross-Border Acquisitions100 Questions

Exam 17: International Capital Structure and the Cost of Capital99 Questions

Exam 18: International Capital Budgeting101 Questions

Exam 19: Multinational Cash Management98 Questions

Exam 20: International Trade Finance100 Questions

Exam 21: International Tax Environment and Transfer Pricing100 Questions

Select questions type

In the swap market,which position potentially carries greater risks,broker or dealer?

(Multiple Choice)

4.7/5  (32)

(32)

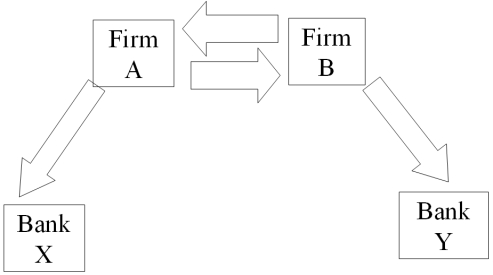

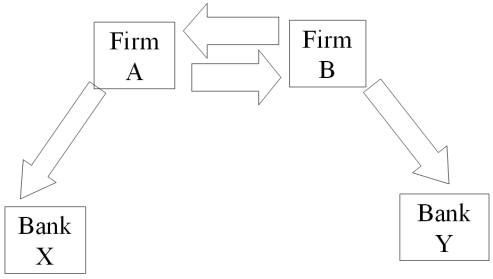

Devise a direct swap for A and B that has no swap bank.Show their external borrowing.Answer the problem in the template provided.

(Essay)

4.8/5 (40)

A major risk faced by a swap dealer is exchange rate risk.This is

(Multiple Choice)

4.8/5 (44)

Consider the situation of firm A and firm B. The current exchange rate is $2.00/£. Firm A is a U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA credit ratings. \ £ \ 6\% £5\% \ 7\% £4\%

-Explain how firm A could use the forward exchange markets to redenominate a 2-year $60m 6% USD loan into a 2-year pound denominated loan.

(Essay)

4.9/5 (34)

Devise a direct swap for A and B that has no swap bank.Show their external borrowing.Answer the problem in the template provided.

(Essay)

4.7/5 (29)

Consider the situation of firm A and firm B. The current exchange rate is $2.00/£. Firm A is a U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA credit ratings. \ £ \ 6\% £5\% \ 7\% £4\% The IRP 1-year and 2-year forward exchange rates are (\ \mid£)== (\ \mid£)==  -Explain how firm B could use the forward exchange markets to redenominate a 2-year £30m 4% pound sterling loan into a 2-year USD-denominated loan.

-Explain how firm B could use the forward exchange markets to redenominate a 2-year £30m 4% pound sterling loan into a 2-year USD-denominated loan.

(Essay)

4.9/5 (44)

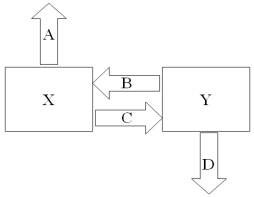

Company X wants to borrow $10,000,000 floating for 5 years.Company Y wants to borrow $10,000,000 fixed for 5 years.Their external borrowing opportunities are: Fixed-Rate Borrowing Floating-Rate Cost Borrowing Cost Company X 10\% LIBOR Company Y 12\% LIBOR +1.5\% Design a mutually beneficial interest only swap for X and Y with a notational principal of $10 million by having appropriate values for A = Company X's external borrowing rate

B = Company Y's payment to X (rate)

C = Company X's payment to Y (rate)

D = Company Y's external borrowing rate

(Multiple Choice)

4.9/5 (29)

Show how your proposed swap would work for firm

A.(e.g.if you were acting as an agent for the swap bank, try to "sell" firm A on your swap)

I would point out that his contracting costs would be less with just having 1 swap instead of 2 forward contracts.Also, he might be able to get a better rate through the swap if he can't find forward contracts at his desired maturity and amounts.

(Essay)

4.8/5 (42)

A swap bank has identified two companies with mirror-image financing needs (they both want to borrow equivalent amounts for the same amount of time.Company X has agreed to one leg of the swap but company Y is "playing hard to get".

(Multiple Choice)

4.9/5 (32)

Suppose that the swap that you proposed in question 2 is now 4 years old (i.e.there is exactly one year to go on the swap).The fourth payment has already been made.If the spot exchange rate prevailing in year 4 is $1.8778 = €1 and the 1-year forward exchange rate prevailing in year 4 is $1.95 = €1,what is the value of the swap to the party paying dollars? If the swap were initiated today the correct rates would be as shown:

(Essay)

4.7/5 (41)

Consider the situation of firm A and firm B. The current exchange rate is $2.00/£. Firm A is a U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA credit ratings. \ £ \ 6\% £5\% \ 7\% £4\%

-Explain how this opportunity affects which swap firm B will be willing to participate in.

(Essay)

4.8/5 (42)

Act as a swap bank and quote bid and ask prices to A and B that are attractive to A and B and promise to make at least 20bp for your firm.

(Essay)

4.8/5 (37)

Which combination of the following statements is true about a swap bank? (i)-it is a generic term to describe a financial institution that facilitates swaps between counterparties

(ii)- it can be an international commercial bank

(iii)- it can be an investment bank

(iv)- it can be a merchant bank

(v)- it can be an independent operator

(Multiple Choice)

4.7/5 (36)

Consider the situation of firm A and firm B. The current exchange rate is $2.00/£. Firm A is a U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA credit ratings. \ £ \ 6\% £5\% \ 7\% £4\% The IRP 1-year and 2-year forward exchange rates are (\ \mid£)== (\ \mid£)==

-Explain how firm B could use two of the swaps offered above to hedge its exchange rate risk.

(Essay)

4.9/5 (28)

XYZ Corporation enters into a 6-year interest rate swap with a swap bank in which it agrees to pay the swap bank a fixed-rate of 9 percent annually on a notional amount of SFr10,000,000 and receive LIBOR - ½ percent.As of the third reset date (i.e.mid-way through the 6 year agreement),calculate the price of the swap,assuming that the fixed-rate at which XYZ can borrow has increased to 10%.

(Multiple Choice)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)