Exam 7: Efficiency, Exchange, and the Invisible Hand in Action

Exam 1: Thinking Like an Economist134 Questions

Exam 2: Comparative Advantage109 Questions

Exam 3: Supply and Demand120 Questions

Exam 4: Elasticity130 Questions

Exam 5: Demand103 Questions

Exam 6: Perfectly Competitive Supply108 Questions

Exam 7: Efficiency, Exchange, and the Invisible Hand in Action115 Questions

Exam 8: Monopoly, Oligopoly, and Monopolistic Competition104 Questions

Exam 9: Games and Strategic Behavior113 Questions

Exam 10: Externalities and Property Rights127 Questions

Exam 11: The Economics of Information145 Questions

Exam 12: Labor Markets, Poverty, and Income Distribution143 Questions

Exam 13: The Environment, Health, and Safety140 Questions

Exam 14: Public Goods and Tax Policy144 Questions

Exam 15: Spending, Income, and GDP150 Questions

Exam 16: Inflation and the Price Level146 Questions

Exam 17: Wages and Unemployment134 Questions

Exam 18: Economic Growth142 Questions

Exam 19: Saving, Capital Formation, and Financial Markets138 Questions

Exam 20: Money, Prices, and the Financial System126 Questions

Exam 21: Short-Term Economic Fluctuations118 Questions

Exam 22: Spending, Output, and Fiscal Policy133 Questions

Exam 23: Monetary Policy and the Federal Reserve101 Questions

Exam 24: Aggregate Demand, Aggregate Supply, and Business Cycles90 Questions

Exam 25: Macroeconomic Policy75 Questions

Exam 26: Exchange Rates, International Trade, and Capital Flows130 Questions

Select questions type

If the demand curve fails to capture all of the benefits of consumption,then the:

(Multiple Choice)

4.9/5  (25)

(25)

Daily Supply and Demand: Oranges in Hurricane Alley  Refer to the figure above.The marginal buyer values the tenth pound of oranges at ____.

Refer to the figure above.The marginal buyer values the tenth pound of oranges at ____.

(Multiple Choice)

4.8/5 (39)

Which of the following is NOT guaranteed by the efficiency of the market equilibrium?

(Multiple Choice)

4.8/5 (37)

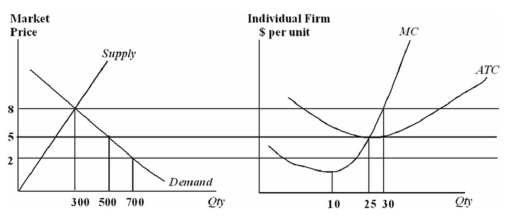

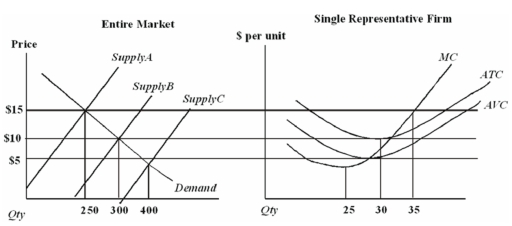

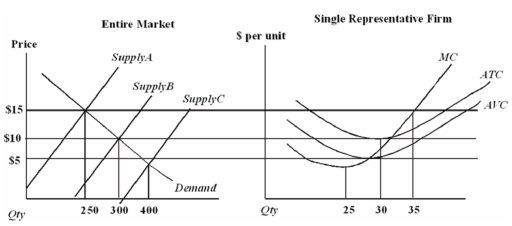

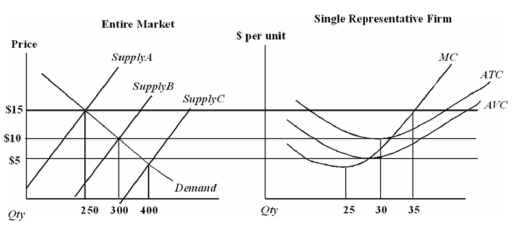

The following graphs depict a perfectly competitive firm and its market.

Assume that all firms in this industry have identical cost functions.  A starting assumption about this industry was that all of the firms had identical cost functions.This assumption

A starting assumption about this industry was that all of the firms had identical cost functions.This assumption

(Multiple Choice)

4.8/5 (43)

Assume that all firms in this industry have identical cost functions.  The long-run equilibrium price in this industry is

The long-run equilibrium price in this industry is

(Multiple Choice)

4.8/5 (39)

Assume that all firms in this industry have identical cost functions.  In the long run,there will be ______ firms in this market.

In the long run,there will be ______ firms in this market.

(Multiple Choice)

4.8/5 (37)

Daily Supply and Demand: Oranges in Hurricane Alley  Refer to the figure above.At the price of $4.00,sellers offer _____ pounds of oranges per day,and buyers want to purchase ____ pounds of oranges a day.

Refer to the figure above.At the price of $4.00,sellers offer _____ pounds of oranges per day,and buyers want to purchase ____ pounds of oranges a day.

(Multiple Choice)

4.7/5 (35)

Barriers to entry are _____,and one effect of barriers to entry is to _____ the ability of the invisible hand to allocate resources efficiently.

(Multiple Choice)

4.9/5 (38)

Suppose that a firm is located along a river.The firm uses water from the river to cool its machinery and returns the water to the river several degrees warmer,which has led to a decline in the fish population downstream of the firm.

The damage to the downstream fish is a(n):

(Multiple Choice)

4.7/5 (40)

An implication of entry and exit in response to the profit incentive is that,for perfectly competitive firms,

(Multiple Choice)

4.9/5 (35)

Duke is a particularly highly skilled negotiator.The law firm that hires Duke is able to collect twice as much revenue per hour of Duke's time than it can for any other negotiator in town.The increased revenue will:

(Multiple Choice)

4.8/5 (38)

Assume that all firms in this industry have identical cost functions.  When price is $15 in this industry,

When price is $15 in this industry,

(Multiple Choice)

4.9/5 (35)

The statement,"price distributes goods and services to those that value them the most" refers to the ______ function of price.

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)