Exam 9: Nontaxable Exchanges

Exam 1: Taxes and Taxing Jurisdictions85 Questions

Exam 2: Policy Standards for a Good Tax85 Questions

Exam 3: Taxes As Transaction Costs82 Questions

Exam 4: Maxims of Income Tax Planning92 Questions

Exam 5: Tax Research75 Questions

Exam 6: Taxable Income From Business Operations116 Questions

Exam 7: Property Acquisitions and Cost Recovery Deductions106 Questions

Exam 8: Property Dispositions110 Questions

Exam 9: Nontaxable Exchanges97 Questions

Exam 10: Sole Proprietorships, Partnerships, Llcs, and S Corporations87 Questions

Exam 11: The Corporate Taxpayer97 Questions

Exam 12: The Choice of Business Entity97 Questions

Exam 13: Jurisdictional Issues in Business Taxation102 Questions

Exam 14: The Individual Tax Formula111 Questions

Exam 15: Compensation and Retirement Planning107 Questions

Exam 16: Investment and Personal Financial Planning104 Questions

Exam 17: Tax Consequences of Personal Activities93 Questions

Exam 18: The Tax Compliance Process86 Questions

Select questions type

Nagin Inc. transferred an old asset in exchange for a new asset worth $84,000 and $6,000 cash. The old asset and new asset were like-kind properties. Which of the following statements is true?

Free

(Multiple Choice)

4.8/5  (27)

(27)

Correct Answer: Verified

Verified

C

IPM Inc. and Zeta Company formed IPeta Inc. by transferring business assets in exchange for 1,000 shares of IPeta common stock. IPM transferred assets with a $675,000 FMV and a $283,000 adjusted tax basis and received 600 shares. Zeta transferred assets with a $450,000 FMV and a $98,000 adjusted tax basis and received 400 shares. Which of the following statements is false?

Free

(Multiple Choice)

4.8/5 (39)

Correct Answer:Verified

D

A corporation's tax basis in property received in exchange for corporate stock depends on whether the exchange was taxable or nontaxable to the transferors of the property.

Free

(True/False)

4.8/5 (47)

Correct Answer:Verified

True

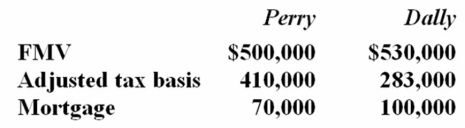

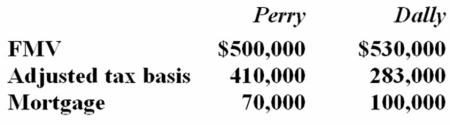

Perry Inc. and Dally Company entered into an exchange of real property. Here is the information for the properties to be exchanged.  Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Dally's gain recognized on the exchange and its tax basis in the property received from Perry.

Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Dally's gain recognized on the exchange and its tax basis in the property received from Perry.

(Multiple Choice)

4.8/5 (38)

A partnership always takes a carryover basis in property received from a partner in exchange for an equity interest in the partnership.

(True/False)

4.9/5 (42)

Eight years ago, Prescott Inc. realized a $16,200 gain on the exchange of old equipment for new equipment. Prescott included the gain in book income, but the exchange was nontaxable. This year, Prescott sold the new equipment for $2,500. At date of sale, the equipment's book basis and tax basis had both been depreciated to zero. Which of the following statements is true?

(Multiple Choice)

4.8/5 (40)

Sissoon Inc. exchanged a business asset for an investment asset. Both assets had a $620,000 appraised FMV. Sissoon's book basis in the business asset was $518,900, and its tax basis was $443,400.

a. Compute Sissoon's book and tax gain if the business asset and investment asset were like-kind properties for tax purposes.

b. Determine Sissoon's book and tax basis of the investment asset acquired in the nontaxable exchange.

c. Compute Sissoon's book and tax gain if the business asset and investment asset were not like-kind properties for tax purposes.

d. Determine Sissoon's book and tax basis of the investment asset acquired in the taxable exchange.

(Essay)

4.8/5 (30)

V&P Company exchanged unencumbered investment land for farmland subject to a $200,000 mortgage. If V&P realized a $168,000 gain on the exchange, it must recognize the entire gain.

(True/False)

4.8/5 (40)

Gain realized on a property exchange that is not recognized is actually deferred rather than nontaxable.

(True/False)

4.8/5 (38)

Mr. Bentley exchanged investment land subject to a $300,000 mortgage for commercial real estate subject to a $188,000 mortgage. Mr. Bentley is treated as paying $112,000 boot in the exchange.

(True/False)

4.8/5 (41)

YCM Inc. exchanged business equipment (initial cost $114,800; accumulated depreciation $63,400) for like-kind equipment worth $110,000 and $10,000 cash. As a result, Rydell must recognize:

(Multiple Choice)

4.8/5 (32)

Tanner Inc. owns a fleet of passenger automobiles that it would like to dispose of in a nontaxable exchange. Which of the following would qualify as like-kind property?

(Multiple Choice)

4.8/5 (39)

Itak Company transferred an old asset with a $44,300 adjusted tax basis in exchange for a new asset worth $48,000 and $3,000 cash. Which of the following statements is false?

(Multiple Choice)

4.8/5 (43)

Kornek Inc. transferred an old asset with a $200,000 adjusted tax basis plus $12,000 cash in exchange for a new asset worth $260,000. Which of the following statements is false?

(Multiple Choice)

4.9/5 (46)

Loonis Inc. and Rhea Company formed LooNR Inc. by transferring business assets in exchange for 1,000 shares of LooNR common stock. Loonis transferred assets with a $820,000 FMV and a $444,000 adjusted tax basis and received 820 shares. Rhea transferred assets with a $180,000 FMV and a $75,000 adjusted tax basis and received 180 shares. Which of the following statements is true?

(Multiple Choice)

4.9/5 (38)

Mr. Weller and the Olson Partnership entered into an exchange of investment real property. Mr. Weller's property was subject to a $428,000 mortgage, which Olson assumed. Olson's property was subject to a $235,000 mortgage, which Mr. Weller assumed. Which of the following statements is true?

(Multiple Choice)

4.9/5 (28)

Loonis Inc. and Rhea Company formed LooNR Inc. by transferring business assets in exchange for 1,000 shares of LooNR common stock. Loonis transferred assets with a $820,000 FMV and a $444,000 adjusted tax basis and received 820 shares. Rhea transferred assets with a $180,000 FMV and a $75,000 adjusted tax basis and received 180 shares. Compute Loonis and Rhea's realized and recognized gain on the exchange.

(Multiple Choice)

4.7/5 (39)

Mrs. Volter exchanged residential real estate for a commercial office building. The residential real estate was subject to a $92,800 mortgage, which was assumed by the other party to the exchange. Mrs. Volter must treat the relief of the mortgage as $92,800 boot received.

(True/False)

4.8/5 (42)

A taxpayer who realizes a loss on the sale of marketable securities and reacquires substantially the same securities within the 30 day period before the sale cannot recognize the loss.

(True/False)

4.9/5 (42)

Perry Inc. and Dally Company entered into an exchange of real property. Here is the information for the properties to be exchanged.  Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Perry's gain recognized on the exchange and its tax basis in the property received from Dally.

Pursuant to the exchange, Perry assumed the mortgage on the Dally property, and Dally assumed the mortgage on the Perry property. Compute Perry's gain recognized on the exchange and its tax basis in the property received from Dally.

(Multiple Choice)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)