Exam 13: Performance Evaluation and Risk Management

Exam 1: A Brief History of Risk and Return100 Questions

Exam 2: The Investment Process100 Questions

Exam 3: Overview of Security Types94 Questions

Exam 4: Mutual Funds101 Questions

Exam 5: The Stock Market106 Questions

Exam 6: Common Stock Valuation104 Questions

Exam 7: Stock Price Behavior and Market Efficiency82 Questions

Exam 8: Behavioral Finance and the Psychology of Investing84 Questions

Exam 9: Interest Rates100 Questions

Exam 10: Bond Prices and Yields95 Questions

Exam 11: Diversification and Risky Asset Allocation84 Questions

Exam 12: Return, Risk, and the Security Market Line84 Questions

Exam 13: Performance Evaluation and Risk Management91 Questions

Exam 14: Futures Contracts97 Questions

Exam 15: Stock Options100 Questions

Exam 16: Option Valuation72 Questions

Exam 17: Projecting Cash Flow and Earnings100 Questions

Exam 18: Corporate Bonds85 Questions

Exam 19: Government Bonds84 Questions

Exam 20: Mortgage-Backed Securities92 Questions

Select questions type

The one-year standard deviation of your portfolio is 16.4 percent. What is the two-year standard deviation?

(Multiple Choice)

4.8/5  (38)

(38)

A portfolio has an expected return of 13.8 percent, a beta of 1.14, and a standard deviation of 12.7 percent. The U.S. Treasury bill rate is 3.2 percent. What is the Treynor ratio?

(Multiple Choice)

4.8/5 (41)

Which one of the following is the primary purpose of the Value-at-Risk computation?

(Multiple Choice)

4.8/5 (33)

A portfolio has a variance of .017424, a beta of 1.06, and an expected return of 13.15 percent. What is the Sharpe ratio if the expected risk-free rate is 3.4 percent?

(Multiple Choice)

4.8/5 (43)

The unadjusted total percentage return on a security that has not been compared to any benchmark is referred to as which one of the following?

(Multiple Choice)

5.0/5 (45)

Which metric measures how volatile a fund's returns are relative to its benchmark?

(Multiple Choice)

4.8/5 (36)

Which one of the following is the best indication that a security is correctly priced according to the Capital Asset Pricing Model?

(Multiple Choice)

4.7/5 (46)

Which of the following measures should be used to determine if a security should be included in a master portfolio?

I. Sharpe ratio

II. Treynor ratio

III. Jensen's alpha

(Multiple Choice)

4.9/5 (39)

The Miller Fund's correlation with the market is .648. What percentage of the fund's movement can be explained by movements in the overall market?

(Multiple Choice)

4.8/5 (31)

Explain the similarities and differences between the Sharpe and Treynor ratios. Also, explain the most appropriate application for each.

(Essay)

4.9/5 (34)

You want to create the best portfolio that can be derived from two assets. Which one of the following will help you identify that portfolio?

(Multiple Choice)

4.8/5 (39)

A portfolio has a Jensen's alpha of 0.82 percent, a beta of 1.40, and a CAPM expected return of 13.7 percent. The risk-free rate is 2.5 percent. What is the actual return of the portfolio?

(Multiple Choice)

4.7/5 (29)

High Mountain Homes has an expected annual return of 16.1 percent and a standard deviation of 22.3 percent. What is the smallest expected loss over the next month given a probability of 2.5 percent?

(Multiple Choice)

4.8/5 (41)

The Value-at-Risk measure assumes which one of the following?

(Multiple Choice)

4.8/5 (31)

Trailer Co. stock has an expected return of 11.8 percent and a standard deviation of 11.8 percent. What is the smallest expected loss over the next month given a probability of 5 percent?

(Multiple Choice)

4.9/5 (37)

Which one of the following statements is true concerning VaR?

(Multiple Choice)

4.8/5 (39)

Your portfolio actually earned 6.2 percent for the year. You were expecting to earn 8.6 percent based on the CAPM formula. What is Jensen's alpha if the portfolio standard deviation is 11.2 percent and the beta is .87?

(Multiple Choice)

4.8/5 (33)

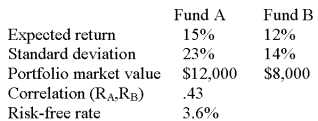

A portfolio consists of the following two funds.  What is the Sharpe ratio of the portfolio?

What is the Sharpe ratio of the portfolio?

(Multiple Choice)

4.8/5 (47)

A Sharpe-optimal portfolio provides which one of the following for a given set of securities?

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)