Exam 13: Performance Evaluation and Risk Management

Exam 1: A Brief History of Risk and Return100 Questions

Exam 2: The Investment Process100 Questions

Exam 3: Overview of Security Types94 Questions

Exam 4: Mutual Funds101 Questions

Exam 5: The Stock Market106 Questions

Exam 6: Common Stock Valuation104 Questions

Exam 7: Stock Price Behavior and Market Efficiency82 Questions

Exam 8: Behavioral Finance and the Psychology of Investing84 Questions

Exam 9: Interest Rates100 Questions

Exam 10: Bond Prices and Yields95 Questions

Exam 11: Diversification and Risky Asset Allocation84 Questions

Exam 12: Return, Risk, and the Security Market Line84 Questions

Exam 13: Performance Evaluation and Risk Management91 Questions

Exam 14: Futures Contracts97 Questions

Exam 15: Stock Options100 Questions

Exam 16: Option Valuation72 Questions

Exam 17: Projecting Cash Flow and Earnings100 Questions

Exam 18: Corporate Bonds85 Questions

Exam 19: Government Bonds84 Questions

Exam 20: Mortgage-Backed Securities92 Questions

Select questions type

Your portfolio has an expected return of 15.6 percent, a beta of 1.31, and a standard deviation of 15.3 percent. The U.S. Treasury bill rate is 3.8 percent. What is the Sharpe ratio of your portfolio?

(Multiple Choice)

4.9/5  (49)

(49)

Which one of the following concerns a money manager's control over investment risks, particularly potential short-run losses?

(Multiple Choice)

4.8/5 (31)

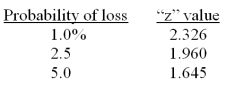

Your portfolio has a standard deviation of 12.3 percent and an average return of 10.6 percent. You have a 5 percent probability of losing _____ percent or more in any given year.

(Multiple Choice)

4.8/5 (37)

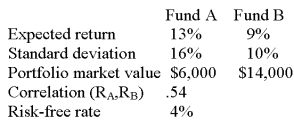

A portfolio consists of the following two funds.  What is the Sharpe ratio of the portfolio?

What is the Sharpe ratio of the portfolio?

(Multiple Choice)

4.8/5 (27)

A diversified portfolio has a beta of 1.47 and a raw return of 14.28 percent. The market return is 11.74 percent and the market risk premium is 7.85 percent. What is Jensen's alpha of the portfolio?

(Multiple Choice)

4.9/5 (28)

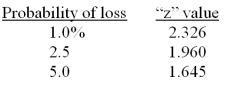

Which one of the following correctly states the VaR for a 3-year period with a 2.5 percent probability?

(Multiple Choice)

4.9/5 (38)

A portfolio has a 2.5 percent chance of losing 16 percent or more according to the VaR when T = 1. This can be interpreted to mean that the portfolio is expected to have an annual loss of 16 percent or more once in every how many years?

(Multiple Choice)

4.8/5 (39)

The U.S. Treasury bill is yielding 3.0 percent and the market has an expected return of 10.7 percent. What is the Sharpe ratio of a portfolio that has a beta of 1.32 and a variance of .027556?

(Multiple Choice)

4.8/5 (43)

You have a portfolio which has an average return of 12.6 percent. In any given year, you have a 2.5 percent probability of earning either a zero or a negative annual return. What is the approximate standard deviation of your portfolio?

(Multiple Choice)

4.8/5 (48)

Your portfolio has an expected annual return of 11.6 percent. What is the two-year expected return?

(Multiple Choice)

4.8/5 (45)

A portfolio has a beta of 1.52 and an actual return of 13.7 percent. The risk-free rate is 2.7 percent and the market risk premium is 7.8 percent. What is the value of Jensen's alpha?

(Multiple Choice)

4.9/5 (32)

A portfolio has an actual return of 15.17 percent, a beta of .93, and a standard deviation of 7.2 percent. The market return is 13.4 percent and the risk-free rate is 2.8 percent. What is the portfolio's Jensen's alpha?

(Multiple Choice)

4.8/5 (42)

A portfolio has an average return of 9.7 percent, a standard deviation of 8.6 percent, and a beta of .72. The risk-free rate is 2.1 percent. What is the Treynor ratio?

(Multiple Choice)

4.8/5 (34)

Mike's portfolio has a two-year expected return of 21.70 percent. What is the expected return for one year?

(Multiple Choice)

4.8/5 (43)

Which one of the following measures risk premium in relation to systematic risk?

(Multiple Choice)

4.9/5 (41)

A stock has a return of 16.18 percent and a beta of 1.47. The market return is 10.65 percent and the risk-free rate is 3.20 percent. What is the Jensen-Treynor alpha of this stock?

(Multiple Choice)

4.9/5 (39)

Which one of the following is a statistical model, defined by its mean and standard deviation, that is used to assess probabilities?

(Multiple Choice)

4.9/5 (35)

Which of the following should generally only be used to evaluate relatively diversified portfolios rather than individual securities?

I. Sharpe ratio

II. Treynor ratio

III. Jensen's alpha

(Multiple Choice)

4.9/5 (43)

A portfolio has a 3-year standard deviation of 20.20 percent. What is the one-year standard deviation?

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)