Exam 16: Alternative Exit and Restructuring Strategies: Divestitures, spin-Offs, carve-Outs, split-Ups, and Split-Offs

Exam 1: Introduction to Mergers, acquisitions, and Other Restructuring Activities108 Questions

Exam 2: The Regulatory Environment103 Questions

Exam 3: The Corporate Takeover Market: Common Takeover Tactics, anti-Takeover Defenses, and Corporate Governance126 Questions

Exam 4: Planning,developing Business,and Acquisition Plans: Phases 1 and 2 of the Acquisition Process109 Questions

Exam 5: Implementation: Search Through Closing: Phases 3 to 10 of the Acquisition Process106 Questions

Exam 6: Postclosing Integration: Mergers, acquisitions, and Business Alliances103 Questions

Exam 7: Merger and Acquisition Cash Flow Valuation Basics81 Questions

Exam 8: Relative,asset-Oriented,and Real Option Valuation Basics84 Questions

Exam 9: Applying Financial Models to Value, structure, and Negotiate Mergers and Acquisitions92 Questions

Exam 10: Analysis and Valuation of Privately Held Companies97 Questions

Exam 11: Structuring the Deal: Payment and Legal Considerations112 Questions

Exam 12: Structuring the Deal: Tax and Accounting Considerations97 Questions

Exam 13: Financing the Deal: Private Equity, hedge Funds, and Other Sources of Funds121 Questions

Exam 14: Highly Leveraged Transactions: Lbo Valuation and Modeling Basics98 Questions

Exam 15: Business Alliances: Joint Ventures, partnerships, strategic Alliances, and Licensing113 Questions

Exam 16: Alternative Exit and Restructuring Strategies: Divestitures, spin-Offs, carve-Outs, split-Ups, and Split-Offs119 Questions

Exam 17: Alternative Exit and Restructuring Strategies: Bankruptcy Reorganization and Liquidation80 Questions

Exam 18: Cross-Border Mergers and Acquisitions: Analysis and Valuation89 Questions

Select questions type

Management may sell assets to fund diversification opportunities?

(True/False)

4.8/5  (41)

(41)

In a spin-off,the board of directors is the same as the board of directors of the parent firm.

(True/False)

4.9/5 (34)

Viacom to Spin Off Blockbuster

After months of trying to sell its 81% stake in Blockbuster Inc. undertook a tax-free spin-off in mid 2004. Viacom shareholders will have the option to swap their Viacom shares for Blockbuster shares and a special cash payout. Blockbuster had been hurt by competition from low-priced rivals and the erosion of video rentals by accelerating DVD sales. Despite Blockbuster's steady contribution to Viacom's overall cash flow, Viacom believed that the growth prospects for the unit were severely limited. In preparation for the spin-off, Viacom had reported a $1.3 billion charge to earnings in the fourth quarter of 2003 in writing down goodwill associated with its acquisition of Blockbuster. By spinning off Blockbuster, Viacom Chairman and ECO Sumner Redstone statd that the firm would now be able to focus on its core TV (i.e., CBS and MTV) and movie (i.e., Paramount Studios) businesses. Blockbuster shares fell by 4% and Viacom shares rose by 1% on the day of the announcement.

:

-In your opinion,why did Viacom and Blockbuster share prices react the way they did to the announcement of the

spin-off?

(Essay)

4.9/5 (37)

Case Study Short Essay Examination Questions

Motorola Bows to Activist Pressure

Under pressure from activist investor Carl Icahn, Motorola felt compelled to make a dramatic move before its May 2008 shareholders' meeting. Icahn had submitted a slate of four directors to replace those up for reelection and demanded that the wireless handset and network manufacturer take actions to improve profitability. Shares of Motorola, which had a market value of $22 billion, had fallen more than 60% since October 2006, making the firm's board vulnerable in the proxy contest over director reelections.

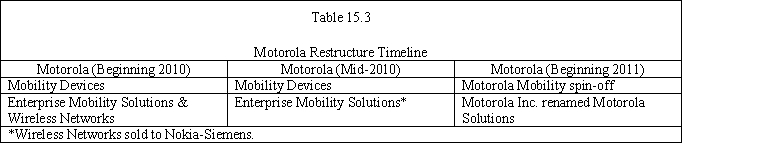

Signaling its willingness to take dramatic action, Motorola announced on March 26, 2008, its intention to create two independent, publicly traded companies. The two new companies would consist of the firm's former Mobile Devices operation (including its Home Devices businesses consisting of modems and set-top boxes) and its Enterprise Mobility Solutions & Wireless Networks business. In addition to the planned spin-off, Motorola agreed to nominate two people supported by Carl Icahn to the firm's board. Originally scheduled for 2009, the breakup was postponed due to the upheaval in the financial markets that year. The breakup would result in a tax-free distribution to Motorola's shareholders, with shareholders receiving shares of the two independent and publicly traded firms.

The Mobile Devices business designs, manufactures, and sells mobile handsets globally, and it has lost more than $5 billion during the last three years. The Enterprise Mobility Solutions & Wireless Networks business manufactures, designs, and services public safety radios, handheld scanners and telecommunications network gear for businesses and government agencies and generates nearly all of the Motorola's current cash flow. This business also makes network equipment for wireless carriers such as Spring Nextel and Verizon Wireless.

By dividing the company in this manner, Motorola would separate its loss-generating Mobility Devices division from its other businesses. Although the third largest handset manufacturer globally, the handset business had been losing market share to Nokia and Samsung Electronics for years. Following the breakup, the Mobility Devices unit would be renamed Motorola Mobility, and the Enterprise Mobility Solutions & Networks operation would be called Motorola Solutions.

Motorola's board is seeking to ensure the financial viability of Motorola Mobility by eliminating its outstanding debt and through a cash infusion. To do so, Motorola intends to buy back nearly all of its outstanding $3.9 billion debt and to transfer as much as $4 billion in cash to Motorola Mobility. Furthermore, Motorola Solutions would assume responsibility for the pension obligations of Motorola Mobility. If Motorola Mobility were to be forced into bankruptcy shortly after the breakup, Motorola Solutions may be held legally responsible for some of the business's liabilities. The court would have to prove that Motorola had conveyed the Mobility Devices unit (renamed Motorola Mobility following the breakup) to its shareholders, fraudulently knowing that the unit's financial viability was problematic.

Once free of debt and other obligations and flush with cash, Motorola Mobility would be in a better position to make acquisitions and to develop new phones. It would also be more attractive as a takeover target. A stand-alone firm is unencumbered by intercompany relationships, including such things as administrative support or parts and services supplied by other areas of Motorola. Moreover, all liabilities and assets associated with the handset business already would have been identified, making it easier for a potential partner to value the business.

In mid-2010, Motorola Inc. announced that it had reached an agreement with Nokia Siemens Networks, a Finnish-German joint venture, to buy the wireless networks operations, formerly part of its Enterprise Mobility Solutions & Wireless Network Devices business for $1.2 billion. On January 4, 2011, Motorola Inc. spun off the common shares of Motorola Mobility it held as a tax-free dividend to its shareholders and renamed the firm Motorola Solutions. Each shareholder of record as of December 21, 2010, would receive one share of Motorola Mobility common for every eight shares of Motorola Inc. common stock they held. Table 15.3 shows the timeline of Motorola's restructuring effort.

1.In your judgment, did the breakup of Motorola make sense? Explain your answer.

2.What other restructuring alternatives could Motorola have pursued to increase shareholder value? Why do you believe it pursued this breakup strategy rather than some other option?  -There is often a natural tension between so-called activist investors interested in short-term profits and a firm's management interested in pursuing a longer-term vision.When is this tension helpful to shareholders and when does it destroy shareholder value?

-There is often a natural tension between so-called activist investors interested in short-term profits and a firm's management interested in pursuing a longer-term vision.When is this tension helpful to shareholders and when does it destroy shareholder value?

(Essay)

4.8/5 (39)

In general,a voluntary bust-up or liquidation has the advantage over mergers of deferring the recognition of a gain by the stockholders of the selling company until they eventually sell the stock.

(True/False)

4.8/5 (40)

AT&T (1984 - 2005)-A POSTER CHILD

FOR RESTRUCTURING GONE AWRY

Between 1984 and 2000, AT&T underwent four major restructuring programs. These included the government-mandated breakup in 1984, the 1996 effort to eliminate customer conflicts, the 1998 plan to become a broadband powerhouse, and the most recent restructuring program announced in 2000 to correct past mistakes. It is difficult to identify another major corporation that has undergone as much sustained trauma as AT&T. Ironically, a former AT&T operating unit acquired its former parent in 2005.

The 1984 Restructure: Changed the Organization But Not the Culture

The genesis of Ma Bell's problems may have begun with the consent decree signed with the Department of Justice in 1984, which resulted in the spin-off of its local telephone operations to its shareholders. AT&T retained its long-distance and telecommunications equipment manufacturing operations. Although the breadth of the firm's product offering changed dramatically, little else seems to have changed. The firm remained highly bureaucratic, risk averse, and inward looking. However, substantial market share in the lucrative long-distance market continued to generate huge cash flow for the company, thereby enabling the company to be slow to react to the changing competitive dynamics of the marketplace.

The 1996 Restructure: Lack of a Coherent Strategy

Cash accumulated from the long-distance business was spent on a variety of ill-conceived strategies such as the firm's foray into the personal computer business. After years of unsuccessfully attempting to redefine the company's strategy, AT&T once again resorted to a major restructure of the firm. In 1996, AT&T spun-off Lucent Technologies (its telecommunications equipment business) and NCR (a computer services business) to shareholders to facilitate Lucent equipment sales to former AT&T operations and to eliminate the non-core NCR computer business. However, this had little impact on the AT&T share price.

The 1998 Restructure: Vision Exceeds Ability to Execute

In its third major restructure since 1984, AT&T CEO Michael Armstrong passionately unveiled in June of 1998 a daring strategy to transform AT&T from a struggling long-distance telephone company into a broadband internet access and local phone services company. To accomplish this end, he outlined his intentions to acquire cable companies MediaOne Group and Telecommunications Inc. for $58 billion and $48 billion, respectively. The plan was to use cable-TV networks to deliver the first fully integrated package of broadband internet access and local phone service via the cable-TV network.

AT&T Could Not Handle Its Early Success

During the next several years, Armstrong seemed to be up to the task, cutting sales, general, and administrative expense's share of revenue from 28 percent to 20 percent, giving AT&T a cost structure comparable to its competitors. He attempted to change the bureaucratic culture to one able to compete effectively in the deregulated environment of the post-1996 Telecommunications Act by issuing stock options to all employees, tying compensation to performance, and reducing layers of managers. He used AT&T's stock, as well as cash, to buy the cable companies before the decline in AT&T's long-distance business pushed the stock into a free fall. He also transformed AT&T Wireless from a collection of local businesses into a national business.

Notwithstanding these achievements, AT&T experienced major missteps. Employee turnover became a big problem, especially among senior managers. Armstrong also bought Telecommunications and MediaOne when valuations for cable-television assets were near their peak. He paid about $106 billion in 2000, when they were worth about $80 billion. His failure to cut enough deals with other cable operators (e.g., Time Warner) to sell AT&T's local phone service meant that AT&T could market its services only in regional markets rather than on a national basis. In addition, AT&T moved large corporate customers to its Concert joint venture with British Telecom, alienating many AT&T salespeople, who subsequently quit. As a result, customer service deteriorated rapidly and major customers defected. Finally, Armstrong seriously underestimated the pace of erosion in AT&T's long-distance revenue base.

AT&T May Have Become Overwhelmed by the Rate of Change

What happened? Perhaps AT&T fell victim to the same problems many other acquisitive companies have. AT&T is a company capable of exceptional vision but incapable of effective execution. Effective execution involves buying or building assets at a reasonable cost. Its substantial overpayment for its cable acquisitions meant that it would be unable to earn the returns required by investors in what they would consider a reasonable period. Moreover, Armstrong's efforts to shift from the firm's historical business by buying into the cable-TV business through acquisition had saddled the firm with $62 billion in debt.

AT&T tried to do too much too quickly. New initiatives such as high-speed internet access and local telephone services over cable-television network were too small to pick up the slack. Much time and energy seems to have gone into planning and acquiring what were viewed as key building blocks to the strategy. However, there appears to have been insufficient focus and realism in terms of the time and resources required to make all the pieces of the strategy fit together. Some parts of the overall strategy were at odds with other parts. For example, AT&T undercut its core long-distance wired telephone business by offers of free long-distance wireless to attract new subscribers. Despite aggressive efforts to change the culture, AT&T continued to suffer from a culture that evolved in the years before 1996 during which the industry was heavily regulated. That atmosphere bred a culture based on consensus building, ponderously slow decision-making, and a low tolerance for risk. Consequently, the AT&T culture was unprepared for the fiercely competitive deregulated environment of the late 1990s (Truitt, 2001).

Furthermore, AT&T created individual tracking stocks for AT&T Wireless and for Liberty Media. The intention of the tracking stocks was to link the unit's stock to its individual performance, create a currency for the unit to make acquisitions, and to provide a new means of motivating the unit's management by giving them stock in their own operation. Unlike a spin-off, AT&T's board continued to exert direct control over these units. In an IPO in April 2000, AT&T sold 14 percent of AT&T's Wireless tracking stock to the public to raise funds and to focus investor attention on the true value of the Wireless operations.

Investors Lose Patience

Although all of these actions created a sense that grandiose change was imminent, investor patience was wearing thin. Profitability foundered. The market share loss in its long-distance business accelerated. Although cash flow remained strong, it was clear that a cash machine so dependent on the deteriorating long-distance telephone business soon could grind to a halt. Investors' loss of faith was manifested in the sharp decline in AT&T stock that occurred in 2000.

The 2000 Restructure: Correcting the Mistakes of the Past

Pushed by investor impatience and a growing realization that achieving AT&T's vision would be more time and resource consuming than originally believed, Armstrong announced on October 25, 2000 the breakup of the business for the fourth time. The plan involved the creation of four new independent companies including AT&T Wireless, AT&T Consumer, AT&T Broadband, and Liberty Media.

By breaking the company into specific segments, AT&T believed that individual units could operate more efficiently and aggressively. AT&T's consumer long-distance business would be able to enter the digital subscriber line (DSL) market. DSL is a broadband technology based on the telephone wires that connect individual homes with the telephone network. AT&T's cable operations could continue to sell their own fast internet connections and compete directly against AT&T's long-distance telephone business. Moreover, the four individual businesses would create "pure-play" investor opportunities. Specifically, AT&T proposed splitting off in early 2001 AT&T Wireless and issuing tracking stocks to the public in late 2001 for AT&T's Consumer operations, including long-distance and Worldnet Internet service, and AT&T's Broadband (cable) operations. The tracking shares would later be converted to regular AT&T common shares as if issued by AT&T Broadband, making it an independent entity. AT&T would retain AT&T Business Services (i.e., AT&T Lab and Telecommunications Network) with the surviving AT&T entity. Investor reaction was swift and negative. Not swayed by the proposal, investors caused the stock to drop 13 percent in a single day. Moreover, it ended 2000 at 17 ½, down 66 percent from the beginning of the year.

The More Things Change The More They Stay The Same

On July 10, 2001, AT&T Wireless Services became an independent company, in accordance with plans announced during the 2000 restructure program. AT&T Wireless became a separate company when AT&T converted the tracking shares of the mobile-phone business into common stock and split-off the unit from the parent. AT&T encouraged shareholders to exchange their AT&T common shares for Wireless common shares by offering AT&T shareholders 1.176 Wireless shares for each share of AT&T common. The exchange ratio represented a 6.5 percent premium over AT&T's current common share price. AT&T Wireless shares have fallen 44 percent since AT&T first sold the tracking stock in April 2000. On August 10, 2001, AT&T spun off Liberty Media.

After extended discussions, AT&T agreed on December 21, 2001 to merge its broadband unit with Comcast to create the largest cable television and high-speed internet service company in the United States. Without the future growth engine offered by Broadband and Wireless, AT&T's remaining long-distance businesses and business services operations had limited growth prospects. After a decade of tumultuous change, AT&T was back where it was at the beginning of the 1990s. At about $15 billion in late 2004, AT&T's market capitalization was about one-sixth of that of such major competitors as Verizon and SBC. SBC Communications (a former local AT&T operating company) acquired AT&T on November 18, 2005 in a $16 billion deal and promptly renamed the combined firms AT&T.

-Was AT&T proactive or reactive in initiating its 2000 restructuring program? Explain your answer.

(Essay)

4.8/5 (37)

Equity carve-outs are similar to divestitures and spin-offs in that they provide a cash infusion to the parent.

(True/False)

4.8/5 (37)

In a spin-off,the proportional ownership of shares in the new legal subsidiary is the same as the stockholders' proportional ownership of shares in the parent firm.

(True/False)

4.9/5 (33)

Equity ownership changes in spin-offs,but it does not change in split-ups.

(True/False)

4.9/5 (37)

Empirical studies show that the desire by parent firms to increase strategic focus is an important motive for exiting businesses.

(True/False)

4.9/5 (33)

For a spin-off to be tax-free to the shareholder it must satisfy which of the following:

(Multiple Choice)

4.7/5 (33)

The divestiture of a business always results in the parent receiving cash from the buyer?

(True/False)

4.9/5 (35)

In an equity carve-out,the cash raised by the subsidiary in this manner may be transferred to the parent as a dividend or as an inter-company loan.

(True/False)

4.8/5 (36)

Which of the following is generally considered a motive for exiting businesses?

(Multiple Choice)

4.9/5 (39)

The board of directors of a large conglomerate has decided that the investment opportunities for the firm are limited and that greater value could be created for the shareholders if the firm were divided into four independent businesses.Following approval by shareholders,the firm executed this strategy which is best described as a

(Multiple Choice)

4.9/5 (38)

A spin-off is tax free to the shareholders if it is properly structured.In contrast,the cash proceeds from an outright sale may be taxable to the parent to the extent a gain is realized.

(True/False)

4.8/5 (42)

Which of the following is generally not considered a common motive for exiting businesses?

(Multiple Choice)

4.8/5 (39)

A firm decides to distribute all of the shares it holds in a subsidiary to its shareholders.The distribution would be called a

(Multiple Choice)

4.8/5 (37)

USX Bows to Shareholder Pressure to Split Up the Company

As one of the first firms to issue tracking stocks in the mid-1980s, USX relented to ongoing shareholder pressure to divide the firm into two pieces. After experiencing a sharp "boom/bust" cycle throughout the 1970s, U.S. Steel had acquired Marathon Oil, a profitable oil and gas company, in 1982 in what was at the time the second largest merger in U.S. history. Marathon had shown steady growth in sales and earnings throughout the 1970s. USX Corp. was formed in 1986 as the holding company for both U.S. Steel and Marathon Oil. In 1991, USX issued its tracking stocks to create "pure plays" in its primary businesses-steel and oil-and to utilize USX's steel losses, which could be used to reduce Marathon's taxable income. Marathon shareholders have long complained that Marathon's stock was selling at a discount to its peers because of its association with USX. The campaign to split Marathon from U.S. Steel began in earnest in early 2000.

On April 25, 2001, USX announced its intention to split U.S. Steel and Marathon Oil into two separately traded companies. The breakup gives holders of Marathon Oil stock an opportunity to participate in the ongoing consolidation within the global oil and gas industry. Holders of USX-U.S. Steel Group common stock (target stock) would become holders of newly formed Pittsburgh-based United States Steel Corporation, a return to the original name of the firm formed in 1901. Under the reorganization plan, U.S. Steel and Marathon would retain the same assets and liabilities already associated with each business. However, Marathon will assume $900 million in debt from U.S. Steel, leaving the steelmaker with $1.3 billion of debt. This assumption of debt by Marathon is an attempt to make U.S. Steel, which continued to lose money until 2004, able to stand on its own financially.

The investor community expressed mixed reactions, believing that Marathon would be likely to benefit from a possible takeover attempt, whereas U.S. Steel would not fare as well. Despite the initial investor pessimism, investors in both Marathon and U.S. Steel saw their shares appreciate significantly in the years immediately following the breakup.

:

:

-In your judgment,did the breakup of USX into Marathon Oil and United States Steel

Corporation make sense? Why or why not?

(Essay)

4.9/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)