Exam 16: Alternative Exit and Restructuring Strategies: Divestitures, spin-Offs, carve-Outs, split-Ups, and Split-Offs

Exam 1: Introduction to Mergers, acquisitions, and Other Restructuring Activities108 Questions

Exam 2: The Regulatory Environment103 Questions

Exam 3: The Corporate Takeover Market: Common Takeover Tactics, anti-Takeover Defenses, and Corporate Governance126 Questions

Exam 4: Planning,developing Business,and Acquisition Plans: Phases 1 and 2 of the Acquisition Process109 Questions

Exam 5: Implementation: Search Through Closing: Phases 3 to 10 of the Acquisition Process106 Questions

Exam 6: Postclosing Integration: Mergers, acquisitions, and Business Alliances103 Questions

Exam 7: Merger and Acquisition Cash Flow Valuation Basics81 Questions

Exam 8: Relative,asset-Oriented,and Real Option Valuation Basics84 Questions

Exam 9: Applying Financial Models to Value, structure, and Negotiate Mergers and Acquisitions92 Questions

Exam 10: Analysis and Valuation of Privately Held Companies97 Questions

Exam 11: Structuring the Deal: Payment and Legal Considerations112 Questions

Exam 12: Structuring the Deal: Tax and Accounting Considerations97 Questions

Exam 13: Financing the Deal: Private Equity, hedge Funds, and Other Sources of Funds121 Questions

Exam 14: Highly Leveraged Transactions: Lbo Valuation and Modeling Basics98 Questions

Exam 15: Business Alliances: Joint Ventures, partnerships, strategic Alliances, and Licensing113 Questions

Exam 16: Alternative Exit and Restructuring Strategies: Divestitures, spin-Offs, carve-Outs, split-Ups, and Split-Offs119 Questions

Exam 17: Alternative Exit and Restructuring Strategies: Bankruptcy Reorganization and Liquidation80 Questions

Exam 18: Cross-Border Mergers and Acquisitions: Analysis and Valuation89 Questions

Select questions type

Case Study Short Essay Examination Questions

Motorola Bows to Activist Pressure

Under pressure from activist investor Carl Icahn, Motorola felt compelled to make a dramatic move before its May 2008 shareholders' meeting. Icahn had submitted a slate of four directors to replace those up for reelection and demanded that the wireless handset and network manufacturer take actions to improve profitability. Shares of Motorola, which had a market value of $22 billion, had fallen more than 60% since October 2006, making the firm's board vulnerable in the proxy contest over director reelections.

Signaling its willingness to take dramatic action, Motorola announced on March 26, 2008, its intention to create two independent, publicly traded companies. The two new companies would consist of the firm's former Mobile Devices operation (including its Home Devices businesses consisting of modems and set-top boxes) and its Enterprise Mobility Solutions & Wireless Networks business. In addition to the planned spin-off, Motorola agreed to nominate two people supported by Carl Icahn to the firm's board. Originally scheduled for 2009, the breakup was postponed due to the upheaval in the financial markets that year. The breakup would result in a tax-free distribution to Motorola's shareholders, with shareholders receiving shares of the two independent and publicly traded firms.

The Mobile Devices business designs, manufactures, and sells mobile handsets globally, and it has lost more than $5 billion during the last three years. The Enterprise Mobility Solutions & Wireless Networks business manufactures, designs, and services public safety radios, handheld scanners and telecommunications network gear for businesses and government agencies and generates nearly all of the Motorola's current cash flow. This business also makes network equipment for wireless carriers such as Spring Nextel and Verizon Wireless.

By dividing the company in this manner, Motorola would separate its loss-generating Mobility Devices division from its other businesses. Although the third largest handset manufacturer globally, the handset business had been losing market share to Nokia and Samsung Electronics for years. Following the breakup, the Mobility Devices unit would be renamed Motorola Mobility, and the Enterprise Mobility Solutions & Networks operation would be called Motorola Solutions.

Motorola's board is seeking to ensure the financial viability of Motorola Mobility by eliminating its outstanding debt and through a cash infusion. To do so, Motorola intends to buy back nearly all of its outstanding $3.9 billion debt and to transfer as much as $4 billion in cash to Motorola Mobility. Furthermore, Motorola Solutions would assume responsibility for the pension obligations of Motorola Mobility. If Motorola Mobility were to be forced into bankruptcy shortly after the breakup, Motorola Solutions may be held legally responsible for some of the business's liabilities. The court would have to prove that Motorola had conveyed the Mobility Devices unit (renamed Motorola Mobility following the breakup) to its shareholders, fraudulently knowing that the unit's financial viability was problematic.

Once free of debt and other obligations and flush with cash, Motorola Mobility would be in a better position to make acquisitions and to develop new phones. It would also be more attractive as a takeover target. A stand-alone firm is unencumbered by intercompany relationships, including such things as administrative support or parts and services supplied by other areas of Motorola. Moreover, all liabilities and assets associated with the handset business already would have been identified, making it easier for a potential partner to value the business.

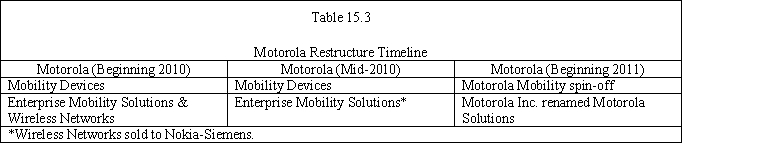

In mid-2010, Motorola Inc. announced that it had reached an agreement with Nokia Siemens Networks, a Finnish-German joint venture, to buy the wireless networks operations, formerly part of its Enterprise Mobility Solutions & Wireless Network Devices business for $1.2 billion. On January 4, 2011, Motorola Inc. spun off the common shares of Motorola Mobility it held as a tax-free dividend to its shareholders and renamed the firm Motorola Solutions. Each shareholder of record as of December 21, 2010, would receive one share of Motorola Mobility common for every eight shares of Motorola Inc. common stock they held. Table 15.3 shows the timeline of Motorola's restructuring effort.

1.In your judgment, did the breakup of Motorola make sense? Explain your answer.

2.What other restructuring alternatives could Motorola have pursued to increase shareholder value? Why do you believe it pursued this breakup strategy rather than some other option?  -What does the decision to split up the firm say about Kraft's decision to buy Cadbury in 2010?

-What does the decision to split up the firm say about Kraft's decision to buy Cadbury in 2010?

(Essay)

5.0/5  (43)

(43)

Hughes Corporation's Dramatic Transformation

In one of the most dramatic redirections of corporate strategy in U.S. history, Hughes Corporation transformed itself from a defense industry behemoth into the world's largest digital information and communications company. Once California's largest manufacturing employer, Hughes Corporation built spacecraft, the world's first working laser, communications satellites, radar systems, and military weapons systems. However, by the late 1990s, the firm had undergone substantial gut-wrenching change to reposition the firm in what was viewed as a more attractive growth opportunity. This transformation culminated in the firm being acquired in 2004 by News Corp., a global media empire.

To accomplish this transformation, Hughes divested its communications satellite businesses and its auto electronics operation. The corporate overhaul created a firm focused on direct-to-home satellite broadcasting with its DirecTV service offering. DirecTV's introduction to nearly 12 million U.S. homes was a technology made possible by U.S. military spending during the early 1980s. Although military spending had fueled much of Hughes' growth during the decade of the 1980s, it was becoming increasingly clear by 1988 that the level of defense spending of the Reagan years was coming to a close with the winding down of the cold war.

For the next several years, Hughes attempted to find profitable niches in the rapidly consolidating U.S. defense contracting industry. Hughes acquired General Dynamics' missile business and made 15 smaller defense-related acquisitions. Eventually, Hughes' parent firm, General Motors, lost enthusiasm for additional investment in defense-related businesses. GM decided that, if Hughes could not participate in the shrinking defense industry, there was no reason to retain any interests in the industry at all. In November 1995, Hughes initiated discussions with Raytheon, and two years later, it sold its aerospace and defense business to Raytheon for $9.8 billion. The firm also merged its Delco product line with GM's Delphi automotive systems. What remained was the firm's telecommunications division. Hughes had transformed itself from a $16 billion defense contractor to a svelte $4 billion telecommunications business.

Hughes' telecommunications unit was its smallest operation but, with DirecTV, its fastest growing. The transformation was to exact a huge cultural toll on Hughes' employees, most of whom had spent their careers dealing with the U.S. Department of Defense. Hughes moved to hire people aggressively from the cable and broadcast businesses. By the late 1990s, former Hughes' employees constituted only 15-20 percent of DirecTV's total employees.

Restructuring continued through the end of the 1990s. In 2000, Hughes sold its satellite manufacturing operations to Boeing for $3.75 billion. This eliminated the last component of the old Hughes and cut its workforce in half. In December 2000, Hughes paid about $180 million for Telocity, a firm that provides digital subscriber line service through phone lines. This acquisition allowed Hughes to provide high-speed Internet connections through its existing satellite service, mainly in more remote rural areas, as well as phone lines targeted at city dwellers. Hughes now could market the same combination of high-speed Internet services and video offered by cable providers, Hughes' primary competitor.

In need of cash, GM put Hughes up for sale in late 2000, expressing confidence that there would be a flood of lucrative offers. However, the faltering economy and stock market resulted in GM receiving only one serious bid, from media tycoon Rupert Murdoch of News Corp. in February 2001. But, internal discord within Hughes and GM over the possible buyer of Hughes Electronics caused GM to backpedal and seek alternative bidders. In late October 2001, GM agreed to sell its Hughes Electronics subsidiary and its DirecTV home satellite network to EchoStar Communication for $25.8 billion. However, regulators concerned about the antitrust implications of the deal disallowed this transaction. In early 2004, News Corp., General Motors, and Hughes reached a definitive agreement in which News Corp acquired GM's 19.9 percent stake in Hughes and an additional 14.1 percent of Hughes from public shareholders and GM's pension and other benefit plans. News Corp. paid about $14 per share, making the deal worth about $6.6 billion for 34.1 percent of Hughes. The implied value of 100 percent of Hughes was, at that time, $19.4 billion, about three fourths of EchoStar's valuation three years earlier.

Case Study :

-Why did Hughes move so aggressively to hire employees from the cable TV and broadcast industry?

(Essay)

4.9/5 (45)

USX Bows to Shareholder Pressure to Split Up the Company

As one of the first firms to issue tracking stocks in the mid-1980s, USX relented to ongoing shareholder pressure to divide the firm into two pieces. After experiencing a sharp "boom/bust" cycle throughout the 1970s, U.S. Steel had acquired Marathon Oil, a profitable oil and gas company, in 1982 in what was at the time the second largest merger in U.S. history. Marathon had shown steady growth in sales and earnings throughout the 1970s. USX Corp. was formed in 1986 as the holding company for both U.S. Steel and Marathon Oil. In 1991, USX issued its tracking stocks to create "pure plays" in its primary businesses-steel and oil-and to utilize USX's steel losses, which could be used to reduce Marathon's taxable income. Marathon shareholders have long complained that Marathon's stock was selling at a discount to its peers because of its association with USX. The campaign to split Marathon from U.S. Steel began in earnest in early 2000.

On April 25, 2001, USX announced its intention to split U.S. Steel and Marathon Oil into two separately traded companies. The breakup gives holders of Marathon Oil stock an opportunity to participate in the ongoing consolidation within the global oil and gas industry. Holders of USX-U.S. Steel Group common stock (target stock) would become holders of newly formed Pittsburgh-based United States Steel Corporation, a return to the original name of the firm formed in 1901. Under the reorganization plan, U.S. Steel and Marathon would retain the same assets and liabilities already associated with each business. However, Marathon will assume $900 million in debt from U.S. Steel, leaving the steelmaker with $1.3 billion of debt. This assumption of debt by Marathon is an attempt to make U.S. Steel, which continued to lose money until 2004, able to stand on its own financially.

The investor community expressed mixed reactions, believing that Marathon would be likely to benefit from a possible takeover attempt, whereas U.S. Steel would not fare as well. Despite the initial investor pessimism, investors in both Marathon and U.S. Steel saw their shares appreciate significantly in the years immediately following the breakup.

:

:

-Why do you think USX issued separate tracking stocks for its oil and steel businesses?

(Essay)

4.8/5 (34)

Which of the following is a common problem associated with tracking stocks?

(Multiple Choice)

4.9/5 (32)

A split-up involves carving out a portion of the equity of each of the parent's operating subsidiaries and selling the shares to the public.

(True/False)

4.9/5 (41)

Sara Lee Attempts to Create Value through Restructuring

After spurning a series of takeover offers, Sara Lee, a global consumer goods company, announced in early 2011 its intention to split the firm into two separate publicly traded companies. The two companies would consist of the firm's North American retail and food service division and its international beverage business. The announcement comes after a long string of restructuring efforts designed to increase shareholder value. It remains to be seen if the latest effort will be any more successful than earlier efforts.

Reflecting a flawed business strategy, Sara Lee had struggled for more than a decade to create value for its shareholders by radically restructuring its portfolio of businesses. The firm's business strategy had evolved from one designed in the mid-1980s to market a broad array of consumer products from baked goods to coffee to underwear under the highly recognizable brand name of Sara Lee into one that was designed to refocus the firm on the faster-growing food and beverage and apparel businesses. Despite acquiring several European manufacturers of processed meats in the early 1990s, the company's profits and share price continued to flounder.

In September 1997, Sara Lee embarked on a major restructuring effort designed to boost both profits, which had been growing by about 6% during the previous five years, and the company's lagging share price. The restructuring program was intended to reduce the firm's degree of vertical integration, shifting from a manufacturing and sales orientation to one focused on marketing the firm's top brands. The firm increasingly viewed itself as more of a marketing than a manufacturing enterprise.

Sara Lee outsourced or sold 110 manufacturing and distribution facilities over the next two years. Nearly 10,000 employees, representing 7% of the workforce, were laid off. The proceeds from the sale of facilities and the cost savings from outsourcing were either reinvested in the firm's core food businesses or used to repurchase $3 billion in company stock. 1n 1999 and 2000, the firm acquired several brands in an effort to bolster its core coffee operations, including such names as Chock Full o'Nuts, Hills Bros, and Chase & Sanborn.

Despite these restructuring efforts, the firm's stock price continued to drift lower. In an attempt to reverse the firm's misfortunes, the firm announced an even more ambitious restructuring plan in 2000. Sara Lee would focus on three main areas: food and beverages, underwear, and household products. The restructuring efforts resulted in the shutdown of a number of meat packing plants and a number of small divestitures, resulting in a 10% reduction (about 13,000 people) in the firm's workforce. Sara Lee also completed the largest acquisition in its history, purchasing The Earthgrains Company for $1.9 billion plus the assumption of $0.9 billion in debt. With annual revenue of $2.6 billion, Earthgrains specialized in fresh packaged bread and refrigerated dough. However, despite ongoing restructuring activities, Sara Lee continued to underperform the broader stock market indices.

In February 2005, Sara Lee executed its most ambitious plan to transform the firm into a company focused on the global food, beverage, and household and body care businesses. To this end, the firm announced plans to dispose of 40% of its revenues, totaling more than $8 billion, including its apparel, European packaged meats, U.S. retail coffee, and direct sales businesses.

In 2006, the firm announced that it had completed the sale of its branded apparel business in Europe, Global Body Care and European Detergents units, and its European meat processing operations. Furthermore, the firm spun off its U.S. Branded Apparel unit into a separate publicly traded firm called HanesBrands Inc. The firm raised more than $3.7 billion in cash from the divestitures. The firm was now focused on its core businesses: food, beverages, and household and body care.

In late 2008, Sara Lee announced that it would close its kosher meat processing business and sold its retail coffee business. In 2009, the firm sold its Household and Body Care business to Unilever for $1.6 billion and its hair care business to Procter & Gamble for $0.4 billion.

In 2010, the proceeds of the divestitures made the prior year were used to repurchase $1.3 billion of Sara Lee's outstanding shares. The firm also announced its intention to repurchase another $3 billion of its shares during the next three years. If completed, this would amount to about one-third of its approximate $10 billion market capitalization at the end of 2010.

What remains of the firm are food brands in North America, including Hillshire Farm, Ball Park, and Jimmy Dean processed meats and Sara Lee baked goods and Earthgrains. A food distribution unit will also remain in North America, as will its beverage and bakery operations. Sara Lee is rapidly moving to become a food, beverage, and bakery firm. As it becomes more focused, it could become a takeover target.

Has the 2005 restructuring program worked? To answer this question, it is necessary to determine the percentage change in Sara Lee's share price from the announcement date of the restructuring program to the end of 2010, as well as the percentage change in the share price of HanesBrands Inc., which was spun off on August 18, 2006. Sara Lee shareholders of record received one share of HanesBrands Inc. for every eight Sara Lee shares they held.

Sara Lee's share price jumped by 6% on the February 21, 2004 announcement date, closing at $19.56. Six years later, the stock price ended 2010 at $14.90, an approximate 24% decline since the announcement of the restructuring program in early 2005. Immediately following the spinoff, HanesBrands' stock traded at $22.06 per share; at the end of 2010, the stock traded at $25.99, a 17.8% increase.

A shareholder owning 100 Sara Lee shares when the spin-off was announced would have been entitled to 12.5 HanesBrands shares. However, they would have actually received 12 shares plus $11.03 for fractional shares .

A shareholder of record who had 100 Sara Lee shares on the announcement date of the restructuring program and held their shares until the end of 2010 would have seen their investment decline 24% from $1,956 (100 shares × $19.56 per share) to $1,486.56 by the end of 2010. However, this would have been partially offset by the appreciation of the HanesBrands shares between 2006 and 2010. Therefore, the total value of the hypothetical shareholder's investment would have decreased by 7.5% from $1,956 to $1,809.47 . This compares to a more modest 5% loss for investors who put the same $1,956 into a Standard & Poor's 500 stock index fund during the same period.

Why did Sara Lee underperform the broader stock market indices during this period? Despite the cumulative buyback of more than $4 billion of its outstanding stock, Sara Lee's fully diluted earnings per share dropped from $0.90 per share in 2005 to $0.52 per share in 2009. Furthermore, the book value per share, a proxy for the breakup or liquidation value of the firm, dropped from $3.28 in 2005 to $2.93 in 2009, reflecting the ongoing divestiture program. While the HanesBrands spin-off did create value for the shareholder, the amount was far too modest to offset the decline in Sara Lee's market value. During the same period, total revenue grew at a tepid average annual rate of about 3% to about $13 billion in 2009.

Case Study :

-Would you expect investors to be better off buying Sara Lee stock or investing in a similar set of consumer product businesses in their own personal investment portfolios? Explain your answer.

(Essay)

4.9/5 (40)

USX Bows to Shareholder Pressure to Split Up the Company

As one of the first firms to issue tracking stocks in the mid-1980s, USX relented to ongoing shareholder pressure to divide the firm into two pieces. After experiencing a sharp "boom/bust" cycle throughout the 1970s, U.S. Steel had acquired Marathon Oil, a profitable oil and gas company, in 1982 in what was at the time the second largest merger in U.S. history. Marathon had shown steady growth in sales and earnings throughout the 1970s. USX Corp. was formed in 1986 as the holding company for both U.S. Steel and Marathon Oil. In 1991, USX issued its tracking stocks to create "pure plays" in its primary businesses-steel and oil-and to utilize USX's steel losses, which could be used to reduce Marathon's taxable income. Marathon shareholders have long complained that Marathon's stock was selling at a discount to its peers because of its association with USX. The campaign to split Marathon from U.S. Steel began in earnest in early 2000.

On April 25, 2001, USX announced its intention to split U.S. Steel and Marathon Oil into two separately traded companies. The breakup gives holders of Marathon Oil stock an opportunity to participate in the ongoing consolidation within the global oil and gas industry. Holders of USX-U.S. Steel Group common stock (target stock) would become holders of newly formed Pittsburgh-based United States Steel Corporation, a return to the original name of the firm formed in 1901. Under the reorganization plan, U.S. Steel and Marathon would retain the same assets and liabilities already associated with each business. However, Marathon will assume $900 million in debt from U.S. Steel, leaving the steelmaker with $1.3 billion of debt. This assumption of debt by Marathon is an attempt to make U.S. Steel, which continued to lose money until 2004, able to stand on its own financially.

The investor community expressed mixed reactions, believing that Marathon would be likely to benefit from a possible takeover attempt, whereas U.S. Steel would not fare as well. Despite the initial investor pessimism, investors in both Marathon and U.S. Steel saw their shares appreciate significantly in the years immediately following the breakup.

:

:

-What other alternatives could USX have pursued to increase shareholder value? Why do you believe they pursued the breakup strategy rather than some of the alternatives?

(Essay)

4.9/5 (38)

To decide if a business is worth more to the shareholder if sold,the parent firm generally considers all of the following factors except for

(Multiple Choice)

4.9/5 (40)

The board of directors of a firm approves an exchange offer in which their shareholders are offered stock in one of the firm's subsidiaries in exchange for their holdings of parent company stock.This offer is best described as a

(Multiple Choice)

4.8/5 (37)

A substantial body of evidence indicates that increasing a firm's degree of diversification can improve substantially financial returns to shareholders.

(True/False)

4.8/5 (41)

Hewlett Packard Spins Out Its Agilent Unit in a Staged Transaction

Hewlett Packard (HP) announced the spin-off of its Agilent Technologies unit to focus on its main business of computers and printers, where sales have been lagging behind such competitors as Sun Microsystems. Agilent makes test, measurement, and monitoring instruments; semiconductors; and optical components. It also supplies patient-monitoring and ultrasound-imaging equipment to the health care industry. HP will retain an 85% stake in the company. The cash raised through the 15% equity carve-out will be paid to HP as a dividend from the subsidiary to the parent. Hewlett Packard will provide Agilent with $983 million in start-up funding. HP retained a controlling interest until mid-2000, when it spun-off the rest of its shares in Agilent to HP shareholders as a tax-free transaction.

Case Study

-Discuss the conditions under which this spin-off would constitute a tax-free transaction.

(Essay)

4.9/5 (33)

Sara Lee Attempts to Create Value through Restructuring

After spurning a series of takeover offers, Sara Lee, a global consumer goods company, announced in early 2011 its intention to split the firm into two separate publicly traded companies. The two companies would consist of the firm's North American retail and food service division and its international beverage business. The announcement comes after a long string of restructuring efforts designed to increase shareholder value. It remains to be seen if the latest effort will be any more successful than earlier efforts.

Reflecting a flawed business strategy, Sara Lee had struggled for more than a decade to create value for its shareholders by radically restructuring its portfolio of businesses. The firm's business strategy had evolved from one designed in the mid-1980s to market a broad array of consumer products from baked goods to coffee to underwear under the highly recognizable brand name of Sara Lee into one that was designed to refocus the firm on the faster-growing food and beverage and apparel businesses. Despite acquiring several European manufacturers of processed meats in the early 1990s, the company's profits and share price continued to flounder.

In September 1997, Sara Lee embarked on a major restructuring effort designed to boost both profits, which had been growing by about 6% during the previous five years, and the company's lagging share price. The restructuring program was intended to reduce the firm's degree of vertical integration, shifting from a manufacturing and sales orientation to one focused on marketing the firm's top brands. The firm increasingly viewed itself as more of a marketing than a manufacturing enterprise.

Sara Lee outsourced or sold 110 manufacturing and distribution facilities over the next two years. Nearly 10,000 employees, representing 7% of the workforce, were laid off. The proceeds from the sale of facilities and the cost savings from outsourcing were either reinvested in the firm's core food businesses or used to repurchase $3 billion in company stock. 1n 1999 and 2000, the firm acquired several brands in an effort to bolster its core coffee operations, including such names as Chock Full o'Nuts, Hills Bros, and Chase & Sanborn.

Despite these restructuring efforts, the firm's stock price continued to drift lower. In an attempt to reverse the firm's misfortunes, the firm announced an even more ambitious restructuring plan in 2000. Sara Lee would focus on three main areas: food and beverages, underwear, and household products. The restructuring efforts resulted in the shutdown of a number of meat packing plants and a number of small divestitures, resulting in a 10% reduction (about 13,000 people) in the firm's workforce. Sara Lee also completed the largest acquisition in its history, purchasing The Earthgrains Company for $1.9 billion plus the assumption of $0.9 billion in debt. With annual revenue of $2.6 billion, Earthgrains specialized in fresh packaged bread and refrigerated dough. However, despite ongoing restructuring activities, Sara Lee continued to underperform the broader stock market indices.

In February 2005, Sara Lee executed its most ambitious plan to transform the firm into a company focused on the global food, beverage, and household and body care businesses. To this end, the firm announced plans to dispose of 40% of its revenues, totaling more than $8 billion, including its apparel, European packaged meats, U.S. retail coffee, and direct sales businesses.

In 2006, the firm announced that it had completed the sale of its branded apparel business in Europe, Global Body Care and European Detergents units, and its European meat processing operations. Furthermore, the firm spun off its U.S. Branded Apparel unit into a separate publicly traded firm called HanesBrands Inc. The firm raised more than $3.7 billion in cash from the divestitures. The firm was now focused on its core businesses: food, beverages, and household and body care.

In late 2008, Sara Lee announced that it would close its kosher meat processing business and sold its retail coffee business. In 2009, the firm sold its Household and Body Care business to Unilever for $1.6 billion and its hair care business to Procter & Gamble for $0.4 billion.

In 2010, the proceeds of the divestitures made the prior year were used to repurchase $1.3 billion of Sara Lee's outstanding shares. The firm also announced its intention to repurchase another $3 billion of its shares during the next three years. If completed, this would amount to about one-third of its approximate $10 billion market capitalization at the end of 2010.

What remains of the firm are food brands in North America, including Hillshire Farm, Ball Park, and Jimmy Dean processed meats and Sara Lee baked goods and Earthgrains. A food distribution unit will also remain in North America, as will its beverage and bakery operations. Sara Lee is rapidly moving to become a food, beverage, and bakery firm. As it becomes more focused, it could become a takeover target.

Has the 2005 restructuring program worked? To answer this question, it is necessary to determine the percentage change in Sara Lee's share price from the announcement date of the restructuring program to the end of 2010, as well as the percentage change in the share price of HanesBrands Inc., which was spun off on August 18, 2006. Sara Lee shareholders of record received one share of HanesBrands Inc. for every eight Sara Lee shares they held.

Sara Lee's share price jumped by 6% on the February 21, 2004 announcement date, closing at $19.56. Six years later, the stock price ended 2010 at $14.90, an approximate 24% decline since the announcement of the restructuring program in early 2005. Immediately following the spinoff, HanesBrands' stock traded at $22.06 per share; at the end of 2010, the stock traded at $25.99, a 17.8% increase.

A shareholder owning 100 Sara Lee shares when the spin-off was announced would have been entitled to 12.5 HanesBrands shares. However, they would have actually received 12 shares plus $11.03 for fractional shares .

A shareholder of record who had 100 Sara Lee shares on the announcement date of the restructuring program and held their shares until the end of 2010 would have seen their investment decline 24% from $1,956 (100 shares × $19.56 per share) to $1,486.56 by the end of 2010. However, this would have been partially offset by the appreciation of the HanesBrands shares between 2006 and 2010. Therefore, the total value of the hypothetical shareholder's investment would have decreased by 7.5% from $1,956 to $1,809.47 . This compares to a more modest 5% loss for investors who put the same $1,956 into a Standard & Poor's 500 stock index fund during the same period.

Why did Sara Lee underperform the broader stock market indices during this period? Despite the cumulative buyback of more than $4 billion of its outstanding stock, Sara Lee's fully diluted earnings per share dropped from $0.90 per share in 2005 to $0.52 per share in 2009. Furthermore, the book value per share, a proxy for the breakup or liquidation value of the firm, dropped from $3.28 in 2005 to $2.93 in 2009, reflecting the ongoing divestiture program. While the HanesBrands spin-off did create value for the shareholder, the amount was far too modest to offset the decline in Sara Lee's market value. During the same period, total revenue grew at a tepid average annual rate of about 3% to about $13 billion in 2009.

Case Study :

-In what sense is the Sara Lee business strategy in effect a breakup strategy? Be specific.

(Essay)

5.0/5 (34)

In deciding to sell a business,a parent firm should compare the business' after-tax value in sale with its pre-tax value to the parent as part of the parent.

(True/False)

4.7/5 (25)

In addition,stock-based incentive programs to attract and retain key managers can be implemented for each operation with its own tracking stock.

(True/False)

4.8/5 (33)

Bristol-Myers Squibb Splits Off Rest of Mead Johnson

Facing the loss of patent protection for its blockbuster drug Plavix, a blood thinner, in 2012, Bristol-Myers Squibb Company decided to split off its 83% ownership stake in Mead Johnson Nutrition Company in late 2009 through an offer to its shareholders to exchange their Bristol-Myers shares for Mead Johnson shares. The decision was part of a longer-term restructuring strategy that included the sale of assets to raise money for acquisitions of biotechnology drug companies and the elimination of jobs to reduce annual operating expenses by $2.5 billion by the end of 2012.

Bristol-Myers anticipated a significant decline in operating profit following the loss of patent protection as increased competition from lower-priced generics would force sizeable reductions in the price of Plavix. Furthermore, Bristol-Myers considered Mead Johnson, a baby formula manufacturer, as a noncore business that was pursuing a focus on biotechnology drugs. Bristol-Myers shareholders greeted the announcement positively, with the firm's shares showing the largest one-day increase in eight months.

In the exchange offer, Bristol-Myers shareholders were able to exchange some, none, or all of their shares of Bristol-Myers common stock for shares of Mead Johnson common stock at a discount. The discount was intended to provide an incentive for Bristol-Myers shareholders to tender their shares. Also, the rapid appreciation of the Mead Johnson shares in the months leading up to the announced split-off suggested that these shares could have attractive long-term appreciation potential.

While the transaction did not provide any cash directly to the firm, it did indirectly augment Bristol-Myer's operating cash flow by $214 million annually. This represented the difference between the $350 million that Bristol-Myers paid in dividends to Mead Johnson shareholders and the $136 million it received in dividends from Mead Johnson each year. By reducing the number of Bristol-Myers shares outstanding, the transaction also improved Bristol-Myers' earnings per share by 4% in 2011. Finally, by splitting-off a noncore business, Bristol-Myers was increasing its attractiveness to investors interested in a "pure play" in biotechnology pharmaceuticals.

The exchange was tax free to Bristol-Myers shareholders participating in the exchange offer, who also stood to gain if the now independent Mead Johnson Corporation were acquired at a later date. The newly independent Mead Johnson had a poison pill in place to discourage any takeover within six months to a year following the split-off. The tax-free status of the transaction could have been disallowed by the IRS if the transaction were viewed as a "disguised sale" intended to allow Bristol-Myers to avoid paying taxes on gains incurred if it had chosen to sell Mead Johnson.

Case Study Short Essay Examination Questions:

British Petroleum Sells Oil and Gas Assets to Apache Corporation

In the months that followed the oil spill in the Gulf of Mexico, British Petroleum agreed to create a $20 billion fund to help cover the damages and cleanup costs associated with the spill. The firm had agreed to contribute $5 billion to the fund before the end of 2010. To help meet this obligation and to help finance the more than $4 billion already spent on the spill, the firm announced on July 20, 2010, that it had reached an agreement to sell Apache Corporation its oil and gas fields in Texas and southeast New Mexico worth $3.1 billion; gas fields in Western Canada for $3.25 billion; and oil and gas properties in Egypt for $650 million. All of these properties had been in production for years, and their output rates were declining.

Apache is a Houston, Texas-based independent oil and gas exploration firm with a reputation for being able to extract additional oil and gas from older properties. Also, Apache had operations near each of the BP properties, enabling them to take control of the acquired assets with existing personnel.

In what appears to have been a premature move, Apache agreed to acquire Mariner Energy and Devon Energy's offshore assets in the Gulf of Mexico for a total of $3.75 billion just days before the BP oil rig explosion in the Gulf. The acquisitions made Apache a major player in the Gulf just weeks before the United States banned temporarily deep-water drilling exploration in federal waters.

The announcement of the sale of these properties came as a surprise because BP had been rumored to be attempting to sell its stake in the oil fields of Prudhoe Bay, Alaska. The sale had been expected to fetch as much as $10 billion. The sale failed to materialize because of lingering concerns that BP might at some point seek bankruptcy protection and because the firm's creditors could seek to reverse an out-of-court asset sale as a fraudulent conveyance of assets. Fraudulent conveyance refers to the illegal transfer of assets to another party in order to defer, hinder, or defraud creditors. Under U.S. bankruptcy laws, courts might order that any asset sold by a company in distress, such as BP, must be encumbered with some of the liabilities of the seller if it can be shown that the distressed firm undertook the sale with the full knowledge that it would be filing for bankruptcy protection at a later date.

Ideally, buyers would like to purchase assets "free and clear" of the environmental liabilities associated with the Gulf oil spill. Consequently, a buyer of BP assets would have to incorporate such risks in determining the purchase price for such assets. In some instances, buyers will buy assets only after the seller has gone through the bankruptcy process in order to limit fraudulent conveyance risks.

Discussion Questions

1. In what sense were the BP properties strategically more valuable to Apache than to British Petroleum?

2. How could Apache have protected itself from risks that they might be required at some point in the future to be liable

for some portion of the BP Gulf-related liabilities? What are some of the ways Apache could have estimated the potential costs of such liabilities? Be specific.

Case Study Short Essay Examination Questions:

Anatomy of a Spin-Off

On October 18, 2006, Verizon Communication's board of directors declared a dividend to the firm's shareholders consisting of shares in a company comprising the firm's domestic print and Internet yellow pages directories publishing operations (Idearc Inc.). The dividend consisted of 1 share of Idearc stock for every 20 shares of Verizon common stock. Idearc shares were valued at $34.47 per share. On the dividend payment date, Verizon shares were valued at $36.42 per share. The 1-to-20 ratio constituted a 4.73% yield-that is, $34.47/ ($36.42 × 20)-approximately equal to Verizon's then current cash dividend yield.

Because of the spin-off, Verizon would contribute to Idearc all its ownership interest in Idearc Information Services and other assets, liabilities, businesses, and employees currently employed in these operations. In exchange for the contribution, Idearc would issue to Verizon shares of Idearc common stock to be distributed to Verizon shareholders. In addition, Idearc would issue senior unsecured notes to Verizon in an amount approximately equal to the $9 billion in debt that Verizon incurred in financing Idearc's operations historically. Idearc would also transfer $2.5 billion in excess cash to Verizon. Verizon believed it owned such cash balances, since they were generated while Idearc was part of the parent.

Verizon announced that the spin-off would enable the parent and Idearc to focus on their core businesses, which may facilitate expansion and growth of each firm. The spin-off would also allow each company to determine its own capital structure, enable Idearc to pursue an acquisition strategy using its own stock, and permit Idearc to enhance its equity-based compensation programs offered to its employees. Because of the spin-off, Idearc would become an independent public company. Moreover, no vote of Verizon shareholders was required to approve the spin-off, since it constitutes the payment of a dividend permissible by the board of directors according to the bylaws of the firm. Finally, Verizon shareholders have no appraisal rights in connection with the spin-off.

In late 2009, Idearc entered Chapter 11 bankruptcy because it was unable to meet its outstanding debt obligations. In September 2010, a trustee for Idearc's creditors filed a lawsuit against Verizon, alleging that the firm breached its fiduciary responsibility by knowingly spinning off a business that was not financially viable. The lawsuit further contends that Verizon benefitted from the spin-off at the expense of the creditors by transferring $9 billion in debt from its books to Idearc and receiving $2.5 billion in cash from Idearc.

Discussion Questions

1. How do you believe the Idearc shares were valued for purposes of the spin-off? Be specific.

2. Do you believe that it is fair for Idearc to repay a portion of the debt incurred by Verizon relating to Idearc's operations even though Verizon included Idearc's earnings in its consolidated income statement? Is the transfer of excess cash to the parent fair? Explain your answer.

3. Do you believe shareholders should have the right to approve a spin-off? Explain your answer?

4. To what extent do you believe that Verizon's activities could be viewed as fraudulent? Explain your answer.

Case Study Short Essay Examination Questions:

Anatomy of a Split-Off: Bristol-Myers Squibb

Under the Bristol-Myers Squibb exchange offer of Mead Johnson shares for shares of its common stock, announced on November 16, 2009, each BMS shareholder would receive $1.11 for each $1 of BMS stock tendered and accepted in the exchange offer. The exchange was subject to an upper limit of 0.6027 shares of MJ common stock per share of BMS common.

On December 4, 2009, BMS amended the offer by increasing the maximum share exchange ratio to 0.6313, indicating it would accept for exchange a maximum of 269,281,601 shares of its stock and that if the exchange offer were oversubscribed, all shares tendered would be subject to proration. The proration formula was be determined by dividing the maximum number of MJ shares BMS was willing to exchange by the number of BMS shares actually tendered.

The actual ratio at which shares of Bristol-Myers common stock and shares of Mead Johnson common stock were exchanged was determined by computing a simple three-day average of the shares of the two firms during December 8-10, 2009, subject to the 0.6313 upper limit. On December 16, 2009, Bristol-Myers announced it would exchange up to 170 million share of Mead Johnson common stock (i.e., all that it owned) for outstanding shares of its stock at an exchange ratio of 0.6313 shares of Mead Johnson common stock for each share of Bristol-Myers common stock tendered and accepted in the exchange offer.

Assuming that the three-day average of BMS and MJ share prices was $24.30 and $43.75, respectively, BMS shareholders whose tendered shares were accepted in the exchange offer received the higher of $26.97 (i.e., $24.30 × 1.11) or $27.62 (i.e., 0.6313 × $43.75). Therefore, a BMS shareholder tendering 100 shares of BMS stock would have received the share equivalent of $2,762 ($27.62 × 100) or 63.13 MJ shares at $43.75 per shares (i.e., $2,762 ÷ $43.75). Fractional shares were paid in cash.

The actual number of BMS shares tendered totaled 500,547,697, resulting in a proration ratio of 53.80% (i.e., 269,281,601 ÷ 500,547,697). Each shareholder tendering BMS shares would only have 53.80% of their tendered shares accepted for the exchange.

Discussion Questions:

1. Why did Bristol-Myers Squibb offer its shareholders $1.11 worth of Mead Johnson stock for each $1 of Bristol-Myers Squibb stock tendered and accepted in the exchange offer?

2. Why did Bristol-Myers Squibb prorate the number of shares tendered in the exchange offer?

Case Study Short Essay Examination Questions:

Inside M&A. Financial Services Firms Streamline their Operations

During 2005 and 2006, a wave of big financial services firms announced their intentions to spin-off operations that did not seem to fit strategically with their core business. In addition to realigning their strategies, the parent firms noted the favorable tax consequences of a spin-off, the potential improvement in the parent's financial returns, the elimination of conflicts with customers, and the removal of what, for some, had become a management distraction.

American Express announced plans in early 2005 to jettison its financial advisory business through a tax-free spin-off to its shareholders. The firm also noted that it would incur significant restructuring-related expenses just before the spin-off. Such one-time write-offs by the parent are sometimes necessary to "clean up" the balance sheet of the unit to be spun off and unburden the newly formed company's earnings performance. American Express anticipated substantial improvement in future financial returns on assets as it will be eliminating more than $410 billion in assets from its balance sheet that had been generating relatively meager earnings.

Investment bank Morgan Stanley announced in mid-2005 its intent to spin-off its Discover Credit Card operation. While Discover Card generated about one fifth of the firm's pretax profits, Morgan Stanley had been unable to realize significant synergies with its other operations. The move represented an attempt by senior Morgan Stanley management to mute shareholder criticism of the company's lackluster stock performance due to what many viewed had been the firm's excessive diversification.

Similarly, J.P. Morgan Chase announced plans in 2006 to spin off its $13 billion private equity fund, J.P. Morgan Partners. The bank would invest up to $1 billion in a new fund J.P. Morgan Partners plans to open as a successor to the current Global Fund. Because the bank's ownership position would be less than 25 percent, it would be classified as a passive partner. The expectation is that, by jettisoning this operation, the bank would be able to reduce earnings volatility and decrease competition between the bank and large customers when making investments.

-Speculate as to why a firm may choose to spin-off rather than divest a business?

(Essay)

4.8/5 (37)

Tracking stocks are often created to give investors a pure play investment opportunity in one of the parent's subsidiaries.

(True/False)

4.9/5 (38)

A diversified automotive parts supplier has decided to sell its valve manufacturing business.This sale is referred to as a

(Multiple Choice)

4.8/5 (41)

Divestitures,spin-offs,equity carve-outs,split-ups,and bust-ups are commonly used strategies to exit businesses.

(True/False)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)