Exam 7: Consolidated Financial Statements - Ownership Patterns and Income Taxes

Exam 1: The Equity Method of Accounting for Investments121 Questions

Exam 1: A: the Equity Method of Accounting for Investments121 Questions

Exam 2: Consolidation of Financial Information116 Questions

Exam 2: A: Consolidation of Financial Information116 Questions

Exam 3: Consolidations - Subsequent to the Date of Acquisition120 Questions

Exam 3: A: Consolidations - Subsequent to the Date of Acquisition120 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership117 Questions

Exam 4: A: Consolidated Financial Statements and Outside Ownership117 Questions

Exam 5: Consolidated Financial Statements Intra-Entity Asset Transactions123 Questions

Exam 5: A: Consolidated Financial Statements Intra-Entity Asset Transactions123 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues117 Questions

Exam 6: A: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues117 Questions

Exam 7: Consolidated Financial Statements - Ownership Patterns and Income Taxes112 Questions

Exam 7: A: Consolidated Financial Statements - Ownership Patterns and Income Taxes112 Questions

Exam 8: Segment and Interim Reporting105 Questions

Exam 8: A: Segment and Interim Reporting115 Questions

Exam 9: Foreign Currency Transactions and Hedging Foreign Exchange Risk99 Questions

Exam 9: A: Foreign Currency Transactions and Hedging Foreign Exchange Risk99 Questions

Exam 10: Translation of Foreign Currency Financial Statements96 Questions

Exam 10: A: Translation of Foreign Currency Financial Statements96 Questions

Exam 11: Worldwide Accounting Diversity and International Accounting Standards63 Questions

Exam 11: A: Worldwide Accounting Diversity and International Accounting Standards63 Questions

Exam 12: Financial Reporting and the Securities and Exchange Commission76 Questions

Exam 12: A: Financial Reporting and the Securities and Exchange Commission76 Questions

Exam 13: Accounting for Legal Reorganizations and Liquidations75 Questions

Exam 13: A: Accounting for Legal Reorganizations and Liquidations78 Questions

Exam 14: Partnerships: Formation and Operation89 Questions

Exam 14: A: Partnerships: Formation and Operation89 Questions

Exam 15: Partnerships: Termination and Liquidation69 Questions

Exam 15: A: Partnerships: Termination and Liquidation69 Questions

Exam 16: Accounting for State and Local Governments, Part I83 Questions

Exam 16: A: Accounting for State and Local Governments, Part I83 Questions

Exam 17: Accounting for State and Local Governments, Part II42 Questions

Exam 17: A: Accounting for State and Local Governments, Part II47 Questions

Exam 18: Accounting for Not-For-Profit Entities72 Questions

Exam 18: A: Accounting for Not-For-Profit Entities72 Questions

Exam 19: Accounting for Estates and Trusts81 Questions

Exam 19: A: Accounting for Estates and Trusts81 Questions

Select questions type

-What was the net income attributable to the noncontrolling interest, assuming that the separate return method was used to assign the income tax expense?

-What was the net income attributable to the noncontrolling interest, assuming that the separate return method was used to assign the income tax expense?

(Multiple Choice)

4.9/5  (37)

(37)

-Compute Whitton's accrual-based consolidated net income for 2018.

-Compute Whitton's accrual-based consolidated net income for 2018.

(Multiple Choice)

4.7/5 (35)

Assuming that separate income tax returns are being filed, what deferred income tax asset is created?

(Multiple Choice)

4.8/5 (38)

Which of the following is true concerning the treasury stock approach in accounting for a subsidiary's investment in parent company stock?

(Multiple Choice)

5.0/5 (39)

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

-Which of the following statements is false concerning a father-son-grandson configuration?

-Which of the following statements is false concerning a father-son-grandson configuration?

(Multiple Choice)

4.9/5 (38)

What configuration of corporate ownership is described as a father-son-grandson relationship?

(Essay)

4.8/5 (37)

Jastoon Co.acquired all of Wedner Co.for $588,000 cash in a tax-free transaction.On that date, the subsidiary had net assets with a $560,000 fair value but a $420,000 book value and income tax basis.The income tax rate was 30%.What amount of goodwill should have been recognized on the date of the acquisition?

(Multiple Choice)

4.9/5 (32)

-Compute accrual-based consolidated income before income tax.

-Compute accrual-based consolidated income before income tax.

(Multiple Choice)

4.9/5 (43)

Wilkins Inc.owned 60% of Motumbo Co.During the current year, Motumbo reported net income of $280,000 but paid a total cash dividend of only $56,000.

Required:

Assuming an income tax rate of 30%, what amount of Deferred Income Tax Liability arising this year must be recognized in the consolidated balance sheet?

(Essay)

4.9/5 (44)

-Under the separate return method, income tax expense that will be assigned to Hill is closest to:

(Multiple Choice)

4.9/5 (35)

-What amount should be reported for consolidated net income?

-What amount should be reported for consolidated net income?

(Multiple Choice)

4.9/5 (32)

Assuming that a consolidated income tax return is being filed, what deferred income tax asset is created?

(Multiple Choice)

4.8/5 (41)

White Company owns 60% of Cody Company. Separate tax returns are required. For 2017, White's operating income (excluding taxes and any income from Cody) was $300,000 while Cody reported a pretax income of $125,000. During the period, Cody declared total dividends of $25,000; $15,000 (60%) to White and $10,000 to the noncontrolling interest. White declared dividends of $180,000. The income tax rate for both companies is 30%.

-Compute Cody's undistributed earnings for 2018.

(Multiple Choice)

4.9/5 (35)

On January 1, 2018, a subsidiary buys 8 percent of the outstanding voting stock of its parent corporation.The payment of $350,000 exceeded book value of the acquired shares by $50,000, attributable to a copyright with a 10-year useful life.During the year, the parent reported operating income of $675,000 (excluding investment income from the subsidiary), and paid $100,000 in dividends.If the treasury stock approach is used, how is the Investment in Parent Stock reported in the consolidated balance sheet at December 31, 2018?

(Multiple Choice)

4.8/5 (38)

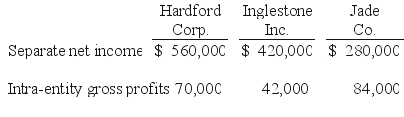

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

-Compute Chase's attributed ownership in Ross.

(Multiple Choice)

4.7/5 (30)

What is net income attributable to the controlling interest of Paris?

(Multiple Choice)

4.7/5 (41)

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

-The benefits of filing a consolidated tax return include all of the following except

(Multiple Choice)

4.9/5 (35)

Hardford Corp. held 80% of Inglestone Inc., which, in turn, owned 80% of Jade Co. Excess amortization expense was not required by any of these acquisitions. Separate net income figures (without investment income) as well as upstream intra-entity gross profits (before deferral) included in the income for the current year follow:

-Compute the net income attributable to the noncontrolling interest in Ross for 2018.

(Multiple Choice)

4.9/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)