Exam 8: Foreign Currency Transactions and Hedges

Compare and contrast accounting for foreign currency transactions and hedges under IFRS and ASPE.

ASPE and IFRS are similar in their methods of accounting for foreign exchange transactions and balances.Monetary items are translated using the spot rate at the date of the SFP,and gains and losses are reported in net earnings.For non-monetary items carried at historical cost,these are translated at the historical exchange rate.

For non-monetary assets carried at fair value,IFRS uses the exchange rate on the date the fair value was determined.Under ASPE,the exchange rate used is the spot rate on the balance sheet date.In both cases,any exchange gains and losses are reported in net earnings.

Hedging under ASPE is more simplified than under IFRS.In both cases,hedging is optional and requires documentation.(Documentation under ASPE is less onerous that under IFRS. )IFRS requires that hedges be classified as fair value hedges or cash flow hedges.The gains and losses on fair value hedges are reported in earnings.Gains and losses on cash flows hedges are reported in OCI until the related anticipated transaction takes place,at which time the gains and losses are either transferred to earnings or included in the carrying cost of the asset.For both fair value hedges and cash flow hedges,the derivatives are fair valued at each reporting period.Forward contracts,futures contracts,options and swaps can all qualify as hedging instruments under IFRS.

Under ASPE,hedge accounting can only be used for anticipated transactions.Derivatives that are not designated as hedges must be fair valued at each reporting period and any gains and losses are reported in net earnings.Only forward contracts can be used to hedge foreign currency transactions.If the forward contract is designated as a hedge,it is not recognized until maturity.At maturity,the gain or loss is adjusted to the carrying value of the hedged item.

Disclosure is required under both ASPE and IFRS,although ASPE disclosure is less extensive.

On December 1,20X5,Gillard Ltd.sold goods to International Traders Ltd. ,a company located in Switzerland for 500,000 Swiss francs (CHF).At the date of sale,the spot rate was CHF1 = $1.0329.On the same date,Gillard acquired a 90-day forward contract at a rate of CHF1 = $1.0315.On March 1,20X6,Gillard receives full payment from International Traders and delivered the Swiss francs in execution of the forward contract.The spot rate at March 1,20X6 was CHF1 = $1.0287.Assume that Gillard has a December 31 year-end and that the spot rate on that date was CHF1 = $1.0302.At December 31,the forward rate for a 60 day contract was CHF1 = 1.0394.At December 31,what is the balance of Gillard's forward contract payable?

B

Under IFRS,a hedging relationship qualifies for special hedge accounting rules,only if it meets five conditions.

Required:

Explain the five conditions that must be met for a derivative to qualify for special hedge accounting.Identify what qualifies as a "hedged item".Identify what qualifies as a "hedging instrument".Outline the conditions required for a hedge to be "highly effective with respect to foreign exchange risk".

All five of the following conditions must be met for a hedging relationship to qualify for special hedge accounting:

1.the hedging relationship is formally designated and documented at the inception and is within the company's overall risk management strategy;

2.the hedge is anticipated to be highly effective;

3.for cash flow hedges,the forecast transaction is highly probable;

4.the effectiveness of the hedge can be determined reliably;and

5.the hedge is assessed regularly on an ongoing basis and has been highly effective in the past.

The hedging item can be an asset,liability,unrecognized future commitment,a highly probable forecast transaction or a net investment in a foreign subsidiary.

The hedging instrument offsets the risk and is normally a derivative,which could include a forward contract,futures contract,option or a swap.For currency hedges,a non-derivative financial asset or liability can also qualify as a hedging instrument.

For a hedge to be highly effective with respect to foreign exchange risk,it must meet the following two conditions:

1.At inception,the hedge must be expected to be highly effective in offsetting changes in fair value or cash flows due to foreign currency risk.The effectiveness is tested at each subsequent reporting date.

2.The actual results of the gain or loss on the hedging instrument must be between 80% and 125% of the loss or gain of the hedged item.

On November 2,20X9,Henry Company purchased a machine for 100,000 Swiss francs (CHF)with payment requirement on March 30,20X10.To eliminate the risk of foreign exchange losses on this payable,Henry entered into a forward exchange contract on November 3,20X9 to receive CHF 100,000 at a forward rate of CHF1 = $2 on March 30,20X10.The spot rate was CHF1 = $1.95 on November 2,20X9 and CHF1 = $1.97 on December 1,20X9.What is the amount of the premium or discount on the forward exchange contract on December 1,20X9?

On December 1,20X5,Gillard Ltd.sold goods to International Traders Ltd. ,a company located in Switzerland for 500,000 Swiss francs (CHF).At the date of sale,the spot rate was CHF1 = $1.0329.On the same date,Gillard acquired a 90-day forward contract at a rate of CHF1 = $1.0315.On March 1,20X6,Gillard receives full payment from International Traders and delivered the Swiss francs in execution of the forward contract.The spot rate at March 1,20X6 was CHF1 = $1.0287.What is the net exchange gain (loss)on the forward contract?

Under accounting standards for private enterprises,what exchange rate is used for non-monetary items carried at fair value?

Under accounting standards for private enterprises,which of the following can be used as hedging instruments?

What is the exchange rate in effect at the date of the transaction called?

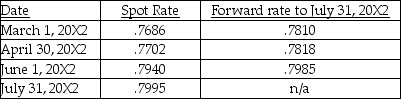

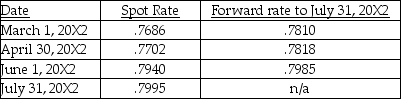

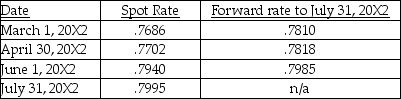

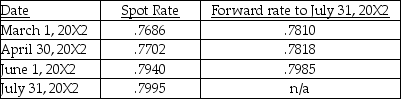

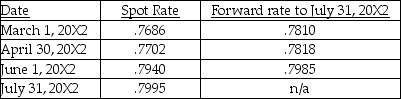

On March 1,20X2,McBride Ltd.issued a purchase order to Tao Heavy Machines (Singapore)Inc.to acquire a drilling machine for $400,000 SGD.On the same day,McBride entered into a forward contract to receive $400,000 SGD on July 31,20X2.The machine was delivered on June 1,20X2 and payment was made July 31,20X2.McBride has an April 30 year-end.The following information has been provided:

Assume that the transaction qualifies as a fair-value hedge.What is the cost of the hedge?

Assume that the transaction qualifies as a fair-value hedge.What is the cost of the hedge?

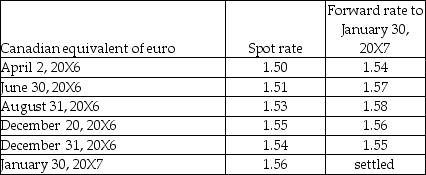

Beauty Care Limited (BCL)manufactures and distributes leather furniture to various companies in Europe.On April 2,20X6,BCL entered into a sales contract with a company in Germany to sell 1,000 sofas.The contract price is €2,000 per sofa.Five hundred sofas are to be delivered in May 15,20X6 and the remaining half is to be delivered on December 20,20X6.Payment is due in two instalments with half due on August 31,20X6 and the remaining half due January 30,20X7.However,the customer has the right to cancel the contract with 30 days' notice.

BCL entered into a forward contract to hedge against the Euro exchange rate for €1 million each coming due on January 31,20X7.BCL has a December 31 year end.

Delivery of the furniture occurred on the dates specified and the company collected the receivables due and settled the forward contract January 30,20X7.

The exchange rates were as followed:

Required:

Assume that the forward contract is designated as a cash flow hedge since the sale is highly probable.Prepare the journal entries to record the sales and the hedge.Use the gross method to record the journal entries.BCL reports under IFRS.

Required:

Assume that the forward contract is designated as a cash flow hedge since the sale is highly probable.Prepare the journal entries to record the sales and the hedge.Use the gross method to record the journal entries.BCL reports under IFRS.

On March 1,20X2,McBride Ltd.issued a purchase order to Tao Heavy Machines (Singapore)Inc.to acquire a drilling machine for $400,000 SGD.On the same day,McBride entered into a forward contract to receive $400,000 SGD on July 31,20X2.The machine was delivered on June 1,20X2 and payment was made July 31,20X2.McBride has an April 30 year-end.The following information has been provided:

Assume that the transaction qualifies as a cash-flow hedge.What is the cost of the hedge?

Assume that the transaction qualifies as a cash-flow hedge.What is the cost of the hedge?

On March 1,20X2,McBride Ltd.issued a purchase order to Tao Heavy Machines (Singapore)Inc.to acquire a drilling machine for $400,000 SGD.On the same day,McBride entered into a forward contract to receive $400,000 SGD on July 31,20X2.The machine was delivered on June 1,20X2 and payment was made July 31,20X2.McBride has an April 30 year-end.The following information has been provided:

Assume that the transaction qualifies as a fair-value hedge.What amount of exchange gain (loss)should be recognized at April 30,20X2?

Assume that the transaction qualifies as a fair-value hedge.What amount of exchange gain (loss)should be recognized at April 30,20X2?

On March 1,20X2,McBride Ltd.issued a purchase order to Tao Heavy Machines (Singapore)Inc.to acquire a drilling machine for $400,000 SGD.On the same day,McBride entered into a forward contract to receive $400,000 SGD on July 31,20X2.The machine was delivered on June 1,20X2 and payment was made July 31,20X2.McBride has an April 30 year-end.The following information has been provided:

Assume that the transaction qualifies as a fair-value hedge.On March 1,at what amount should the forward contract be recorded?

Assume that the transaction qualifies as a fair-value hedge.On March 1,at what amount should the forward contract be recorded?

On November 2,20X9,Henry Company purchased a machine for 100,000 Swiss francs (CHF)with payment requirement on March 30,20X10.To eliminate the risk of foreign exchange losses on this payable,Henry entered into a forward exchange contract on November 3,20X9 to receive CHF 100,000 at a forward rate of CHF1 = $2 on March 30,20X10.The spot rate was CHF1 = $1.95 on November 2,20X9 and CHF1 = $1.97 on December 1,20X9.How should the premium or discount on the forward exchange contract be accounted for?

Helvetia Corp. ,a Swiss firm,bought merchandise from Bouchard Company of Quebec on December 15,20X7 for 20,000 CHF,payable on January 14,20X8.Bouchard and Helvetia both close their books on December 31.The 20,000 CHF was paid on January 14,20X8.The exchange rates for CHF1 were:  Required:

Provide the journal entries for Helvetia (the buyer)at each of the above dates,as required.

Required:

Provide the journal entries for Helvetia (the buyer)at each of the above dates,as required.

Under IFRS,which of the following statements about hedging a foreign currency risk of an accepted purchase order is true?

On December 1,20X5,Gillard Ltd.sold goods to International Traders Ltd. ,a company located in Switzerland for 500,000 Swiss francs (CHF).At the date of sale,the spot rate was CHF1 = $1.0329.On the same date,Gillard acquired a 90-day forward contract at a rate of CHF1 = $1.0315.On March 1,20X6,Gillard receives full payment from International Traders and delivered the Swiss francs in execution of the forward contract.The spot rate at March 1,20X6 was CHF1 = $1.0287.What amount should Gillard record for the sale?

On March 1,20X2,McBride Ltd.issued a purchase order to Tao Heavy Machines (Singapore)Inc.to acquire a drilling machine for $400,000 SGD.On the same day,McBride entered into a forward contract to receive $400,000 SGD on July 31,20X2.The machine was delivered on June 1,20X2 and payment was made July 31,20X2.McBride has an April 30 year-end.The following information has been provided:

Assume that the transaction qualifies as a cash-flow hedge.What amount should be recognized as other comprehensive income at April 30,20X2?

Assume that the transaction qualifies as a cash-flow hedge.What amount should be recognized as other comprehensive income at April 30,20X2?

Which of the following is not one of the conditions that must be met to qualify for hedge accounting?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)