Exam 26: Property Transactions: Section 1231 and Recapture

Exam 1: Tax Research115 Questions

Exam 2 an Introduction to Taxation104 Questions

Exam 3: Corporate Formations and Capital Structure123 Questions

Exam 4: I: Determination of Tax138 Questions

Exam 5: The Corporate Income Tax126 Questions

Exam 6: Gross Income: Inclusions132 Questions

Exam 7: Corporate Nonliquidating Distributions113 Questions

Exam 8: Gross Income: Exclusions107 Questions

Exam 9: Other Corporate Tax Levies104 Questions

Exam 10: Property Transactions: Capital Gains and Losses133 Questions

Exam 1: Corporate Liquidating Distributions102 Questions

Exam 12: Deductions and Losses130 Questions

Exam 13: Corporate Acquisitions and Reorganizations104 Questions

Exam 14: Itemized Deductions114 Questions

Exam 15: Consolidated Tax Returns99 Questions

Exam 16: Losses and Bad Debts114 Questions

Exam 17: Partnership Formation and Operation115 Questions

Exam 18: Employee Expenses and Deferred Compensation135 Questions

Exam 19: Special Partnership Issues107 Questions

Exam 20: Depreciation cost Recovery amortization and Depletion93 Questions

Exam 21: S Corporations103 Questions

Exam 22: Accounting Periods and Methods107 Questions

Exam 23: The Gift Tax105 Questions

Exam 24: Property Transactions: Nontaxable Exchanges115 Questions

Exam 25: The Estate Tax107 Questions

Exam 26: Property Transactions: Section 1231 and Recapture100 Questions

Exam 27: Income Taxation of Trusts and Estates105 Questions

Exam 28: Special Tax Computation Methods, tax Credits, and Payment of Tax117 Questions

Exam 29: Administrative Procedures104 Questions

Select questions type

When gain is recognized on an involuntary conversion,gain is subject to recapture under Sec.1245 or Sec.1250.

(True/False)

4.8/5  (47)

(47)

Sec.1245 can increase the amount of gain recognized on an asset.

(True/False)

4.8/5 (39)

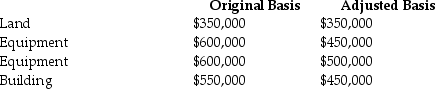

Describe the tax treatment for a noncorporate taxpayer in the 39.6% marginal tax bracket who sells each of the first two assets for $500,000 and each of the second two assets for $750,000.Each asset was purchased in 2010 and is used in a trade or business.There are no other gains and losses and no nonrecaptured Section 1231 losses.

(Essay)

4.8/5 (33)

Section 1250 could convert a portion of Sec.1231 gain into ordinary income if the real property was placed in service prior to 1987 and accelerated depreciation was used.

(True/False)

4.7/5 (37)

When a donee disposes of appreciated gift property,the recapture amount for the donee is computed by including the recapture amount attributable to the donor.

(True/False)

4.9/5 (32)

Pete sells equipment for $15,000 to Marcel,his son.The equipment cost $20,000 and has accumulated depreciation of $12,000. Marcel will use the equipment in his business.

a.What is the amount and character of Pete's gain on the sale?

b.How does your answer change if the sales price is $22,000?

(Essay)

4.9/5 (33)

Indicate whether each of the following assets are capital assets,Sec.1231 assets,or ordinary income property (property which,if sold,results in ordinary income).Assume that all of the property is held for more than one year.

a.XYZ Corporation owns land used as an employee parking lot.How is the parking lot classified for tax purposes?

b.Montana Corporation owns land held as an investment.How is the land classified for tax purposes?

c.John,a self-employed electrician,owns an automobile he uses strictly for personal use.How is the automobile classified for tax purposes?

d.Jan,a self-employed contractor,owns a truck she uses exclusively in her trade or business.How is the truck classified for tax purposes?

e.Leslie owns an office building where her accounting practice is located.What is the classification of the building?

f.Yvonne owns a computer for use in her job as a sales representative.She does not use the computer for personal purposes.How is the computer classified for tax purposes?

(Essay)

4.9/5 (39)

Gifts of appreciated depreciable property may trigger recapture of depreciation or cost-recovery deductions to the donor.

(True/False)

5.0/5 (40)

Octet Corporation placed a small storage building in service in 1999.Octet's original cost for the building is $800,000 and the cost recovery deductions are $300,000.This year the building is sold for $1,100,000. The amount and character of the gain are

(Multiple Choice)

4.8/5 (32)

Connors Corporation sold a warehouse during the current year for $980,000.The building had been acquired in 1980 at a cost of $830,000.The building is fully depreciated.

What is the amount and nature of the gain or loss on the sale of the warehouse?

(Essay)

4.9/5 (38)

In 2014,Thomas,who has a marginal tax rate of 15%,sells land that is Sec.1231 property at a gain of $4,000.If he has no other 1231 transactions or capital asset transactions and has no nonrecaptured 1231 gain,Thomas will pay no tax on the $4,000 gain.

(True/False)

4.8/5 (39)

Jacqueline dies while owning a building with a $1,000,000 FMV.The building is classified as Sec.1245 property acquired in 1985 for $850,000.Cost-recovery deductions of $850,000 have been claimed.Pam inherits the property.

a.What is the amount of Pam's basis in the property?

b.What is the amount of cost-recovery deductions that Pam must recover if she immediately sells the building?

(Essay)

4.9/5 (37)

Gains and losses from involuntary conversions of property used in a trade or business generally are classified as capital gains and losses.

(True/False)

4.9/5 (35)

Jed sells an office building during the current year for $800,000.The building was purchased in 1980 for $350,000. Jed had depreciated the building under an accelerated method,but it is now fully depreciated.Jed has never had any other Sec.1231 transactions.

a.What is the recognized gain or loss on the sale of the building and the character of the gain?

b.How will the gain be taxed?

(Essay)

4.9/5 (42)

Harry owns equipment ($50,000 basis and $38,000 FMV)and a building ($140,000 basis and $156,000 FMV),which are used in his business.Harry uses straight-line depreciation for both assets,which were acquired several years ago.Both the equipment and the building are destroyed in a fire,and Harry collects insurance proceeds equal to the assets' FMV.The tax result to Harry for this transaction is

(Multiple Choice)

4.9/5 (33)

In order to be considered Sec.1231 property,all of the following livestock must be held for 12 months or more from date of acquisition except

(Multiple Choice)

4.9/5 (42)

For noncorporate taxpayers,depreciation recapture is not required on real property placed in service after 1986.

(True/False)

4.7/5 (37)

During the current year,Kayla recognizes a $40,000 Section 1231 gain on sale of land and a $22,000 Section 1231 loss on the sale of land.Prior to this,Kayla's only Section 1231 item was a $10,000 loss six years ago.Kayla is in the 28% marginal tax bracket.The amount of tax resulting from these transactions is

(Multiple Choice)

5.0/5 (41)

Blair,whose tax rate is 28%,sells one tract of land at a gain of $29,000 and another tract of land at a gain of $11,000.Both tracts of land are Sec.1231 property.She has never had any other Sec.1231 transactions.How are the gains taxed?

(Multiple Choice)

4.8/5 (35)

During the current year,a corporation sells equipment for $300,000.The equipment cost $270,000 when purchased and placed in service two years ago and $60,000 of depreciation deductions were allowed.The results of the sale are

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)