Exam 12: An Alternative View of Risk and Return: The Arbitrage Pricing Theory

Exam 1: Introduction to Corporate Finance30 Questions

Exam 2: Accounting Statements and Cash Flow55 Questions

Exam 3: Financial Planning and Growth33 Questions

Exam 4: Financial Markets and Net Present Value: First Principles of Finance35 Questions

Exam 5: The Time Value of Money62 Questions

Exam 6: How to Value Bonds and Stocks68 Questions

Exam 7: Net Present Value and Other Investment Rules42 Questions

Exam 8: Net Present Value and Capital Budgeting39 Questions

Exam 9: Risk Analysis, Real Options, and Capital Budgeting24 Questions

Exam 10: Risk and Return: Lessons From Market History58 Questions

Exam 11: Risk and Return: the Capital Asset Pricing Model Capm58 Questions

Exam 12: An Alternative View of Risk and Return: The Arbitrage Pricing Theory36 Questions

Exam 13: Risk, Return, and Capital Budgeting57 Questions

Exam 14: Corporate Financing Decisions and Efficient Capital Markets39 Questions

Exam 15: Long-Term Financing: an Introduction40 Questions

Exam 16: Capital Structure: Basic Concepts44 Questions

Exam 17: Capital Structure: Limits to the Use of Debt44 Questions

Exam 18: Valuation and Capital Budgeting for the Levered Firm46 Questions

Exam 19: Dividends and Other Payouts42 Questions

Exam 20: Issuing Equity Securities to the Public43 Questions

Exam 21: Long-Term Debt51 Questions

Exam 22: Leasing37 Questions

Exam 23: Options and Corporate Finance: Basic Concepts52 Questions

Exam 24: Options and Corporate Finance: Extensions and Applications21 Questions

Exam 25: Warrants and Convertibles43 Questions

Exam 26: Derivatives and Hedging Risk48 Questions

Exam 27: Short-Term Finance and Planning48 Questions

Exam 28: Cash Management41 Questions

Exam 29: Credit Management29 Questions

Exam 30: Mergers and Acquisitions53 Questions

Exam 31: Financial Distress17 Questions

Exam 32: International Corporate Finance50 Questions

Select questions type

Which of the following is true about the impact on market price of a security when a company makes an announcement and the market has discounted the news?

Free

(Multiple Choice)

4.9/5  (43)

(43)

Correct Answer: Verified

Verified

E

Shareholders discount many corporate announcements because of their prior expectations. If an announcement causes the price to change it will mostly be driven by:

Free

(Multiple Choice)

4.9/5 (35)

Correct Answer:Verified

C

The term Corr(å R, ε T) = 0 tells us that:

Free

(Multiple Choice)

4.8/5 (33)

Correct Answer:Verified

B

The systematic response coefficient for productivity, βP, would produce an unexpected change in any security return of ________ if the expected rate of productivity was 1.5% and the actual rate was 2.25%:

(Multiple Choice)

4.8/5 (34)

For a diversified portfolio including a large number of stocks,:

(Multiple Choice)

4.9/5 (46)

Assuming that the single factor APT model applies, the beta for the market portfolio is:

(Multiple Choice)

4.8/5 (39)

In the One Factor (APT) Model, the characteristic line to estimate βi passes through the origin, unlike the estimate used in the CAPM because:

(Multiple Choice)

4.7/5 (33)

A security that has a beta of zero will have an expected return of:

(Multiple Choice)

4.9/5 (28)

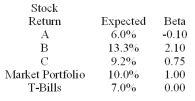

An investor is considering the three stocks given below:

Calculate the expected return and beta of a portfolio equally weighted between stocks B and C. Demonstrate that holding stock A actually reduces risk by comparing the risk of a portfolio equally weighted between stock B and T-Bills with a portfolio equally weighted between stock B and A.

Calculate the expected return and beta of a portfolio equally weighted between stocks B and C. Demonstrate that holding stock A actually reduces risk by comparing the risk of a portfolio equally weighted between stock B and T-Bills with a portfolio equally weighted between stock B and A.

(Essay)

4.8/5 (36)

If the expected rate of inflation was 3% and the actual rate was 6.2%; the systematic response coefficient from inflation, βI, would result in a change in any security return of:

(Multiple Choice)

5.0/5 (44)

Suppose the JumpStart Corporation's common stock has a beta of 0.8. If the risk-free rate is 4% and the expected market return is 9%, the expected return for JumpStart's common is:

(Multiple Choice)

4.7/5 (39)

In normal market conditions if a security has a negative beta:

(Multiple Choice)

4.8/5 (30)

Both the APT and the CAPM imply a positive relationship between expected return and risk. The APT views risk:

(Multiple Choice)

4.9/5 (35)

To estimate the cost of equity capital for a firm using APT or CAPM, it is necessary to have:

(Multiple Choice)

4.8/5 (32)

A growth stock portfolio and a value portfolio might be characterized

(Multiple Choice)

4.9/5 (42)

In a portfolio of risk y assets the response to a factor, Fi, can easily be determined by:

(Multiple Choice)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)