Exam 10: Risk and Return: Lessons From Market History

Exam 1: Introduction to Corporate Finance30 Questions

Exam 2: Accounting Statements and Cash Flow55 Questions

Exam 3: Financial Planning and Growth33 Questions

Exam 4: Financial Markets and Net Present Value: First Principles of Finance35 Questions

Exam 5: The Time Value of Money62 Questions

Exam 6: How to Value Bonds and Stocks68 Questions

Exam 7: Net Present Value and Other Investment Rules42 Questions

Exam 8: Net Present Value and Capital Budgeting39 Questions

Exam 9: Risk Analysis, Real Options, and Capital Budgeting24 Questions

Exam 10: Risk and Return: Lessons From Market History58 Questions

Exam 11: Risk and Return: the Capital Asset Pricing Model Capm58 Questions

Exam 12: An Alternative View of Risk and Return: The Arbitrage Pricing Theory36 Questions

Exam 13: Risk, Return, and Capital Budgeting57 Questions

Exam 14: Corporate Financing Decisions and Efficient Capital Markets39 Questions

Exam 15: Long-Term Financing: an Introduction40 Questions

Exam 16: Capital Structure: Basic Concepts44 Questions

Exam 17: Capital Structure: Limits to the Use of Debt44 Questions

Exam 18: Valuation and Capital Budgeting for the Levered Firm46 Questions

Exam 19: Dividends and Other Payouts42 Questions

Exam 20: Issuing Equity Securities to the Public43 Questions

Exam 21: Long-Term Debt51 Questions

Exam 22: Leasing37 Questions

Exam 23: Options and Corporate Finance: Basic Concepts52 Questions

Exam 24: Options and Corporate Finance: Extensions and Applications21 Questions

Exam 25: Warrants and Convertibles43 Questions

Exam 26: Derivatives and Hedging Risk48 Questions

Exam 27: Short-Term Finance and Planning48 Questions

Exam 28: Cash Management41 Questions

Exam 29: Credit Management29 Questions

Exam 30: Mergers and Acquisitions53 Questions

Exam 31: Financial Distress17 Questions

Exam 32: International Corporate Finance50 Questions

Select questions type

The dominant portfolio with the lowest possible risk measures is:

Free

(Multiple Choice)

4.9/5  (39)

(39)

Correct Answer: Verified

Verified

B

You have plotted the data for two securities over time on the same graph, ie., the month return of each security for the last 5 years. If the pattern of the movements of the two securities rose and fell as the other did, these two securities would have:

Free

(Multiple Choice)

4.8/5 (31)

Correct Answer:Verified

D

The CML is the pricing relationship between:

Free

(Multiple Choice)

4.8/5 (38)

Correct Answer:Verified

C

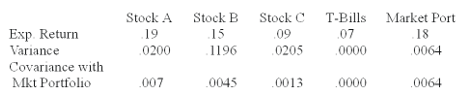

Given the following information on 3 stocks:

Using the CAPM, calculate the expected return for Stock's A, B, and C. Which stocks would you recommend purchasing?

Using the CAPM, calculate the expected return for Stock's A, B, and C. Which stocks would you recommend purchasing?

(Essay)

4.8/5 (41)

For a highly diversified equally weighted portfolio, the portfolio variance is:

(Multiple Choice)

4.7/5 (37)

Given the range of betas on actual companies reported in Table 11.7, a very low beta would be ___, and a very high beta would be _____ in comparison.

(Multiple Choice)

4.9/5 (34)

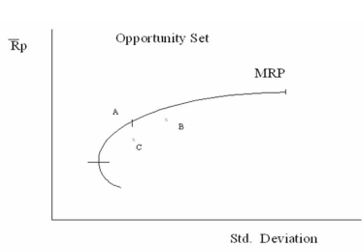

The diagram below represents an opportunity set for a two asset combination. Indicate the correct efficient set with labels; explain why it is so.

(Essay)

5.0/5 (42)

When a security is added to a portfolio the appropriate return and risk contributions are:

(Multiple Choice)

4.7/5 (34)

The elements along the diagonal of the Variance Covariance matrix are:

(Multiple Choice)

4.8/5 (30)

You want your portfolio beta to be 1.20. Currently, your portfolio consists of $100 invested in stock A with a beta of 1.4 and $300 in stock B with a beta of .6. You have another $400 to invest and want to divide it between an asset with a beta of 1.6 and a risk-free asset. How much should you invest in the risk-free asset?

(Multiple Choice)

4.9/5 (38)

The combination of the efficient set of portfolios with a riskless lending and borrowing rate results in:

(Multiple Choice)

4.7/5 (42)

The variance and standard deviation of GenLabs returns are:

(Multiple Choice)

4.9/5 (38)

Which one of the following would indicate a portfolio is being effectively diversified?

(Multiple Choice)

5.0/5 (37)

Stock A has an expected return of 20%, and stock B has an expected return of 4%. However, the risk of stock A as measured by its variance is 3 times that of stock B. If the two stocks are combined equally in a portfolio, what would be the portfolio's expected return?

(Multiple Choice)

4.9/5 (35)

A portfolio has 25% of its funds invested in Security C and 75% of its funds invested in Security D. Security C has an expected return of 8% and a standard deviation of 6. Security B has an expected return of 10% and a standard deviation of 10. The securities have a coefficient of correlation of .6. Which of the following values is closest to portfolio return and variance?

(Multiple Choice)

4.9/5 (52)

You've owned a share of stock for 6 years. It returned 5% in 3 of those years and -5% in the other 3. What was the variance?

(Multiple Choice)

4.9/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)