Exam 13: Accounting Information Systems and Adjusting Entries: A Comprehensive Guide

Exam 1: The Canadian Financial Reporting Environment74 Questions

Exam 2: Conceptual Framework Underlying Financial Reporting81 Questions

Exam 3: Measurement31 Questions

Exam 4: Reporting Financial Performance125 Questions

Exam 5: Financial Position and Cash Flows103 Questions

Exam 6: Revenue Recognition117 Questions

Exam 7: Cash and Receivables114 Questions

Exam 8: Inventory168 Questions

Exam 9: Investments128 Questions

Exam 10: Property, Plant, and Equipment: Accounting Model Basics99 Questions

Exam 11: Depreciation, Impairment, and Disposition88 Questions

Exam 12: Intangible Assets and Goodwill104 Questions

Exam 13: Accounting Information Systems and Adjusting Entries: A Comprehensive Guide86 Questions

Select questions type

Which type of account is always debited during the closing process?

(Multiple Choice)

4.9/5  (33)

(33)

An external event involving a transfer or exchange between two or more entities or parties is called a(n)

(Multiple Choice)

4.8/5 (36)

In the closing process, all the revenue and expense accounts are transferred to a clearing or suspense account called

(Multiple Choice)

4.8/5 (40)

Lime Limited has received its invoice for $ 75,000 for property taxes for the calendar year 2020. The invoice was received and paid in June 2020 and the entire amount was debited to Property Tax Expense. Assuming Lime does NOT prepare interim financial statements, the required adjustment on December 31, 2020, related to the property taxes is

(Multiple Choice)

4.9/5 (43)

Adjusting entries

Present, in journal form, the adjustments that would be made on July 31, 2020, the end of the fiscal year, for each of the following:

1. The supplies inventory on August 1, 2019, was $ 8,350. Supplies costing $ 16,650 were purchased during the fiscal year and debited to Supplies Inventory. A count on July 31, 2020, indicated supplies on hand of $ 6,810.

2. On April 30, a ten-month, 4% note for $ 40,000 was received from a customer.

3. On March 1, $ 8,400 was collected as rent for one year and a nominal (temporary) account was credited.

(Essay)

4.9/5 (46)

A corporation's net income or loss is closed at year end to

(Multiple Choice)

4.7/5 (29)

Calculation of revenue

The records for Oriole Corp. showed the following for 2020:

Unearned revenue............................... \3 ,000 \3 ,400 Accrued revenue................................... 1,400 1,100 Cash collected during the year from revenue....... \8 5,000

Instructions

Show the calculation of the amount of revenue that should be reported on the 2020 statement of comprehensive income.

(Essay)

4.8/5 (27)

Which of the following must be considered in estimating depreciation on an asset for an accounting period?

(Multiple Choice)

4.8/5 (38)

Preparing financial statements

The adjusted trial balance of Ryan Financial Planners appears below.

Instructions

Using the information from the adjusted trial balance, you are to prepare for the month ended December 31:

a) an income statement.

b) a retaired eamings statement.

c) a balence sheet.

Ryan Financial Planners

Adjusted Trial Balance

December 31, 2020

Cash........................................................................ Accounts Receivable................................................ Supplies................................................................... Equipment................................................................ Accumulated Depreciation-Equipment..................... Accounts Payable..................................................... Unearned Service Revenue....................................... Common Shares........................................................ Retained Earnings..................................................... Dividends.................................................................. Service Revenue....................................................... Supplies Expense.................................................... Depreciation Expense............................................. Rent Expense......................................................... \2 ,900 2,200 1,800 16,000 2,000 600 2,500 \ 4,000 3,300 5,000 10,000 4,400 4,200

(Essay)

4.9/5 (43)

Use the following information for the following questions:

Orange Corp reported the following items on its calendar 2020 statement of comprehensive income:

Interest revenue..................... \8 4,200 Salaries expense..................... 72,000 Insurance expense.................. 10,600

As well, their statements of financial position showed the following balances:

Accrued interest receivable................ \1 0,100 \8 ,800 Accrued salaries payable................... 9,800 5,400 Prepaid insurance.............................. 1,500 1,600

-The cash paid for insurance premiums during 2020 was

(Multiple Choice)

4.8/5 (40)

Accrual accounting

Prudence Corp.'s records provide the following information concerning certain account balances and changes in these account balances during the current year. Transaction information is missing from each item below.

Instructions

Prepare the entry to record the missing information for each account. (Consider each independently.)

1. Accounts Receivable: Jan 1, balance $ 30,000, Dec 31, balance $ 37,000, uncollectible accounts written off during the year, $ 4,000; accounts receivable collected during the year, $ 134,000. Prepare the entry to record sales for the year.

2. Allowance for Doubtful Accounts: Jan 1, balance $ 3,800, Dec 31 balance $ 7,700, uncollectible accounts written off during the year, $ 28,000. Prepare the entry to record bad debt expense.

3. Accounts Payable: Jan 1, balance $ 20,000, Dec 31, balance $ 33,000, purchases on account for the year, $ 110,000. Prepare the entry to record payments on account.

4. Interest Receivable: Jan 1 accrued, $ 3,000, Dec 31 accrued, $ 3,500, earned for the year, $ 14,000. Prepare the entry to record cash interest received.

(Essay)

4.9/5 (39)

Recordable events

Before transactions are entered into a corporation's accounting system, the underlying event must be analyzed, to determine how (and if) it should be recorded. The situations below relate to Maxwell Corporation:

Instructions

Indicate whether the items below are recordable events.

1. A new mortgage contract for its new factory building is signed.

2. The first mortgage payment is made.

3. Wages for the current month are paid.

4. A new secretary is hired.

5. Property taxes are paid.

6. HST collections for the current month are forwarded to the CRA.

(Essay)

4.8/5 (34)

Adjusting entries

Reed Co. wishes to record receipts and payments in such a manner that adjustments at the end of the period will NOT require reversing entries at the beginning of the next period.

Instructions

Record the following transactions in the desired manner; as well, record the adjusting entry on December 31, 2020. (Two entries for each part.)

1. An insurance policy for two years was purchased on April 1, 2020, for $ 18,000.

2. Rent of $ 12,000 for six months for a portion of the building was received on November 1, 2020.

(Essay)

4.8/5 (36)

Use the following information for the following questions:

During the 2020 calendar year, Purple Corp. paid or collected the following items:

Insurance premiums paid................... \1 4,200 Interest collected................................ 21,700 Salaries paid....................................... 131,300

As well, the comparative statement of financial position showed the following balances:

Prepaid Insurance..................... \1 ,400 \1 ,500 Interest Receivable..................... 2,800 2,100 Salaries Payable.......................... 14,700 12,900

-The insurance expense on the 2019 statement of comprehensive income was

(Multiple Choice)

4.8/5 (31)

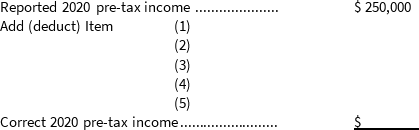

Adjusting entries

Part I - Maison Corp. has reported pre-tax income of $ 250,000 for calendar 2020, before considering the five items below. Prepare the adjusting entries needed at December 31, 2020 in order to correctly state the 2020 pre-tax income. If no entry is needed, write NONE.

1. Interest on a $ 42,000, 7%, six-year note payable was last paid on September 1, 2019.

2. On May 31, 2020, Maison entered into a contract to provide services to a customer for 18 months beginning June 1. The customer paid the $ 18,000 fee in full on June 1 and Maison credited it to Service Revenue.

3. On August 1, 2020, Maison paid a year's rent in advance on a warehouse, and debited the $ 48,000 payment to Prepaid Rent.

4. Depreciation on office equipment for 2020 is $ 17,000.

5. On December 18, 2020, Maison paid the local newspaper $ 1,000 for an advertisement to be run in January of 2021, debiting it to Prepaid Advertising.

Part II - Show the effect of each adjusting entry in Part I on previously reported pre-tax income, and indicate the correct amount of pre-tax income.

(Essay)

4.8/5 (37)

Frog Corporation had revenues of $ 300,000, expenses of $ 200,000, and dividends of $ 45,000. When Income Summary is closed to Retained Earnings, the amount of the debit or credit to Retained Earnings is a

(Multiple Choice)

4.9/5 (34)

The book of original entry where transactions and other selected events are first recorded is called the

(Multiple Choice)

4.9/5 (35)

Use the following information to prepare a multi-step Statement of Comprehensive Income, a Statement of Changes in Shareholders Equity, and a classified Statement of Financial Position.

-Other Data:

1. Salaries expense is 70% selling and 30% administrative.

2. Rent expense and utilities expense are 80% selling and 20% administrative.

3. $ 60,000 of notes payable are due for payment within 12 months.

4. Repair expense is 100% administrative.

-Other Data:

1. Salaries expense is 70% selling and 30% administrative.

2. Rent expense and utilities expense are 80% selling and 20% administrative.

3. $ 60,000 of notes payable are due for payment within 12 months.

4. Repair expense is 100% administrative.

(Essay)

4.8/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)