Exam 2: Principles of Accounting and Financial Reporting for State and Local Governments

Exam 1: Introduction to Accounting and Financial Reporting for Governmental and Not-For-Profit Entities48 Questions

Exam 2: Principles of Accounting and Financial Reporting for State and Local Governments50 Questions

Exam 3: Governmental Operating Statement Accounts; Budgetary Accounting67 Questions

Exam 4: Accounting for Governmental Operating Activitiesillustrative Transactions and Financial Statements85 Questions

Exam 5: Accounting for General Capital Assets and Capital Projects87 Questions

Exam 6: Accounting for General Long-Term Liabilities and Debt Service82 Questions

Exam 7: Accounting for the Business-Type Activities of State and Local Governments85 Questions

Exam 8: Accounting for Fiduciary Activities Agency and Trust Funds56 Questions

Exam 9: Financial Reporting of State and Local Governments50 Questions

Exam 10: Analysis of Governmental Financial Performance48 Questions

Exam 11: Auditing of Governmental and Not-For-Profit Organizations51 Questions

Exam 12: Budgeting and Performance Measurement58 Questions

Exam 13: Accounting for Not-For-Profit Organizations65 Questions

Exam 14: Not-For-Profit Organizations Regulatory, taxation, and Performance Issues56 Questions

Exam 15: Accounting for Colleges and Universities41 Questions

Exam 16: Accounting for Health Care Organizations46 Questions

Exam 17: Accounting and Reporting for the Federal Government52 Questions

Select questions type

The basis of accounting that should be used in preparing fund financial statements is:

Free

(Multiple Choice)

5.0/5  (41)

(41)

Correct Answer: Verified

Verified

C

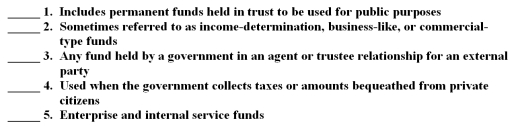

The following are categories of funds described in Chapter 2:

A.Governmental funds

B.Proprietary funds

C.Fiduciary funds

Free

(Short Answer)

4.8/5 (37)

Correct Answer:Verified

1.A,2.B,3.C,4.C,5.B

A fund is an accounting but not a fiscal entity.

Free

(True/False)

4.8/5 (30)

Correct Answer:Verified

False

Reporting fund financial information in separate columns for each major fund and aggregate information for nonmajor funds

(Multiple Choice)

4.8/5 (31)

"Capital assets of a government unit should always be reported on the same basis as a business-depreciated historical cost." Do you agree? Why or why not?

(Essay)

4.9/5 (37)

Financial resources set aside to pay principal and interest on general long-term debt may be accounted for in which of the following fund types?

(Multiple Choice)

4.9/5 (33)

Budgetary comparison schedules presenting budgeted versus actual revenues and expenditures are

(Multiple Choice)

4.9/5 (42)

The activities of a water utility department,which offers its services to the general public on a user charge basis,should be accounted for in

(Multiple Choice)

4.9/5 (40)

The accrual basis of accounting applicable to proprietary fund types requires that exchange revenues be recognized when

(Multiple Choice)

4.9/5 (29)

The accounting system used by a state or local government must make it possible

(Multiple Choice)

4.9/5 (36)

Which of the following organizations should not be included as part of the governmental reporting entity?

(Multiple Choice)

4.8/5 (34)

An objective of the accounting system for a state or a local government is to make it possible both to present fairly the funds and activities of the government in conformity with generally accepted accounting principles and to demonstrate compliance with finance-related legal and contractual provisions.

(True/False)

4.8/5 (38)

In accounting for state and local governments the modified accrual basis is required for

(Multiple Choice)

4.9/5 (39)

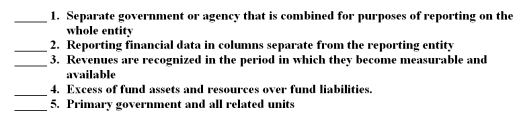

The following are key terms in Chapter 2 that relate to principles of accounting and financial reporting for state and local governments:

A.Fund equity

B.Modified accrual basis

C.Reporting entity

D.Discrete presentation

E.Component unit

F.Accrual basis

G.Blended presentation

H.Governmental activities

For each of the following definitions,indicate the key term from the list above that best matches by placing the appropriate letter in the blank space next to the definition.

(Short Answer)

4.9/5 (39)

Describe why a combining balance sheet might be prepared for governmental funds of a government.

(Essay)

5.0/5 (37)

Explain the difference between measurement focus and basis of accounting.Also,explain the difference between the economic resources measurement focus and the current financial resources measurement focus as well as the difference between the accrual and modified accrual bases of accounting.Which funds and government-wide activities use each focus and each basis?

(Essay)

4.8/5 (37)

Generally accepted accounting principles applicable to state and local governments require that

(Multiple Choice)

4.8/5 (36)

The governmental funds category includes the General Fund,special revenue funds,debt service funds,capital projects funds,and internal service funds.

(True/False)

4.8/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)