Exam 3: Adjusting Accounts for Financial Statements

Exam 1: Accounting in Business331 Questions

Exam 2: Analyzing for Business Transactions293 Questions

Exam 3: Adjusting Accounts for Financial Statements445 Questions

Exam 4: Accounting for Merchandising Operations267 Questions

Exam 5: Inventories and Cost of Sales258 Questions

Exam 6: Cash, fraud, and Internal Controls230 Questions

Exam 7: Accounting for Receivables237 Questions

Exam 8: Accounting for Long-Term Assets283 Questions

Exam 9: Accounting for Current Liabilities258 Questions

Exam 10: Accounting for Long-Term Liabilities250 Questions

Exam 11: Corporate Reporting and Analysis247 Questions

Exam 12: Reporting Cash Flows265 Questions

Exam 13: Analysis of Financial Statements263 Questions

Exam 14: Time Value of Money84 Questions

Exam 15: Investments228 Questions

Exam 16: Partnership Accounting189 Questions

Select questions type

It is acceptable to record prepayment of expenses as debits to expense accounts if an adjusting entry is made at the end of the period to bring the asset account balance to the correct unused or unexpired amount.

(True/False)

4.8/5  (42)

(42)

Match the following terms with the appropriate definition.

-A method that allocates equal amounts of an asset's cost (less any salvage value)to depreciation expense during its useful life.

(Multiple Choice)

4.9/5 (41)

Wilson Company paid $4,800 for a 4-month insurance premium in advance on November 1,with coverage beginning on that date.The balance in the prepaid insurance account before adjustment at the end of the year is $4,800 and no adjustments had been made previously.The adjusting entry required on December 31 is:

(Multiple Choice)

4.9/5 (37)

Match the following terms with the appropriate definition.

-Items paid for in advance of receiving their benefits; recorded as an asset when purchased and expensed when used.

(Multiple Choice)

4.9/5 (42)

All of the following are true regarding unearned revenues except:

(Multiple Choice)

4.8/5 (38)

________ revenues are liabilities requiring delivery of products and for services.

(Short Answer)

4.8/5 (35)

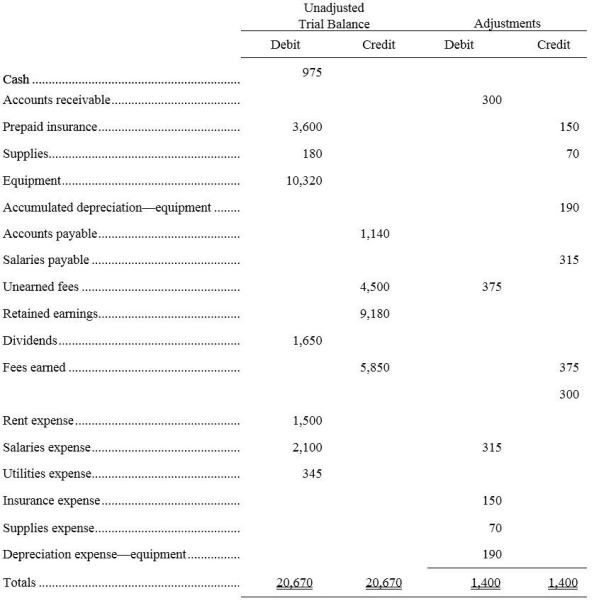

A company's December 31 work sheet for the current period appears below.Based on the information provided,what is net income for the current period?

(Multiple Choice)

4.7/5 (40)

Closing entries are required at the end of each accounting period to close all ledger accounts.

(True/False)

4.9/5 (38)

If a prepaid expense account were not adjusted for the amount used,on the balance sheet assets would be ________ and equity would be ________.

(Short Answer)

4.9/5 (33)

A company shows a $600 balance in Prepaid Rent in the Unadjusted Trial Balance columns of the work sheet.The Adjustments columns show expired rent of $200.This adjusting entry results in:

(Multiple Choice)

4.9/5 (29)

The expense recognition (matching)principle does not aim to record expenses in the same accounting period as the revenue earned as a result of these expenses.

(True/False)

4.8/5 (34)

Adjusting entries are necessary so that asset,liability,revenue,and expense account balances are correctly recorded.

(True/False)

4.9/5 (32)

Record the December 31 adjusting entries for the following transactions and events in general journal form.Assume that December 31 is the end of the annual accounting period.

a.The Prepaid Insurance account shows a debit balance of $2,340,representing the cost of a two-year fire insurance policy that was purchased on October 1 of the current year and has not been adjusted to-date.

b.The Store Supplies account has a debit balance of $400; a year-end inventory count reveals $80 of supplies still on hand.

c.On November 1 of the current year,Rent Earned was credited for $1,500.This amount represented the rent earned for a three-month period beginning November 1.

d.Estimated depreciation on store equipment is $600.

e.Accrued salaries amount to $1,400.

(Essay)

5.0/5 (33)

Farmers' net income was $740,000 and its net sales were $8,000,000.Calculate its profit margin ratio.

(Essay)

4.7/5 (36)

Asset and liability balances are transferred from the adjusted trial balance to the income statement.

(True/False)

4.8/5 (42)

Financial statements are typically prepared in the following order:

(Multiple Choice)

4.7/5 (33)

Werner Company had $1,300 of store supplies at the beginning of the current year.During this year,Werner purchased $6,250 worth of store supplies.On December 31,$1,125 worth of store supplies remained.Calculate the amount of Werner Company's store supplies expense for the current year.

(Essay)

4.8/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)