Exam 3: Adjusting Accounts and Preparing Financial Statements

Exam 1: Accounting in Business298 Questions

Exam 2: Analyzing and Recording Transactions253 Questions

Exam 3: Adjusting Accounts and Preparing Financial Statements247 Questions

Exam 4: Completing the Accounting Cycle186 Questions

Exam 5: Accounting for Merchandising Operations258 Questions

Exam 6: Inventories and Cost of Sales232 Questions

Exam 7: Accounting Information Systems177 Questions

Exam 8: Cash and Internal Controls220 Questions

Exam 9: Accounting for Receivables217 Questions

Exam 10: Plant Assets Natural Resoures and Intangibles245 Questions

Exam 11: Current Liabilities and Payroll Accounting210 Questions

Exam 12: Accounting for Partnerships172 Questions

Exam 13: Accounting for Corporations228 Questions

Exam 14: Long-Term Liabilities234 Questions

Exam 15: Investments220 Questions

Exam 16: Reporting the Statement of Cash Flows237 Questions

Exam 17: Analysis of Financial Statements235 Questions

Exam 18: Managerial Accounting Concepts and Principles246 Questions

Exam 19: Job Order Costing213 Questions

Exam 20: Process Costing230 Questions

Exam 21: Cost-Volume-Profit Analysis244 Questions

Exam 22: Master Budgets and Planning216 Questions

Exam 23: Flexible Budgets and Standard Costs223 Questions

Exam 24: Performance Measurement and Responsibility Accounting208 Questions

Exam 25: Capital Budgeting and Managerial Decisions190 Questions

Exam 26: Present and Future Values in Accounting84 Questions

Exam 27: Activity-Based Costing70 Questions

Select questions type

It is acceptable to record cash received in advance of providing products or services to revenue accounts if an adjusting entry is made at the end of the period to bring the liability account balance to the correct unearned amount.

(True/False)

4.7/5  (39)

(39)

____________ is the process of allocating the cost of plant assets to the income statement over their expected useful lives.

(Short Answer)

4.8/5 (34)

Andrew's net income was $280,000; its total assets were $1,050,000; and its net sales were

$3,500,000. Calculate the company's profit margin ratio.

(Essay)

4.8/5 (33)

________ expenses are those costs that are incurred in a period but are both unpaid and unrecorded.

(Short Answer)

4.8/5 (34)

A company had no office supplies available at the beginning of the year. During the year, the company purchased $250 worth of office supplies. On December 31, $75 worth of office supplies remained. How much should the company report as office supplies expense for the year?

(Multiple Choice)

4.7/5 (32)

Depreciation expense for a period is the portion of a plant asset's cost that is allocated to that period.

(True/False)

4.9/5 (48)

A company owes its employees $5,000 for the year ended December 31. It will pay employees on January 6 for the previous two weeks' salaries. The year-end adjusting entry on December 31 will include a debit to Salaries Expense and a credit to Cash.

(True/False)

4.9/5 (35)

Before an adjusting entry is made to accrue employee salaries, Salaries Expense and Salaries Payable are both understated.

(True/False)

4.9/5 (33)

Record the December 31 adjusting entries for the following transactions and events in general journal form. Assume that December 31 is the end of the annual accounting period.

a. The Prepaid Insurance account shows a debit balance of $2,340, representing the cost of a

two-year fire insurance policy that was purchased on October 1 of the current year and has not been adjusted to-date.

b. The Store Supplies account has a debit balance of $400; a year-end inventory count reveals $80 of supplies still on hand.

c. On November 1 of the current year, Rent Earned was credited for $1,500. This amount represented the rent earned for a three-month period beginning November 1.

d. Estimated depreciation on store equipment is $600.

e. Accrued salaries amount to $1,400.

(Essay)

4.9/5 (31)

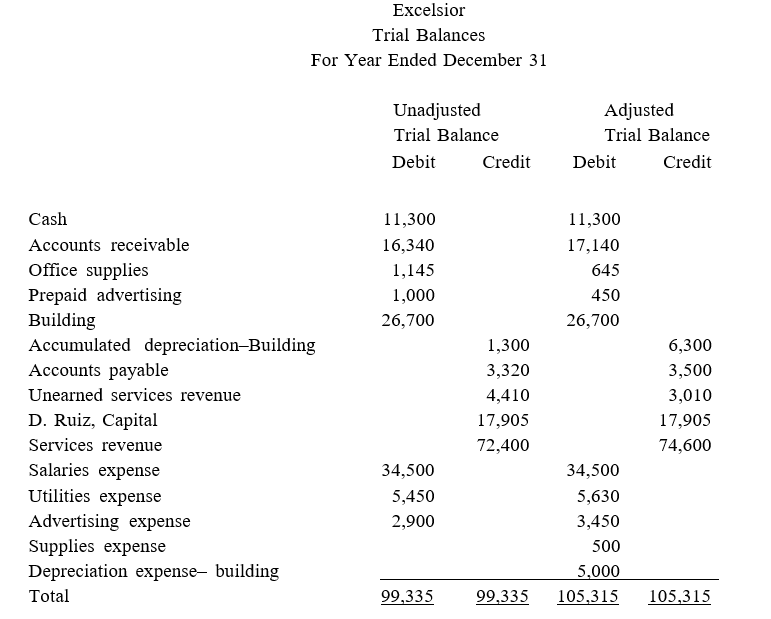

The following unadjusted and adjusted trial balances are from the current year's accounting system for Excelsior.

Present the six adjusting entries in general journal form that explain the changes in the account balances from the unadjusted to the adjusted trial balance.

Present the six adjusting entries in general journal form that explain the changes in the account balances from the unadjusted to the adjusted trial balance.

(Essay)

4.8/5 (38)

________ revenues are liabilities requiring delivery of products and for services.

(Short Answer)

4.7/5 (34)

A balance sheet that places the assets above the liabilities and equity is called a(n):

(Multiple Choice)

4.9/5 (41)

Match the following definitions with the appropriate term

Correct Answer: Verified

Verified

Premises:

Responses:

(Matching)

4.9/5 (34)

Asset and liability balances are transferred from the adjusted trial balance to the balance sheet.

(True/False)

4.8/5 (37)

A company purchased a new delivery van at a cost of $45,000 on July 1. The delivery van is estimated to have a useful life of 6 years and a salvage value of $3,000. The company uses the straight-line method of depreciation. How much depreciation expense will be recorded for the van during the first year ended December 31?

(Multiple Choice)

4.8/5 (39)

On September 1, Kennedy Company loaned $100,000, at 12% annual interest, to a customer. Interest and principal will be collected when the loan matures one year from the issue date. Assuming adjustments are only made at year-end, what is the adjusting entry for accruing interest that Kennedy would need to make on December 31, the calendar year-end?

(Multiple Choice)

4.9/5 (41)

Farmers' net income was $740,000 and its net sales were $8,000,000. Calculate its profit margin ratio.

(Essay)

4.9/5 (32)

Incurred but unpaid expenses that are recorded during the adjusting process with a debit to an expense and a credit to a liability are:

(Multiple Choice)

4.9/5 (40)

Rogers Company's employees are paid a total of $1,600 per day for a 5-day workweek. The employees are paid each Friday. This year the accounting period ends on Tuesday. Prepare the December 31 year-end adjusting journal entry Rogers Company should make to accrue salaries.

(Essay)

4.8/5 (37)

Accrued revenues at the end of one accounting period often result in cash ________ in the next period.

(Short Answer)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)