Exam 11: Optimal Portfolio Choice and the Capital Asset Pricing Model

Exam 1: The Corporation38 Questions

Exam 2: Introduction to Financial Statement Analysis103 Questions

Exam 3: Financial Decision Making and the Law of One Price89 Questions

Exam 4: The Time Value of Money91 Questions

Exam 5: Interest Rates68 Questions

Exam 6: Valuing Bonds115 Questions

Exam 7: Investment Decision Rules86 Questions

Exam 8: Fundamentals of Capital Budgeting95 Questions

Exam 9: Valuing Stocks96 Questions

Exam 10: Capital Markets and the Pricing of Risk103 Questions

Exam 11: Optimal Portfolio Choice and the Capital Asset Pricing Model134 Questions

Exam 12: Estimating the Cost of Capital104 Questions

Exam 13: Investor Behavior and Capital Market Efficiency77 Questions

Exam 14: Capital Structure in a Perfect Market99 Questions

Exam 15: Debt and Taxes95 Questions

Exam 16: Financial Distress,managerial Incentives,and Information111 Questions

Exam 17: Payout Policy96 Questions

Exam 18: Capital Budgeting and Valuation With Leverage99 Questions

Exam 19: Valuation and Financial Modeling: a Case Study49 Questions

Select questions type

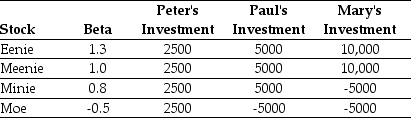

Use the table for the question(s)below.

Consider the following three individuals portfolios consisting of investments in four stocks:

-Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then required return on Peter's portfolio is closest to:

-Assuming that the risk-free rate is 4% and the expected return on the market is 12%,then required return on Peter's portfolio is closest to:

Free

(Multiple Choice)

4.8/5  (41)

(41)

Correct Answer: Verified

Verified

C

Suppose that you want to maximize your expected return without increasing your risk.How can you achieve this goal? Without increasing your risk,what is the maximum expected return you can expect?

Free

(Essay)

4.8/5 (38)

Correct Answer:Verified

By investing in a combination of the risk-free asset and the efficient portfolio.We find the weights and expected returns as follows: SD( Rxp)= xSD(Rp) .10 = x(.12) x = .10/.12 x = .833333 invested in the efficient portfolio So,E[Rxp] = rf + x(E[Rp] - rf) = .05 + .8333(.17 - .05)= .15 or 15%

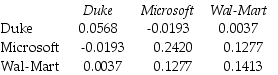

Use the table for the question(s)below.

Consider the following covariances between securities:

-The variance on a portfolio that is made up of a $6000 investments in Microsoft and a $4000 investment in Wal-Mart stock is closest to:

-The variance on a portfolio that is made up of a $6000 investments in Microsoft and a $4000 investment in Wal-Mart stock is closest to:

Free

(Essay)

4.8/5 (36)

Correct Answer:Verified

Total invested = $6000 + $4000 = $10,000 XMicrosoft =  = .60 XWal-Mart =

= .60 XWal-Mart =  = .40 Var(Rp)= x12Var(R1)+ x22Var(R2)+ 2X1X2Cov(R1,R2) = (.60)2(0.2420)+ (.40)2(0.1413)+ 2(.6)(.4)(0.1277)= 0.1710

= .40 Var(Rp)= x12Var(R1)+ x22Var(R2)+ 2X1X2Cov(R1,R2) = (.60)2(0.2420)+ (.40)2(0.1413)+ 2(.6)(.4)(0.1277)= 0.1710

The expected return of a portfolio that consists of a long position of $10,000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

(Multiple Choice)

4.9/5 (27)

Use the following information to answer the question(s)below.

The volatility of the market portfolio is 10%,the expected return on the market is 12%,and the risk-free rate of interest is 4%.

-The beta of the precious metals fund with the Luther Fund

The volatility of the market portfolio is 10%,the expected return on the market is 12%,and the risk-free rate of interest is 4%.

-The beta of the precious metals fund with the Luther Fund  is closest to:

is closest to:

(Multiple Choice)

4.8/5 (37)

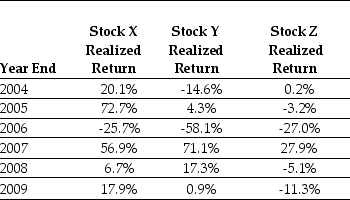

Use the table for the question(s)below.

Consider the following returns:

-Calculate the variance on a portfolio that is made up of equal investments in Stock Y and Stock Z stock.

-Calculate the variance on a portfolio that is made up of equal investments in Stock Y and Stock Z stock.

(Essay)

4.9/5 (45)

Use the following information to answer the question(s)below.

The volatility of the market portfolio is 10%,the expected return on the market is 12%,and the risk-free rate of interest is 4%.

-Suppose that Google stock has a beta of 1.06 and Boeing stock has a beta of 1.31.If the risk-free interest rate is 4% and the expected return from the market portfolio is 12%,then the expected return on a portfolio that consists of 30% Google stock and 70% Boeing stock is closest to:

The volatility of the market portfolio is 10%,the expected return on the market is 12%,and the risk-free rate of interest is 4%.

-Suppose that Google stock has a beta of 1.06 and Boeing stock has a beta of 1.31.If the risk-free interest rate is 4% and the expected return from the market portfolio is 12%,then the expected return on a portfolio that consists of 30% Google stock and 70% Boeing stock is closest to:

(Multiple Choice)

4.9/5 (34)

Use the following information to answer the question(s)below.

The volatility of the market portfolio is 10%,the expected return on the market is 12%,and the risk-free rate of interest is 4%.

-The beta for Sisyphean's new project is closest to:

(Multiple Choice)

4.8/5 (38)

Use the following information to answer the question(s)below.

The volatility of the market portfolio is 10%,the expected return on the market is 12%,and the risk-free rate of interest is 4%.

-The Sharpe Ratio for Wyatt Oil is closest to:

(Multiple Choice)

4.8/5 (43)

The volatility of a portfolio that consists of a long position of $10,000 in Wal-Mart and a short position of $2000 in Microsoft is closest to:

(Multiple Choice)

4.8/5 (39)

The expected return of a portfolio that is equally invested in Duke Energy and Microsoft is closest to:

(Multiple Choice)

4.8/5 (41)

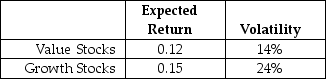

Use the following information to answer the question(s)below.

Suppose that all stocks can be grouped into two mutually exclusive portfolios (with each stock appearing in only one portfolio): growth stocks and value stocks.Assume that these two portfolios are equal in size (market value),the correlation of their returns is equal to 0.6,and the portfolios have the following characteristics:

The risk free rate is 3.5%.

-The Sharpe ratio for the market (which is a 50-50 combination of the value and growth portfolios)portfolio is closest to:

The risk free rate is 3.5%.

-The Sharpe ratio for the market (which is a 50-50 combination of the value and growth portfolios)portfolio is closest to:

(Multiple Choice)

4.8/5 (31)

You currently own $100,000 worth of Wal-Mart stock.Suppose that Wal-Mart has an expected return of 14% and a volatility of 23%.The market portfolio has an expected return of 12% and a volatility of 16%.The risk-free rate is 5%.Assuming the CAPM assumptions hold,what alternative investment has the highest possible expected return while having the same volatility as Wal-Mart? What is the expected return of this portfolio?

(Essay)

4.8/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)