Exam 6: How Is Cost-Volume-Profit Analysis Used for Decision Making

Smart Products Inc.produces smart phones.The company has no finished goods inventory at the beginning of year 1.The following information pertains to Smart Products Inc.

Annual production 200,000 units Sales price \ 400 per unit Variable production cost per unit: Direct materials \ 120 Direct labor 60 Manufacturing overhead 80 Total variable cost per unit \ 260 per unit Fixed production costs \ 400,000 each year; \ 2 per unit at 200,000 units of production Variable selling and admin. cost \ 20 per unit Fixed selling and admin. costs \ 400,000 each year

(1) All 200,000 units produced during year 1 are sold during year 1 .

a. Prepare a traditional income statement assuming the company uses absorption costing.

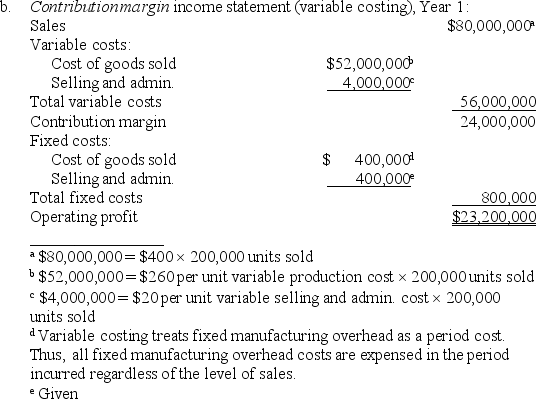

b. Prepare a contribution margin income statement assuming the company uses variable costing

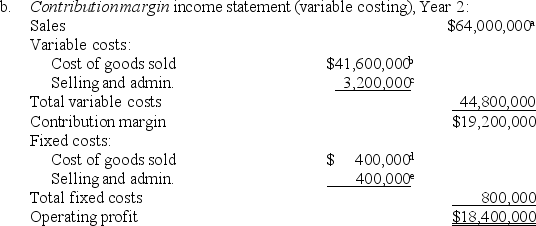

(2) Although 200,000 units are produced during year 2 , only 160,000 are sold during the year. The remaining 40,000 units are in finished goods inventory at the end of year 2 .

a. Prepare a traditional income statement assuming the company uses absorption costing.

b. Prepare a contribution margin income statement assuming the company uses variable costing

(1) a. Traditional incorne statement (absorption costing), Year I:

units sold

per unit fixed production cost units sold

($260 per unit variable production cost units sold)

fixed selling and admin. cost per unit

variable selling and admin. cost units sold)

(2) a. Traditional incorme statement (absoption costing), Year 2:

units sold

per unit fixed production cost units sold ($260 per unit variable production cost units sold)

fixed selling and admin. cost per unit

variable selling and admin. cost units sold)

units sold

units sold

per unit variable production cost units sold

per unit variable selling and admin. cost units sold

Variable costing treats fixed manufacturing overhead as a period cost. Thus, all fixed manufacturing overhead costs are expensed in the period incurred regardless of the level of sales.

Given

Absorption costing treats all manufacturing costs as period costs.

False

It is important for all profit and non-profit companies to determine their profit desired after accounting for income taxes.

False

The margin of safety cannot be calculated for multiple product and service organizations.

The only difference between absorption costing and variable costing is the treatment of fixed manufacturing overhead costs.

Although absorption costing meets the requirements of generally accepted accounting principles,variable costing is typically more useful for internal decision making purposes.

If the number of units produced is more than the number of units sold,which of the following statements is true when comparing operating profit under absorption versus variable costing?

Exhibit 6-4

Sanchez Company produces two different remote control products with the following monthly data for the most recent month:

Plane Boat Total Selling price per unit \ 300 \ 100 Variable cost per unit \ 240 \ 60 Expected unit sales 28,000 7,000 35,000 Sales mix 80\% 20\% 100\% Fixed costs \ 1,400,000

-Refer to Exhibit 6-4.Assume the sales mix remains the same at all levels of sales.

How many units in total must be sold to break even?

Using the information below,identify the mathematical equation used to find total profit.

S= Selling price per unit;

V= Variable cost per unit;

F= Total fixed costs;and

Q= Quantity of units produced and sold

Paddleboard Incorporated builds three products: River,Lake,and Ocean.Information for these three products is shown below:

River Lake Ocean Total Selling price per unit \ 300 \ 250 \ 275 Variable cost per unit \ 175 \ 150 \ 125 Expected unit sales (annual) 14,000 2,000 4,000 20,000 Sales mix 70\% 10\% 20\% 100\%

Total annual fixed costs are $765,000.Assume the sales mix remains the same at all levels of sales.

Assume each scenario below is independent of the other.Unless stated otherwise,assume the variables are the same as in the base case.

(1)Prepare a contribution margin income statement for the base case.

(2)How will total profit change if the Lake sales price increases by 15 percent? (Compare your result with requirement 1 above. )

(3)Go back to the base case.How will total profit change if the River sales volume decreases by 2,000 units and the sales volume of other products remains the same? (Compare your result with requirement 1 above. )

(4)Go back to the base case.How will total profit change if fixed costs decrease by 10 percent? (Compare your result with requirement 1 above. )

Sensitivity analysis can be used to determine how changes in variables will impact target profit.

Exhibit 6-7

Bodega Chocolate,Inc.is a new company that produces a single product.The company has no beginning inventory.During the year the company produced 10,000 units out of which 9,000 were sold.Below are Bodega's costs:

Production \ 4.00 Selling and administrative \ 2.50

Production \2 0,700.00 Selling and administrative \8 5,000

-Refer to Exhibit 6-7.What is the unit product cost using absorption costing?

Which of the following is not found on an income statement prepared using absorption costing?

Exhibit 6-3

Howard Company sells mountain bikes for $1,400 per unit representing 40 percent of total sales,and cruising bikes for $1,000 per unit representing 60 percent of total sales.Variable cost per unit is $600 for mountain bikes and $500 for cruising bikes.

-Refer to Exhibit 6-3.What is the weighted average contribution margin per unit?

Paco's Bikes sells 120 bicycles each month for $400 per unit.Variable cost per unit is $160 and fixed costs total $4,800 per month.What is the contribution margin per unit?

Contribution margin per unit is calculated by subtracting variable costs per unit and fixed costs per unit from the selling price per unit.

Exhibit 6-2

Victor Company makes a single product.The company has monthly fixed costs totaling $200,000 and variable costs of $20 per unit.Each unit of product is sold for $35.Brevard expects to sell 25,000 units each month.

-Refer to Exhibit 6-2.What would be the operating profit if the unit variable cost decreases 20 percent?

Target profit before taxes is calculated as target profit after tax divided by one minus the tax rate.

Exhibit 6-8

Perry,Inc.produced 15,000 units during the year.Of these,12,000 were sold for $50 each.Other Perry,Inc.data are as follows:

Direct materials \ 8.00 per unit Direct labor \ 6.00 per unit Variable manufacturing overhead \ 2.00 per unit Variable selling and administrative costs \ 1.00 per unit Fixed manufacturing overhead \7 5,000 Fixed selling and administrative costs \5 0,000

-Refer to Exhibit 6-8.Calculate Perry's operating profit assuming the company uses variable costing.

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)