Exam 12: Interim Reporting and Disclosures About Segments of an Enterprise

Exam 1: Business Combinations: New Rules for a Long-Standing Business Practice48 Questions

Exam 2: Consolidated Statements: Date of Acquisition44 Questions

Exam 3: Consolidated Statements: Subsequent to Acquisition37 Questions

Exam 4: Intercompany Transactions: Merchandise, Plant Assets, and Notes43 Questions

Exam 5: Intercompany Transactions: Bonds and Leases54 Questions

Exam 6: Cash Flow, Eps, and Taxation48 Questions

Exam 7: Special Issues in Accounting for an Investment in a Subsidiary42 Questions

Exam 8: Subsidiary Equity Transactions, Indirect Subsidiary Ownership, and Subsidiary Ownership of Parent Shares41 Questions

Exam 9: The International Accounting Environment17 Questions

Exam 10: Foreign Currency Transactions75 Questions

Exam 11: Translation of Foreign Financial Statements79 Questions

Exam 12: Interim Reporting and Disclosures About Segments of an Enterprise63 Questions

Exam 13: Partnerships: Characteristics, Formation, and Accounting for Activities36 Questions

Exam 14: Partnerships: Ownership Changes and Liquidations47 Questions

Exam 15: Government and Not for Profit Accounting44 Questions

Exam 16: Governmental Accounting: Other Governmental Funds, Proprietary Funds, and Fiduciary Funds60 Questions

Exam 17: Financial Reporting Issues37 Questions

Exam 18: Accounting for Private Not-For-Profit Organizations61 Questions

Exam 19: Accounting for Not-For-Profit Colleges and Universities and Health Care Organizations83 Questions

Exam 20: Estates and Trusts: Their Nature and the Accountants Role56 Questions

Exam 21: Debt Restructuring, Corporate Reorganizations, and Liquidations49 Questions

Exam 22: Derivatives and Related Accounting Issues60 Questions

Exam 23: Equity Method for Unconsolidated Investments25 Questions

Exam 24: Variable Interest Entities10 Questions

Select questions type

The following events took place in Morgan Corporation's second quarter.

?

a.An expired insurance policy was replaced by a $12,000, 12-month policy.?

?

b.Morgan sold marketable securities at a $10,000 gain.?

?

c.Research and development costs of $15,000, which were expected to benefit the company over the next 12 months, were incurred.?

?

d.On the first day of the quarter, Morgan signed a one-year, $100,000 bank note carrying an 8% interest rate.?

?

e.Used equipment with a book value of $36,000 was sold for $18,000.?

Required:

?

Determine the effect of the above events on Morgan Corporation's second-quarter income.

(Essay)

4.8/5  (40)

(40)

During the first quarter, a company's application of lower of cost or market methods indicated a $150,000 loss from a temporary market decline, which is expected to be restored in the fiscal year.During the second quarter, the market reversed the decline.Which of the following situations indicates a proper treatment of these facts?

(Multiple Choice)

4.8/5 (40)

Which of the following statements is not true concerning the determination of the effective tax rate to be used for interim reporting?

(Multiple Choice)

4.7/5 (46)

Assume there is an interim year-to-date operating loss and a potential tax benefit associated with this loss.Which of the following is true?

(Multiple Choice)

4.9/5 (40)

Corriveau Industries decided to switch from an accelerated depreciation method to a straight-line method in the second quarter of 2016.This is classified as a cumulative effect of a change in accounting principle.The first-quarter, pretax income reported was $30,000, and projected pretax income for 2016 was $90,000.If Corriveau had used straight-line depreciation for the quarter, pretax income would have been $35,000 and projected pretax income for 2016 would have been $110,000.The cumulative effect on prior years from the change is a $50,000 increase in retained earnings.The second-quarter income using straight-line depreciation is $20,000, and the expected annual earnings continue to be $110,000.Assume that Corriveau is subject to a flat 25% statutory tax rate for 2016.Corriveau is expecting $5,000 of tax-free income during the third and fourth quarters of 2016.

Required:

For all categories of income, calculate the interim tax expense for the first quarter, first quarter restated, and second quarter.

(Essay)

4.9/5 (37)

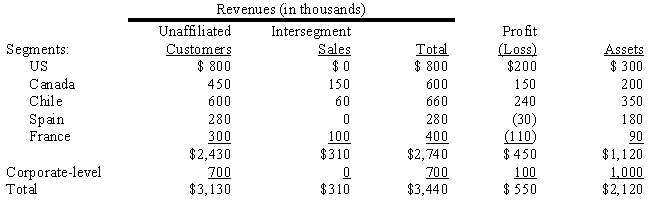

Santas Corporation is a diversified firm with operations in the United States, Canada, Chile, Spain, and France, each of which qualifies as a geographic segment.Data with respect to those segments follows:

?

?

Required:

?

Determine which of the Santas segments would be reportable segments, and explain why.

?

Required:

?

Determine which of the Santas segments would be reportable segments, and explain why.

?

(Essay)

4.8/5 (33)

For interim reporting, which of the following statements is true?

(Multiple Choice)

4.9/5 (35)

Cracker Corporation's first-quarter 2019, pretax income is $55,000.The company anticipates an annual tax credit of $15,500.Cracker is projecting income for the remaining three quarters of $135,000.For the second quarter of 2019, Cracker reports $85,000 of pretax income with a projected pre-tax income for the remainder of the year of $165,000.Cracker does not have any permanent differences between taxable income and financial income.

?

In the second quarter, Cracker suffers an uninsured loss of one of its warehouses.The loss is determined to be unusual in nature and infrequent in occurrence.The amount of the loss is determined to be $140,000.

?

The current tax schedule is:

?

\ 1-\ 100,000 15\% \ 100,001-200,000 22\% \ 200,001-460,000 28\% \ 460,001 and above 30\% Required:

?

Calculate the first and second quarter interim tax expenses on continuing income and on the non-ordinary item.

?

(Essay)

4.9/5 (40)

It is possible for segments to qualify as reportable, but not represent a material portion of the enterprise.What test is applied to ensure the segments reported represent a significant portion of enterprise activity?

(Multiple Choice)

4.8/5 (45)

Futura Corporation reported pretax net income of $30,000 in the first quarter of 2016.The company anticipated pretax net income of $90,000 for the year.During the second quarter, after issuing the first-quarter interim statement, Futura decided to discontinue its electronics division and adopted a formal plan for its disposal.

?

During the first quarter, the electronics division reported a pretax loss of $70,000 and estimated a $270,000 operating loss for the year.During the second quarter, the division experienced an operating loss of $35,000 prior to the measurement date and $8,000 in the remainder of that quarter.The anticipated loss on the disposal of that division's assets was $40,000.

?

Futura had a flat 25% tax rate for 2016.The firm is expecting a $5,000 tax credit attributed to operations outside of the electronic division.Second-quarter pretax income for the non-electronics operations was $40,000.As of the end of the second quarter, annual pretax income of $225,000 was anticipated for continuing operations.

?

Required:

?

In good form, prepare a schedule showing the income (loss) and tax expense (benefit) determination for the first quarter, the restated first quarter, and the second quarter.

(Essay)

4.9/5 (36)

Which of the following best describes the treatment given a change in accounting principles made during the second quarter?

(Multiple Choice)

4.9/5 (40)

Information about the seven segments of the Kenny Corporation is presented below.Determine which of the segments are reportable and why.

?

General and Segment Revenue from Rll Sources Cost of Sales Administrative Expenses Total Assets 1 \ 17,450,000 \ 15,200,000 \ 4,500,000 \ 55,000,000 2 25,200,000 20,000,000 4,000,000 80,000,000 3 9,150,000 7,000,000 1,500,000 28,250,000 4 780,000 300,000 100,000 4,750,000 5 11,500,000 8,900,000 4,250,000 25,500,000 6 6,800,000 3,400,000 2,000,000 12,000,000 7 2,100,000 1,000,000 900,000 10,000,000 Total \ 72,980,000 \ 55,800,000 \ 17,250,000 \ 215,500,000

(Essay)

4.7/5 (40)

When a company makes a second quarter decision to discontinue a segment, the first quarter tax expense:

(Multiple Choice)

4.9/5 (31)

Stidham Company is a large international company with diversified operating segments.These segments include the following:

A.Manufacturing processes in the United States and Europe that produce rubber-coated metal automotive parts which are sold to automobile manufacturers and automotive repair retail shops in the United States, Europe and Japan.

B.Manufacturing processes in the United States that batteries used in military and commercial satellites, and for other military purposes.These products are made of lithium and nickel compounds and are sold primarily to United States government agencies, European governmental agencies and selected commercial customers in the United States and Europe.

C.Manufacturing processes in the United States and Latin America that produce precision-machined automotive parts which are sold to international and American automobile manufacturers, but are shipped only to plants located in the United States and Latin America.

D.Manufacturing processes in the United States that produce traditional acid batteries for commercial applications such as toys and emergency lighting systems.The products are sold primarily in the United States and Asia.

E.Processes where rare minerals are refined and distributed internationally for use in producing solar panels used to power space craft, items used to absorb radiation in nuclear power plants and military optical equipment.Customers are primarily United States and selected European governmental agencies, and selected commercial customers in the United States and Europe.

Given the management approach, discuss various ways in which the segments might be structured.

(Essay)

4.9/5 (43)

Allee Co.has pretax, ordinary income of $7,000 and $38,000 in the first and second quarters, respectively.The projected ordinary income for the third and fourth quarters is $60,000 and $30,000.Occurring in the second quarter is a pretax, non-ordinary loss of $50,000 and pretax non-ordinary income of $35,000.The statutory tax rate is 15% on the first $50,000, 22% on the next $50,000, and 28% on income over $100,000.

Required:

Determine the tax impact traceable to the non-ordinary income and non-ordinary loss.

(Essay)

4.9/5 (37)

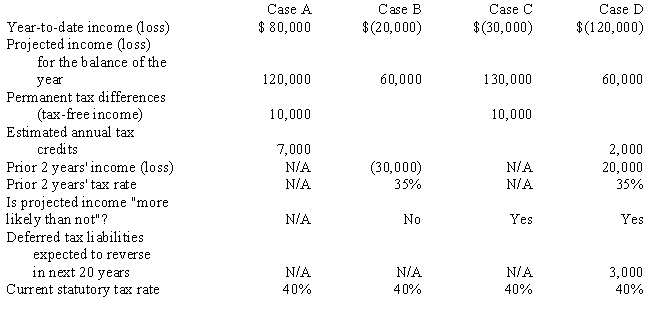

For each of the following independent cases, determine the estimated effective tax rate to be used for the current quarter's interim statements.

?

?

(Essay)

5.0/5 (40)

Which of the following best describes how the tax benefit resulting from the extraordinary loss in an interim period is recognized?

(Multiple Choice)

5.0/5 (44)

With regard to major customers, which of the following items is not true?

(Multiple Choice)

4.9/5 (34)

Explain the difference in the independent and integral viewpoints of accounting for interim periods.Which method best describes the accepted accounting practice for interim financial reporting?

(Essay)

4.9/5 (33)

Lancaster Inc.expects to have taxable income of $275,000 for 2016 and a tax credit of $12,250.Assume that the graduated tax rate schedule is as follows:

?

?

\ 1-\ 100,000 15\% \ 100,001-200,000 22\% \ 200,001-460,000 28\%+5\% surtax \ 460,001 and above 30\% Required:

?

Determine the tax expense for the first quarter, assuming that taxable income is $65,000.

(Essay)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)