Exam 16: Option Contracts

Exam 1: The Investment Setting72 Questions

Exam 1: The Investment Setting: Part A6 Questions

Exam 2: Asset Allocation and Security Selection77 Questions

Exam 2: Asset Allocation and Security Selection: Part A3 Questions

Exam 3: Organization and Functioning of Securities Markets87 Questions

Exam 4: Security Market Indexes and Index Funds89 Questions

Exam 5: Efficient Capital Markets, Behavioral Finance, and Technical Analysis162 Questions

Exam 6: An Introduction to Portfolio Management114 Questions

Exam 6: An Introduction to Portfolio Management: Part A2 Questions

Exam 6: An Introduction to Portfolio Management: Part B2 Questions

Exam 7: Asset Pricing Models152 Questions

Exam 8: Equity Valuation83 Questions

Exam 9: The Top-Down Approach to Market, Industry, and Company Analysis216 Questions

Exam 10: The Practice of Fundamental Investing60 Questions

Exam 11: Equity Portfolio Management Strategies65 Questions

Exam 12: Bond Fundamentals and Valuation138 Questions

Exam 13: Bond Analysis and Portfolio Management Strategies125 Questions

Exam 14: An Introduction to Derivative Markets and Securities102 Questions

Exam 15: Forward, Futures, and Swap Contracts148 Questions

Exam 16: Option Contracts122 Questions

Exam 17: Professional Money Management, Alternative Assets, and Industry Ethics109 Questions

Exam 18: Evaluation of Portfolio Performance111 Questions

Select questions type

The buyer of a straddle expects stock prices to move strongly in either direction.

(True/False)

4.8/5  (40)

(40)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

BioTech Industries has debentures outstanding (par value $1,000) convertible into the company's common stock at $30. The coupon rate is 11 percent payable semiannually, and they mature in 10 years.

-Refer to Exhibit 16.9. At present, what would be the minimum value of the bond?

(Multiple Choice)

4.8/5 (39)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The following information is provided in the context of a two-period (two six-month periods) binomial option pricing model. A stock currently trades at $60 per share, and a call option on the stock has an exercise price of $65. The stock is equally likely to rise by 15 percent or fall by 15 percent during each six-month period. The one-year risk free rate is 3 percent.

-Refer to Exhibit 16.2. Calculate the possible prices of the stock at the end of one year.

(Multiple Choice)

4.8/5 (32)

A credit default swap (CDS) is better regarded as an option-like arrangement.

(True/False)

4.8/5 (36)

The binomial option pricing model and the Black and Scholes model are similar because they are both discrete models.

(True/False)

4.8/5 (37)

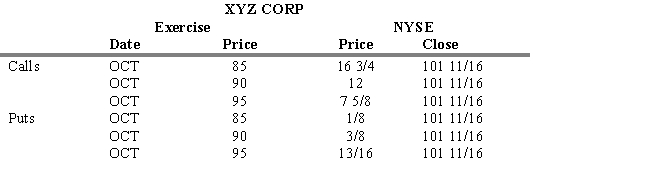

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 16.8. If you establish a long straddle using the options with an 85 exercise price, what is your dollar gain or loss if at expiration XYZ is still trading at 101 11/16?

-Refer to Exhibit 16.8. If you establish a long straddle using the options with an 85 exercise price, what is your dollar gain or loss if at expiration XYZ is still trading at 101 11/16?

(Multiple Choice)

5.0/5 (39)

In convertible bonds, the value of the common stock price upon immediate conversion is the

(Multiple Choice)

4.8/5 (28)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

GE Corporation has a put option selling for $2.90 and a call option selling for $1.95, both with a strike price of $29.00.

-Refer to Exhibit 16.6. What would the net value of a covered call position be if the stock price at expiration is $35?

(Multiple Choice)

4.9/5 (41)

The conversion parity price is equal to the par value of a convertible bond divided by the number of shares into which it can be converted.

(True/False)

4.9/5 (33)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the following information on put and call options for Citigroup

-Refer to Exhibit 16.4. Calculate the payoffs of a short straddle at a stock price at expiration of $20 and a stock price at expiration of $45.

-Refer to Exhibit 16.4. Calculate the payoffs of a short straddle at a stock price at expiration of $20 and a stock price at expiration of $45.

(Multiple Choice)

4.8/5 (30)

A money spread involves buying and selling call options in the same stock with

(Multiple Choice)

4.9/5 (33)

Which of the following is NOT a factor needed to calculate the value of an American call option?

(Multiple Choice)

4.8/5 (38)

Which of the following is not a variable required to determine an option's value in the Black-Scholes valuation model?

(Multiple Choice)

4.8/5 (30)

The Black-Scholes model assumes that stock price movements can be described by

(Multiple Choice)

4.8/5 (35)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 16.8. If you establish a long strap using the options with a 90 exercise price, what is your dollar gain or loss if at expiration XYZ is still trading at 101 11/16?

(Multiple Choice)

4.8/5 (45)

A vertical spread involves buying and selling call options in the same stock with

(Multiple Choice)

4.8/5 (30)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the following information on put and call options for Citigroup

-Refer to Exhibit 16.4. A covered call is an appropriate strategy if

(Multiple Choice)

4.8/5 (42)

A foreign currency option contract traded on U.S. exchanges allows for the sale or purchase of a set amount of

(Multiple Choice)

4.9/5 (32)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 16.8. If you establish a long strap using the options with an 85 exercise price, what is your dollar gain or loss if at expiration XYZ is still trading at 101 11/16?

(Multiple Choice)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)