Exam 16: Option Contracts

Exam 1: The Investment Setting72 Questions

Exam 1: The Investment Setting: Part A6 Questions

Exam 2: Asset Allocation and Security Selection77 Questions

Exam 2: Asset Allocation and Security Selection: Part A3 Questions

Exam 3: Organization and Functioning of Securities Markets87 Questions

Exam 4: Security Market Indexes and Index Funds89 Questions

Exam 5: Efficient Capital Markets, Behavioral Finance, and Technical Analysis162 Questions

Exam 6: An Introduction to Portfolio Management114 Questions

Exam 6: An Introduction to Portfolio Management: Part A2 Questions

Exam 6: An Introduction to Portfolio Management: Part B2 Questions

Exam 7: Asset Pricing Models152 Questions

Exam 8: Equity Valuation83 Questions

Exam 9: The Top-Down Approach to Market, Industry, and Company Analysis216 Questions

Exam 10: The Practice of Fundamental Investing60 Questions

Exam 11: Equity Portfolio Management Strategies65 Questions

Exam 12: Bond Fundamentals and Valuation138 Questions

Exam 13: Bond Analysis and Portfolio Management Strategies125 Questions

Exam 14: An Introduction to Derivative Markets and Securities102 Questions

Exam 15: Forward, Futures, and Swap Contracts148 Questions

Exam 16: Option Contracts122 Questions

Exam 17: Professional Money Management, Alternative Assets, and Industry Ethics109 Questions

Exam 18: Evaluation of Portfolio Performance111 Questions

Select questions type

Risk management is the driving force behind the futures options market.

(True/False)

4.7/5  (38)

(38)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

BioTech Industries has debentures outstanding (par value $1,000) convertible into the company's common stock at $30. The coupon rate is 11 percent payable semiannually, and they mature in 10 years.

-Refer to Exhibit 16.9. Calculate the straight-bond value assuming that bonds of equivalent risk and maturity are yielding 14 percent per year compounded semiannually.

(Multiple Choice)

4.9/5 (35)

The investment value of a convertible bond is the price that it would be expected to sell as a straight debt instrument.

(True/False)

5.0/5 (39)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

GE Corporation has a put option selling for $2.90 and a call option selling for $1.95, both with a strike price of $29.00.

-Refer to Exhibit 16.6. Which strategy is most appropriate for an investor who expects share prices to be volatile but was inclined to be bullish?

(Multiple Choice)

4.7/5 (34)

Assume that you have just sold a stock for a loss at a price of $75 for tax purposes. You still wish to maintain exposure to the sold stock. Suppose that you sell a put with a strike price of $80 and a price of $7.25. Calculate the effective price paid to repurchase the stock if the price after 35 days is $85.

(Multiple Choice)

4.8/5 (28)

The most important input the investor must provide in determining option values is the strike price.

(True/False)

4.7/5 (42)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the following information on put and call options for a common stock.

-Refer to Exhibit 16.7. Calculate the net value of a covered call position at an expiration stock price of $20.

-Refer to Exhibit 16.7. Calculate the net value of a covered call position at an expiration stock price of $20.

(Multiple Choice)

4.9/5 (29)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the following information on put and call options for Citigroup

-Refer to Exhibit 16.4. Calculate the payoffs of a long strap at a stock price at expiration of $20 and a stock price at expiration of $45.

-Refer to Exhibit 16.4. Calculate the payoffs of a long strap at a stock price at expiration of $20 and a stock price at expiration of $45.

(Multiple Choice)

4.8/5 (39)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the following information on put and call options for a common stock.

-Refer to Exhibit 16.7. Calculate the payoff of a short straddle at an expiration stock price of $20.

(Multiple Choice)

4.8/5 (32)

Stock options expire on the Sunday following the third Saturday of the designated month.

(True/False)

4.9/5 (41)

All of the following are normal characteristics of a convertible bond, EXCEPT

(Multiple Choice)

4.8/5 (39)

Risk management strategies involving interest rate agreements can be classified as forward-based or option-based.

(True/False)

4.9/5 (39)

In a binomial option pricing model, the initial value of the call can be determined by working backward through the tree and solving for each of the remaining intermediate option values.

(True/False)

4.9/5 (38)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

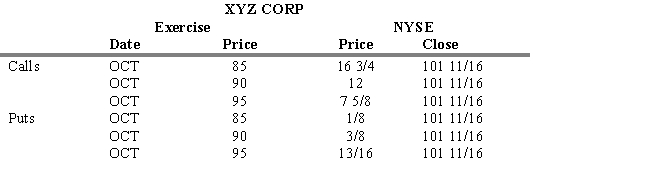

-Refer to Exhibit 16.8. If you establish a long strip using the options with an 85 exercise price, what is your dollar gain or loss if at expiration XYZ is still trading at 101 11/16?

-Refer to Exhibit 16.8. If you establish a long strip using the options with an 85 exercise price, what is your dollar gain or loss if at expiration XYZ is still trading at 101 11/16?

(Multiple Choice)

4.9/5 (32)

A currency call is like being ____ in the currency futures.

(Multiple Choice)

4.8/5 (32)

Options on futures expire at the same time the futures contract expires.

(True/False)

5.0/5 (38)

In index options, the aggregate market takes the place of the individual stock issues being traded, as in stock options.

(True/False)

5.0/5 (37)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

GE Corporation has a put option selling for $2.90 and a call option selling for $1.95, both with a strike price of $29.00.

-Refer to Exhibit 16.6. What would the net value of a long straddle position be if the stock price at expiration is $35?

(Multiple Choice)

4.8/5 (41)

Assume that you have just sold a stock for a loss at a price of $75 for tax purposes. You still wish to maintain exposure to the sold stock. Suppose that you sell a put with a strike price of $80 and a price of $7.25. Calculate the effective price paid to repurchase the stock if the price after 35 days is $70.

(Multiple Choice)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)