Exam 7: Technology, Production and Costs

Exam 1: Economics: Foundations and Models160 Questions

Exam 2: Choices and Trade-Offs in the Market192 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply202 Questions

Exam 4: Elasticity: the Responsiveness of Demand and Supply226 Questions

Exam 5: Economic Efficiency, Government Price Setting and Taxes187 Questions

Exam 6: Consumer Choice and Behavioural Economics254 Questions

Exam 7: Technology, Production and Costs300 Questions

Exam 8: Firms in Perfectly Competitive Markets270 Questions

Exam 9: Monopoly Markets281 Questions

Exam 10: Monopolistic Competition253 Questions

Exam 11: Oligopoly: Firms in Less Competitive Markets186 Questions

Exam 12: The Markets for Labour and Other Factors of Production253 Questions

Exam 13: International Trade131 Questions

Exam 14: Government Intervention in the Market122 Questions

Exam 15: Externalities, Environmental Policy and Public Goods212 Questions

Exam 16: The Distribution of Income and Social Policy121 Questions

Select questions type

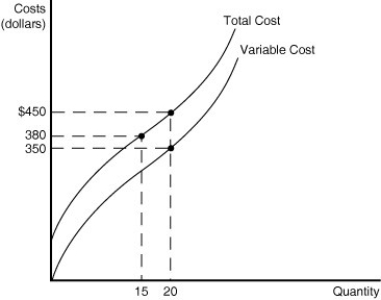

Figure 7-9  -Refer to Figure 7-9 above to solve the following problems.

a.Calculate the fixed cost of production.

b.Calculate the average total cost of production when the firm produces 20 units of output.

c.Calculate the average variable cost of production when the firm produces 20 units of output.

d.Calculate the average fixed cost of production when the firm produces 20 units of output.

e.Calculate the average fixed cost of production when the firm produces 15 units of output.

f.If the firm increases output from 15 to 20 units what is the marginal cost of output?

-Refer to Figure 7-9 above to solve the following problems.

a.Calculate the fixed cost of production.

b.Calculate the average total cost of production when the firm produces 20 units of output.

c.Calculate the average variable cost of production when the firm produces 20 units of output.

d.Calculate the average fixed cost of production when the firm produces 20 units of output.

e.Calculate the average fixed cost of production when the firm produces 15 units of output.

f.If the firm increases output from 15 to 20 units what is the marginal cost of output?

(Essay)

4.9/5  (27)

(27)

Which of the following can a firm do in the long run but not in the short run?

(Multiple Choice)

4.9/5 (31)

If marginal product is equal to average product,then total product is at a maximum.

(True/False)

4.8/5 (24)

Explain how the listed events (a-d)would affect the following at Hilton Hotels.

i.Marginal cost

ii.Average variable cost

iii.Average fixed cost

iv.Average total cost

a.Hilton decides on an across-the-board 5 per cent increase in executive salaries.

b.Hilton decides to eliminate all print advertising.

c.Hilton signs a new contract with the Culinary Workers Union that requires the company to increase wages for all its kitchen workers.

d.The federal government starts to levy a $5 room tax on all hotel rooms.

(Essay)

5.0/5 (33)

The processes a firm uses to turn inputs into outputs of goods and services is called

(Multiple Choice)

4.9/5 (36)

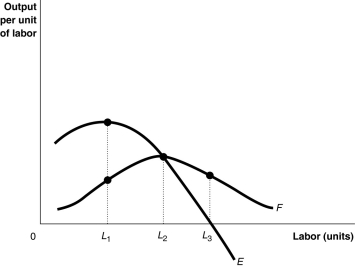

Figure 7-2  -Refer to Figure 7-2.The average product of labour declines after L2 because

-Refer to Figure 7-2.The average product of labour declines after L2 because

(Multiple Choice)

4.8/5 (35)

Which of the following describes how output changes in the short run? Because of specialisation and the division of labour,as more workers are hired

(Multiple Choice)

4.8/5 (34)

Which of the following is a reason why a firm would experience diseconomies of scale?

(Multiple Choice)

4.9/5 (31)

Which of the following costs will not change as output changes?

(Multiple Choice)

4.8/5 (39)

As the level of output increases,what happens to the value of average fixed cost,and what happens to the difference between the value of average total cost and average variable cost?

(Essay)

4.9/5 (33)

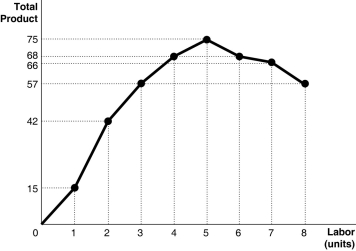

Figure 7-1  -Refer to Figure 7-1.The marginal product of the 3rd worker is

-Refer to Figure 7-1.The marginal product of the 3rd worker is

(Multiple Choice)

4.8/5 (37)

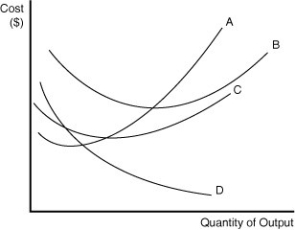

Figure 7-6  Figure 7-6 contains information about the short-run cost structure of a firm.

-Refer to Figure 7-6.In the figure above,which letter represents the marginal cost curve?

Figure 7-6 contains information about the short-run cost structure of a firm.

-Refer to Figure 7-6.In the figure above,which letter represents the marginal cost curve?

(Multiple Choice)

4.9/5 (37)

Which of the following are examples of a firm experiencing a positive technological change?

a.A firm is able to reduce its inputs by 15 per cent and still produce the same level of output.

b.A seminar attended by the firm's workers makes them more productive.

c.A firm adds 5 per cent to its workforce and is able to maintain its initial level of output.

d.A firm restructures its distribution system and is able to save on its shipping times.

e.A firm rearranges its warehouse and finds that it can use fewer workers to maintain its productivity level.

(Essay)

4.7/5 (30)

The additional output a firm produces by hiring one more worker is called the marginal product of labour.

(True/False)

4.7/5 (33)

Figure 7-1

-Refer to Figure 7-1.Diminishing marginal productivity sets in after

(Multiple Choice)

4.9/5 (41)

In economics,technology only refers to the development of new products.

(True/False)

4.7/5 (37)

A firm has successfully adopted a positive technological change when

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)