Exam 8: Firms in Perfectly Competitive Markets

Exam 1: Economics: Foundations and Models160 Questions

Exam 2: Choices and Trade-Offs in the Market192 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply202 Questions

Exam 4: Elasticity: the Responsiveness of Demand and Supply226 Questions

Exam 5: Economic Efficiency, Government Price Setting and Taxes187 Questions

Exam 6: Consumer Choice and Behavioural Economics254 Questions

Exam 7: Technology, Production and Costs300 Questions

Exam 8: Firms in Perfectly Competitive Markets270 Questions

Exam 9: Monopoly Markets281 Questions

Exam 10: Monopolistic Competition253 Questions

Exam 11: Oligopoly: Firms in Less Competitive Markets186 Questions

Exam 12: The Markets for Labour and Other Factors of Production253 Questions

Exam 13: International Trade131 Questions

Exam 14: Government Intervention in the Market122 Questions

Exam 15: Externalities, Environmental Policy and Public Goods212 Questions

Exam 16: The Distribution of Income and Social Policy121 Questions

Select questions type

A very large number of small sellers who sell identical products imply

Free

(Multiple Choice)

4.9/5  (35)

(35)

Correct Answer: Verified

Verified

C

If price = marginal cost at the output produced by a perfectly competitive firm and the firm is earning an economic profit,then

Free

(Multiple Choice)

4.8/5 (38)

Correct Answer:Verified

D

Figure 8-10  -Refer to Figure 8-10.Consider a typical firm in a perfectly competitive industry that makes short-run profits.Which of the diagrams in the figure shows the effect on the industry as it transitions to a long-run equilibrium?

-Refer to Figure 8-10.Consider a typical firm in a perfectly competitive industry that makes short-run profits.Which of the diagrams in the figure shows the effect on the industry as it transitions to a long-run equilibrium?

Free

(Multiple Choice)

4.9/5 (33)

Correct Answer:Verified

B

Which of the following describes the difference between the market demand curve for a perfectly competitive industry and the demand curve for a firm in this industry?

(Multiple Choice)

4.8/5 (32)

Suppose the equilibrium price in a perfectly competitive industry is $15 and a firm in the industry charges $21.Which of the following will happen?

(Multiple Choice)

4.8/5 (30)

Figure 8-13  -Refer to Figure 8-13.Suppose a typical firm in a perfectly competitive market is earning economic profits in the short run.Which of the diagrams in the figure depicts what happens in the industry as it transitions to a long-run equilibrium?

-Refer to Figure 8-13.Suppose a typical firm in a perfectly competitive market is earning economic profits in the short run.Which of the diagrams in the figure depicts what happens in the industry as it transitions to a long-run equilibrium?

(Multiple Choice)

4.8/5 (29)

Figure 8-14  -Refer to Figure 8-14.Which panel best represents the perfectly competitive organic produce market's transition to the long run when some firms in the market are earning economic profits?

-Refer to Figure 8-14.Which panel best represents the perfectly competitive organic produce market's transition to the long run when some firms in the market are earning economic profits?

(Multiple Choice)

4.7/5 (34)

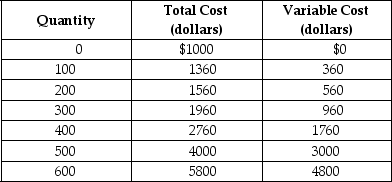

Table 8-1

Table 8-1 shows the short-run cost data of a perfectly competitive firm that produces plastic camera cases.Assume that output can only be increased in batches of 100 units.

-Refer to Table 8-1.The firm will not produce in the short run if the output price falls below

Table 8-1 shows the short-run cost data of a perfectly competitive firm that produces plastic camera cases.Assume that output can only be increased in batches of 100 units.

-Refer to Table 8-1.The firm will not produce in the short run if the output price falls below

(Multiple Choice)

4.9/5 (32)

Maximising average profit is equivalent to maximising total profit.

(True/False)

4.9/5 (41)

Firms in perfectly competitive industries are unable to control the prices of the products they sell and earn a profit in the long run.Which of the following is one reason for this?

(Multiple Choice)

4.9/5 (32)

In an increasing-cost industry,the long-run supply curve is upward sloping.

(True/False)

4.8/5 (30)

For a perfectly competitive firm,at the profit-maximising output,average revenue equals marginal cost.

(True/False)

4.8/5 (41)

If the market price is $25,the average revenue of selling five units is

(Multiple Choice)

4.7/5 (36)

Using two graphs,illustrate how a positive technological change in the market for notebook computers could eliminate short-run economic profit for a firm in that market.On the first graph,use a supply and demand graph to illustrate the positive technological change.On the second graph,use demand,ATC,MC and MR curves to illustrate the elimination of economic profit resulting from the positive technological change.Explain what is taking place in each graph.

(Essay)

4.8/5 (33)

A perfectly competitive firm in long-run equilibrium produces output at the lowest possible average total cost.

(True/False)

4.9/5 (29)

The short-run supply curve for a perfectly competitive firm is that part of the firm's marginal cost curve that lies above the minimum point of its average variable cost curve.

(True/False)

4.9/5 (34)

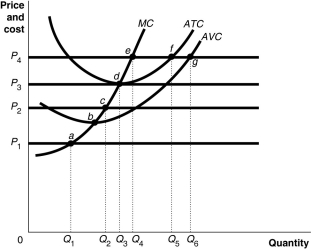

Figure 8-7  Figure 8-7 shows cost and demand curves facing a profit-maximising,perfectly competitive firm.

-Refer to Figure 8-7.At price P2,the firm would produce

Figure 8-7 shows cost and demand curves facing a profit-maximising,perfectly competitive firm.

-Refer to Figure 8-7.At price P2,the firm would produce

(Multiple Choice)

4.9/5 (35)

Assume that the tuna fishing industry is perfectly competitive.Which of the following best characterises the industry if,as demand for tuna increases,fishing boats have to go farther into the ocean to harvest tuna?

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)