Exam 11: Return and Risk: the Capital Asset Pricing Model

Exam 1: Introduction to Corporate Finance61 Questions

Exam 2: Financial Statements and Cash Flow92 Questions

Exam 3: Financial Statements Analysis and Long-Term Planning117 Questions

Exam 5: Net Present Value and Other Investment Rules92 Questions

Exam 8: Interest Rates and Bond Valuation67 Questions

Exam 10: Risk and Return: Lessons From Market History81 Questions

Exam 11: Return and Risk: the Capital Asset Pricing Model125 Questions

Exam 12: An Alternative View of Risk and Return: the Arbitrage Pricing Theory45 Questions

Exam 14: Efficient Capital Markets and Behavioral Challenges50 Questions

Exam 15: Long-Term Financing: an Introduction43 Questions

Exam 20: Raising Capital65 Questions

Exam 22: Options and Corporate Finance93 Questions

Exam 23: Options and Corporate Finance: Extensions and Applications42 Questions

Exam 24: Warrants and Convertibles52 Questions

Exam 25: Derivatives and Hedging Risk56 Questions

Exam 31: International Corporate Finance93 Questions

Select questions type

When computing the expected return on a portfolio of stocks the portfolio weights are based on the:

(Multiple Choice)

4.9/5  (33)

(33)

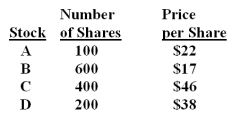

You own the following portfolio of stocks.What is the portfolio weight of stock C?

(Multiple Choice)

4.8/5 (33)

Which one of the following is an example of unsystematic risk?

(Multiple Choice)

4.9/5 (40)

The majority of the benefits from portfolio diversification can generally be achieved with just _____ diverse securities.

(Multiple Choice)

4.9/5 (35)

The excess return earned by an asset that has a beta of 1.0 over that earned by a risk-free asset is referred to as the:

(Multiple Choice)

4.9/5 (39)

The elements in the off-diagonal positions of the variance/covariance matrix are:

(Multiple Choice)

4.8/5 (39)

What is the portfolio variance if 30% is invested in stock S and 70% is invested in stock T?

(Multiple Choice)

4.8/5 (50)

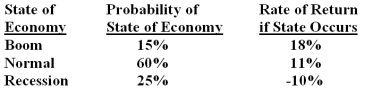

The Rotor Co.stock is expected to earn 16% in a recession,7% in a normal economy,and lose 3% in a booming economy.The probability of a boom is 20% while the probability of a normal economy is 55% and the chance of a recession is 25%.What is the expected rate of return on this stock?

(Multiple Choice)

4.8/5 (36)

What is the expected return on a portfolio which is invested 20% in stock A,50% in stock B,and 30% in stock C?

(Multiple Choice)

4.8/5 (41)

The stock of Martin Industries has a beta of 1.43.The risk-free rate of return is 3.6% and the market risk premium is 9%.What is the expected rate of return on Martin Industries stock?

(Multiple Choice)

4.8/5 (30)

You would like to combine a risky stock with a beta of 1.8 with U.S.Treasury bills in such a way that the risk level of the portfolio is equivalent to the risk level of the overall market.What percentage of the portfolio should be invested in Treasury bills?

(Multiple Choice)

4.9/5 (41)

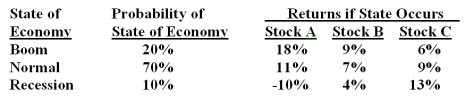

You own a portfolio with the following expected returns given the various states of the economy.What is the overall portfolio expected return?

(Multiple Choice)

4.9/5 (38)

The combination of the efficient set of portfolios with a riskless lending and borrowing rate results in:

(Multiple Choice)

4.8/5 (39)

The relationship between the covariance of the security with the market to the variance is called the:

(Multiple Choice)

4.8/5 (42)

The percentage of a portfolio's total value invested in a particular asset is called that asset's:

(Multiple Choice)

4.9/5 (36)

The amount of systematic risk present in a particular risky asset,relative to the systematic risk present in an average risky asset,is called the particular asset's:

(Multiple Choice)

4.9/5 (45)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)