Exam 11: Return and Risk: the Capital Asset Pricing Model

Exam 1: Introduction to Corporate Finance61 Questions

Exam 2: Financial Statements and Cash Flow92 Questions

Exam 3: Financial Statements Analysis and Long-Term Planning117 Questions

Exam 5: Net Present Value and Other Investment Rules92 Questions

Exam 8: Interest Rates and Bond Valuation67 Questions

Exam 10: Risk and Return: Lessons From Market History81 Questions

Exam 11: Return and Risk: the Capital Asset Pricing Model125 Questions

Exam 12: An Alternative View of Risk and Return: the Arbitrage Pricing Theory45 Questions

Exam 14: Efficient Capital Markets and Behavioral Challenges50 Questions

Exam 15: Long-Term Financing: an Introduction43 Questions

Exam 20: Raising Capital65 Questions

Exam 22: Options and Corporate Finance93 Questions

Exam 23: Options and Corporate Finance: Extensions and Applications42 Questions

Exam 24: Warrants and Convertibles52 Questions

Exam 25: Derivatives and Hedging Risk56 Questions

Exam 31: International Corporate Finance93 Questions

Select questions type

For a highly diversified equally weighted portfolio with a large number of securities,the portfolio variance is:

(Multiple Choice)

4.9/5  (33)

(33)

Which one of the following measures is relevant to the systematic risk principle?

(Multiple Choice)

4.8/5 (38)

If the correlation between two stocks is +1,then a portfolio combining these two stocks will have a variance that is:

(Multiple Choice)

4.7/5 (29)

What is the standard deviation of a portfolio that is invested 40% in stock Q and 60% in stock R?

(Multiple Choice)

5.0/5 (40)

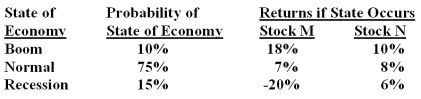

What is the expected return on a portfolio comprised of $4,000 in stock M and $6,000 in stock N if the economy enjoys a boom period?

(Multiple Choice)

4.8/5 (32)

The diagram below represents an opportunity set for a two asset combination.Indicate the correct efficient set with labels;explain why it is so.

(Essay)

4.8/5 (40)

Which one of the following is an example of systematic risk?

(Multiple Choice)

4.8/5 (34)

Draw the SML and plot asset C such that it has less risk than the market but plots above the

SML,and asset D such that it has more risk than the market and plots below the SML.(Be sure to indicate where the market portfolio is on your graph. )Explain how assets like C or D can plot as they do and explain why such pricing cannot persist in a market that is in equilibrium.

(Essay)

4.8/5 (42)

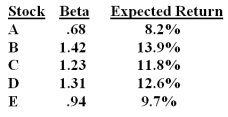

Which one of the following stocks is correctly priced if the risk-free rate of return is 2.5% and the market risk premium is 8%?

(Multiple Choice)

4.8/5 (33)

You have plotted the data for two securities over time on the same graph,i.e. ,the monthly return of each security for the last 5 years.If the pattern of the movements of each of the two securities rose and fell as the other did,these two securities would have:

(Multiple Choice)

4.8/5 (31)

If the economy booms,RTF,Inc.stock is expected to return 10%.If the economy goes into a recessionary period,then RTF is expected to only return 4%.The probability of a boom is 60% while the probability of a recession is 40%.What is the variance of the returns on RTF,Inc.stock?

(Multiple Choice)

5.0/5 (40)

The Rotor Co.stock is expected to earn 14% in a recession,6% in a normal economy,and lose 4% in a booming economy.The probability of a boom is 20% while the probability of a normal economy is 55% and the chance of a recession is 25%.What is the expected rate of return on this stock?

(Multiple Choice)

4.9/5 (43)

The common stock of Chai Tea Inc has an expected return of 14.4%.The return on the market is 10% and the risk-free rate of return is 3.5%.What is the beta of this stock?

(Multiple Choice)

4.9/5 (35)

A portfolio is entirely invested into Buzz's Bauxite Boring equity,which is expected to return 16%,and Zum's Inc.bonds,which are expected to return 8%.60% of the funds are invested in Buzz's and the rest in Zum's.What is the expected return on the portfolio?

(Multiple Choice)

4.8/5 (40)

Risk that affects at most a small number of assets is called _____ risk.

(Multiple Choice)

4.9/5 (38)

A security that is fairly priced will have a return _____ the Security Market Line.

(Multiple Choice)

4.8/5 (38)

The expected return on a stock that is computed using economic probabilities is:

(Multiple Choice)

4.8/5 (39)

The Capital Market Line is the pricing relationship between:

(Multiple Choice)

4.8/5 (43)

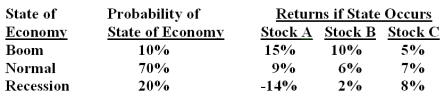

What is the standard deviation of a portfolio which is invested 20% in stock A,30% in stock B and 50% in stock C?

(Multiple Choice)

4.8/5 (35)

The variance of Stock A is .004,the variance of the market is .007 and the covariance between the two is .0026.What is the correlation coefficient?

(Multiple Choice)

4.7/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)