Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting

Exam 1: Economics: Foundations and Models233 Questions

Exam 2: Trade-Offs, comparative Advantage, and the Market System259 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply242 Questions

Exam 4: Economic Efficiency, government Price Setting, and Taxes208 Questions

Exam 5: Externalities, environmental Policy, and Public Goods267 Questions

Exam 6: Elasticity: The Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care169 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance278 Questions

Exam 9: Comparative Advantage and the Gains From International Trade189 Questions

Exam 10: Consumer Choice and Behavioral Economics302 Questions

Exam 11: Technology, production, and Costs330 Questions

Exam 12: Firms in Perfectly Competitive Markets298 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting278 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets262 Questions

Exam 15: Monopoly and Antitrust Policy271 Questions

Exam 16: Pricing Strategy263 Questions

Exam 17: The Markets for Labor and Other Factors of Production286 Questions

Exam 18: Public Choice,taxes,and the Distribution of Income258 Questions

Select questions type

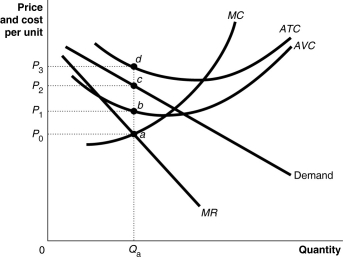

Figure 13-4  Figure 13-4 shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 13-4.What is the area that represents the total fixed cost of production?

Figure 13-4 shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 13-4.What is the area that represents the total fixed cost of production?

Free

(Multiple Choice)

4.9/5  (36)

(36)

Correct Answer: Verified

Verified

C

If a firm has excess capacity,it means

Free

(Multiple Choice)

4.8/5 (32)

Correct Answer:Verified

B

A monopolistically competitive industry that earns economic profits in the short run will

Free

(Multiple Choice)

4.9/5 (42)

Correct Answer:Verified

B

If buyers of a monopolistically competitive product feel the products of different sellers are strongly differentiated,then the demand for each seller's product is

(Multiple Choice)

4.9/5 (29)

Which of the following is not a characteristic of monopolistic competition?

(Multiple Choice)

4.9/5 (43)

When a monopolistically competitive firm lowers it price one bad thing happens to the firm.What is this "one bad thing" called?

(Multiple Choice)

4.8/5 (31)

Every firm that has the ability to affect the price of the good or service it sells will

(Multiple Choice)

4.9/5 (35)

Draw a graph that shows the impact on a firm's profit when it increases spending on advertising and the increased advertising has no effect on the demand for a firm's product.

(Essay)

5.0/5 (34)

In the long-run equilibrium,a monopolistically competitive firm earning normal profit produces the allocatively efficient output level.

(True/False)

4.8/5 (31)

Which of the following describes the relative positions of the demand curve and the average total cost (ATC)curve of a monopolistically competitive firm that earns a profit in the short run?

(Multiple Choice)

4.8/5 (34)

If a monopolistically competitive firm is producing 50 units of output where marginal cost equals marginal revenue,total cost is $1,674 and total revenue is $2,000,its average profit is

(Multiple Choice)

4.9/5 (30)

Unlike a perfectly competitive firm,a monopolistic competitor does not have a short-run shut-down point.

(True/False)

4.9/5 (34)

Suppose that if a local McDonald's restaurant reduces the price of a Big Mac from $4.00 to $3.25,the number of Big Macs it sells per day will increase from 4 to 5.Explain the output effect and the price effect resulting from this change.Using a graph,illustrate both the loss in revenue from selling each of the first 4 Big Macs for $0.75 less and the additional revenue from selling 1 more Big Mac.What is the total change in revenue received which results from this price decrease?

(Essay)

4.8/5 (32)

Long-run equilibrium in a monopolistically competitive market is similar to long-run equilibrium in a perfectly competitive market in that in both markets,firms

(Multiple Choice)

4.8/5 (28)

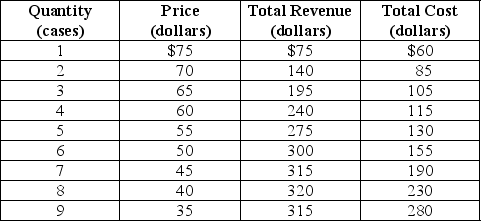

Table 13-2

Eco Energy is a monopolistically competitive producer of a sports beverage called Power On. Table 13-2 shows the firm's demand and cost schedules.

-Refer to Table 13-2.What is the output (Q)that maximizes profit and what is the price (P)charged?

Eco Energy is a monopolistically competitive producer of a sports beverage called Power On. Table 13-2 shows the firm's demand and cost schedules.

-Refer to Table 13-2.What is the output (Q)that maximizes profit and what is the price (P)charged?

(Multiple Choice)

4.8/5 (38)

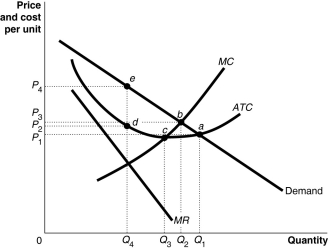

Figure 13-13  -Refer to Figure 13-13.If the diagram represents a typical firm in the market,what is likely to happen in the long run?

-Refer to Figure 13-13.If the diagram represents a typical firm in the market,what is likely to happen in the long run?

(Multiple Choice)

4.8/5 (47)

One of the assumptions of monopolistic competition is that firms produce differentiated products.What does this assumption imply about the demand curve facing a representative firm?

(Essay)

4.9/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)