Exam 1: Introduction to Business Combinations and the Conceptual Framework

Exam 1: Introduction to Business Combinations and the Conceptual Framework35 Questions

Exam 2: Accounting for Business Combinations42 Questions

Exam 3: Consolidated Financial Statements Date of Acquisition37 Questions

Exam 4: Consolidated Financial Statements After Acquisition42 Questions

Exam 5: Allocation and Depreciation of Differences Between Implied and Book Values36 Questions

Exam 6: Elimination of Unrealized Profit on Intercompany Sales of Inventory35 Questions

Exam 7: Elimination of Unrealized Gains or Losses on Intercompany Sales of Property and Equipment33 Questions

Exam 8: Changes in Ownership Interest32 Questions

Exam 9: Intercompany Bond Holdings and Miscellaneous Topics Consolidated Financial Statements33 Questions

Exam 10: Insolvency Liquidation and Reorganization35 Questions

Exam 11: International Financial Reporting Standards28 Questions

Exam 12: Accounting for Foreign Currency Transactions and Hedging Foreign Exchange Risk35 Questions

Exam 13: Translation of Financial Statements of Foreign Affiliates29 Questions

Exam 14: Reporting for Segments and for Interim Financial Periods44 Questions

Exam 15: Partnerships: Formation, operation and Ownership Changes39 Questions

Exam 16: Partnership Liquidation35 Questions

Exam 17: Introduction to Fund Accounting29 Questions

Exam 18: Introduction to Accounting for State and Local Governmental Units34 Questions

Exam 19: Accounting for Nongovernment Nonbusiness Organizations: Colleges and Universities, hospitals, and Other Health Care Organizations38 Questions

Select questions type

The excess of the amount offered in an acquisition over the prior stock price of the acquired firm is the:

(Multiple Choice)

4.7/5  (37)

(37)

The view that consolidated financial statements represent those of a single economic entity with several classes of stockholder interest is consistent with the:

(Multiple Choice)

4.9/5 (35)

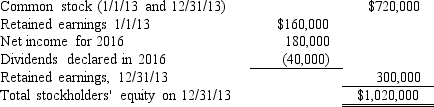

The following balances were taken from the records of S Company:

P Company purchased 75% of S Company's common stock on January 1,2014 for $900,000.The difference between implied value and book value is attributable to assets with a remaining useful life on January 1,2016 of ten years.

Required:

A.Compute the difference between cost/(implied)and book value applying:

1.Parent company theory.

2.Economic unit theory.

B.Assuming the economic unit theory:

1.Compute noncontrolling interest in consolidated income for 2016.

2.Compute noncontrolling interest in net assets on December 31,2016.

P Company purchased 75% of S Company's common stock on January 1,2014 for $900,000.The difference between implied value and book value is attributable to assets with a remaining useful life on January 1,2016 of ten years.

Required:

A.Compute the difference between cost/(implied)and book value applying:

1.Parent company theory.

2.Economic unit theory.

B.Assuming the economic unit theory:

1.Compute noncontrolling interest in consolidated income for 2016.

2.Compute noncontrolling interest in net assets on December 31,2016.

(Essay)

4.8/5 (36)

The view that only the parent company's share of the unrealized intercompany profit recognized by the selling affiliate that remains in assets should be eliminated in the preparation of consolidated financial statements is consistent with the:

(Multiple Choice)

4.8/5 (44)

The defense tactic that involves purchasing shares held by the would-be acquiring company at a price substantially in excess of their fair value is called:

(Multiple Choice)

4.9/5 (30)

Under the parent company concept,consolidated net income __________ the consolidated net income under the economic unit concept.

(Multiple Choice)

4.9/5 (40)

The two alternative views of consolidated financial statements are the parent company concept and the economic entity concept.Briefly explain the differences between the concepts.

(Essay)

4.8/5 (38)

Estimating the value of goodwill to be included in an offering price can be done under several alternative methods.The excess earnings approach is frequently used.Identify the steps used in this approach to estimate goodwill.

(Essay)

4.8/5 (29)

The impairment standard as it relates to goodwill is an example of a:

(Multiple Choice)

4.9/5 (35)

The third period of business combinations started after World War II and is called:

(Multiple Choice)

4.9/5 (40)

Which of the following situations best describes a business combination to be accounted for as a statutory merger?

(Multiple Choice)

4.9/5 (35)

Which of the following is not a component of other comprehensive income under GAAP?

(Multiple Choice)

4.9/5 (29)

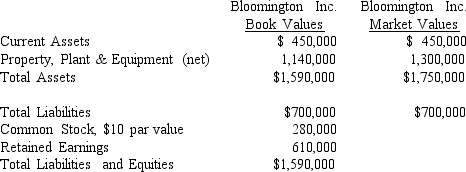

Eden Company is trying to decide whether to acquire Bloomington Inc.The following balance sheet for Bloomington Inc.provides information about book values.Estimated market values are also listed,based upon Eden Company's appraisals.

Eden Company expects that Bloomington will earn approximately $290,000 per year in net income over the next five years.This income is higher than the 14% annual return on tangible assets considered to be the industry "norm."

Required:

A.Compute an estimation of goodwill based on the information above that Eden might be willing to pay (include in its purchase price),under each of the following additional assumptions:

(1)Eden is willing to pay for excess earnings for an expected life of 4 years (undiscounted).

(2)Eden is willing to pay for excess earnings for an expected life of 4 years,which should be

capitalized at the industry normal rate of return.

(3)Excess earnings are expected to last indefinitely,but Eden demands a higher rate of return of

20% because of the risk involved.

B.Determine the amount of goodwill to be recorded on the books if Eden pays $1,300,000 cash and assumes Bloomington's liabilities.

Eden Company expects that Bloomington will earn approximately $290,000 per year in net income over the next five years.This income is higher than the 14% annual return on tangible assets considered to be the industry "norm."

Required:

A.Compute an estimation of goodwill based on the information above that Eden might be willing to pay (include in its purchase price),under each of the following additional assumptions:

(1)Eden is willing to pay for excess earnings for an expected life of 4 years (undiscounted).

(2)Eden is willing to pay for excess earnings for an expected life of 4 years,which should be

capitalized at the industry normal rate of return.

(3)Excess earnings are expected to last indefinitely,but Eden demands a higher rate of return of

20% because of the risk involved.

B.Determine the amount of goodwill to be recorded on the books if Eden pays $1,300,000 cash and assumes Bloomington's liabilities.

(Essay)

4.9/5 (38)

When following the parent company concept in the preparation of consolidated financial statements,noncontrolling interest in combined income is considered a(n):

(Multiple Choice)

4.8/5 (44)

Stock given as consideration for a business combination is valued at:

(Multiple Choice)

4.8/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)