Exam 9: Long-Run Costs and Output Decisions

Exam 1: The Scope and Method of Economics120 Questions

Exam 2: The Economic Problem: Scarcity and Choice110 Questions

Exam 3: Demand, Supply, and Market Equilibrium144 Questions

Exam 4: Demand and Supply Applications86 Questions

Exam 5: Elasticity86 Questions

Exam 6: Household Behavior and Consumer Choice137 Questions

Exam 7: The Production Process: the Behavior of Profit-Maximizing Firms144 Questions

Exam 8: Short-Run Costs and Output Decisions196 Questions

Exam 9: Long-Run Costs and Output Decisions187 Questions

Exam 10: Input Demand: the Labor and Land Markets123 Questions

Exam 11: Input Demand: the Capital Market and the Investment Decision116 Questions

Exam 12: General Equilibrium and the Efficiency of Perfect Competition99 Questions

Exam 13: Monopoly and Antitrust Policy200 Questions

Exam 14: Oligopoly110 Questions

Exam 15: Monopolistic Competition118 Questions

Exam 16: Externalities, Public Goods, and Social Choice170 Questions

Exam 17: Uncertainty and Asymmetric Information66 Questions

Exam 18: Income Distribution and Poverty143 Questions

Exam 19: Public Finance: The Economics of Taxation136 Questions

Exam 20: International Trade, Comparative Advantage, and Protectionism151 Questions

Exam 21: Economic Growth in Developing and Transitional Economies105 Questions

Select questions type

The Supply Room, a mail-order school supply store, grew rapidly. As a result of achieving a much larger size, the Supply Room is able to realize (1) volume discounts when buying from its suppliers, and (2) lower transportation costs by shipping in bulk. The best explanation of this is that the Supply Room seems to be experiencing

(Multiple Choice)

4.8/5  (28)

(28)

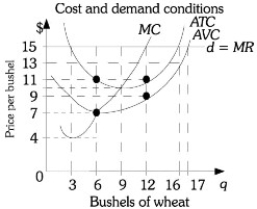

Refer to the information provided in Figure 9.1 below to answer the questions that follow.  Figure 9.1

-Refer to Figure 9.1. If this farmer is maximizing profits, his total costs will be

Figure 9.1

-Refer to Figure 9.1. If this farmer is maximizing profits, his total costs will be

(Multiple Choice)

4.8/5 (46)

Refer to the information provided in Figure 9.1 below to answer the questions that follow. Figure 9.1

-Refer to Figure 9.1. This farmer would be breaking even if price was

(Multiple Choice)

4.8/5 (38)

Assume a perfectly competitive industry is in long-run equilibrium at a price of $20. If this industry is a constant-cost industry and the demand for the product decreases, long-run equilibrium will be reestablished at a price

(Multiple Choice)

4.8/5 (33)

Refer to the information provided in Figure 9.1 below to answer the questions that follow. Figure 9.1

-Refer to Figure 9.1. If this farmer is maximizing profits, his total revenue will be

(Multiple Choice)

4.8/5 (43)

The long run industry supply curve is made up of the zero-profit equilibrium levels of output as the industry expands due to entry of new firms.

(True/False)

4.9/5 (27)

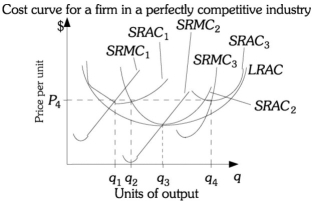

Refer to the information provided in Figure 9.5 below to answer the questions that follow.  Figure 9.5

-Refer to Figure 9.5. Assume this firm is in a constant-cost industry. For this firm to be in long-run equilibrium, the firm must be producing

Figure 9.5

-Refer to Figure 9.5. Assume this firm is in a constant-cost industry. For this firm to be in long-run equilibrium, the firm must be producing

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)