Exam 9: Long-Run Costs and Output Decisions

Exam 1: The Scope and Method of Economics120 Questions

Exam 2: The Economic Problem: Scarcity and Choice110 Questions

Exam 3: Demand, Supply, and Market Equilibrium144 Questions

Exam 4: Demand and Supply Applications86 Questions

Exam 5: Elasticity86 Questions

Exam 6: Household Behavior and Consumer Choice137 Questions

Exam 7: The Production Process: the Behavior of Profit-Maximizing Firms144 Questions

Exam 8: Short-Run Costs and Output Decisions196 Questions

Exam 9: Long-Run Costs and Output Decisions187 Questions

Exam 10: Input Demand: the Labor and Land Markets123 Questions

Exam 11: Input Demand: the Capital Market and the Investment Decision116 Questions

Exam 12: General Equilibrium and the Efficiency of Perfect Competition99 Questions

Exam 13: Monopoly and Antitrust Policy200 Questions

Exam 14: Oligopoly110 Questions

Exam 15: Monopolistic Competition118 Questions

Exam 16: Externalities, Public Goods, and Social Choice170 Questions

Exam 17: Uncertainty and Asymmetric Information66 Questions

Exam 18: Income Distribution and Poverty143 Questions

Exam 19: Public Finance: The Economics of Taxation136 Questions

Exam 20: International Trade, Comparative Advantage, and Protectionism151 Questions

Exam 21: Economic Growth in Developing and Transitional Economies105 Questions

Select questions type

An industry is in ________ if firms have an incentive to enter or exit in the ________ run.

(Multiple Choice)

4.8/5  (36)

(36)

Related to the Economics in Practice on page 198. The process of producing solar panels is subject to economies of scale, which means that as the use of solar panels ________, the long-run cost to produce them will likely ________.

(Multiple Choice)

4.9/5 (38)

Assume firms break even in an industry. New firms ________ attracted to the industry and current ones ________ exiting it.

(Multiple Choice)

4.8/5 (39)

In the long run firms will expand as long as there are more ________, and new firms will enter the industry as long as they earn ________.

(Multiple Choice)

4.8/5 (37)

The Taste Freeze Ice Cream Company is a perfectly competitive firm producing where MR = MC. The current market price of an ice cream sandwich is $5.00. Taste Freeze sells 200 ice cream sandwiches. Its AVC is $8.00 and its AFC is $3.00. What should Taste Freeze do?

(Multiple Choice)

4.8/5 (27)

A firm suffering economic losses decides whether or not to produce in the short run on the basis of whether

(Multiple Choice)

4.9/5 (39)

Refer to the data provided in Table 9.1 below to answer the questions that follow.

Table 9.1 q TFC TVC TC MC AVC ATC 0 \ 50 \ 0 \ 50 -- -- -- 1 50 20 70 20 20 70 2 50 30 80 10 15 40 3 50 45 95 15 15 31.67 4 50 62 112 17 15.50 28 5 50 90 140 28 18 28 6 50 132 182 42 22 30.33 7 50 186 236 54 26.57 33.71

-Refer to Table 9.1. If the market price is $42, then in the long run the firm will

(Multiple Choice)

4.8/5 (28)

If TR > TVC but TR < TC, a firm would ________ in the short run and ________ in the long run.

(Multiple Choice)

4.7/5 (34)

Refer to Scenario 9.2 below to answer the questions that follow.

SCENARIO 9.2: Tom borrowed $40,000 from his parents to open a donut stand. He agrees to pay his parents a 5% yearly return on the money they lent him. His other yearly fixed costs equal $10,000. His variable costs equal $25,000. He sold 40,000 dozen donuts during the year at a price of $2.00 per dozen.

-Refer to Scenario 9.2. Tom's total fixed costs equal

(Multiple Choice)

4.7/5 (29)

In the short run, firms earning a profit will want to ________ their profits while firms suffering losses will want to ________ their losses.

(Multiple Choice)

4.7/5 (33)

The marginal cost curve of a firm above AVC is also its short-run supply curve.

(True/False)

4.8/5 (34)

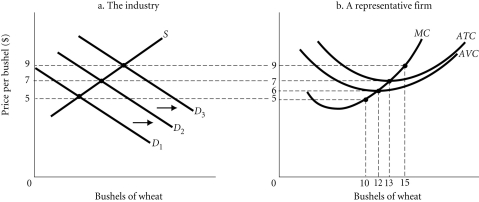

Refer to the information provided in Figure 9.7 below to answer the questions that follow.  Figure 9.7

-Refer to Figure 9.7. If demand for wheat is D1, then a profit maximizing firm will produce ________ units and earn ________.

Figure 9.7

-Refer to Figure 9.7. If demand for wheat is D1, then a profit maximizing firm will produce ________ units and earn ________.

(Multiple Choice)

4.8/5 (33)

Input prices fall as entry occurs in an decreasing-cost industry.

(True/False)

4.8/5 (39)

Related to the Economics in Practice on page 204: The auto industry exhibits large economies of scale due in part to the large capital investment of the assembly lines. During the recession of 2008-2009, the auto industry ________, and the per-unit costs of producing cars ________.

(Multiple Choice)

4.8/5 (31)

The short-run industry supply curve for a perfectly competitive industry is the

(Multiple Choice)

4.8/5 (45)

Assume a perfectly competitive industry is in long-run equilibrium at a price of $30. If this industry is an increasing-cost industry and the demand for the product increases, long-run equilibrium will be reestablished at a price

(Multiple Choice)

4.9/5 (28)

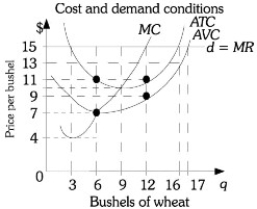

Refer to the information provided in Figure 9.1 below to answer the questions that follow.  Figure 9.1

-Refer to Figure 9.1. This farmer would earn a zero economic profit if price was

Figure 9.1

-Refer to Figure 9.1. This farmer would earn a zero economic profit if price was

(Multiple Choice)

4.9/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)