Exam 13: Current Liabilities and Contingencies

Exam 1: Environment and Theoretical Structure of Financial Accounting135 Questions

Exam 2: Review of the Accounting Process126 Questions

Exam 3: The Balance Sheet and Financial Disclosures102 Questions

Exam 4: The Income Statement, Comprehensive Income, and the Statement of Cash Flows103 Questions

Exam 5: Income Measurement and Profitability Analysis210 Questions

Exam 6: Time Value of Money Concepts114 Questions

Exam 7: Cash and Receivables164 Questions

Exam 8: Inventories: Measurement126 Questions

Exam 9: Property, Plant, and Equipment and Intangible Assets: Acquisition and Disposition120 Questions

Exam 10: Property, Plant, and Equipment and Intangible Assets: Acquisition and Disposition128 Questions

Exam 11: Property, Plant, and Equipment and Intangible Assets: Utilization and Impairment146 Questions

Exam 12: Investments186 Questions

Exam 13: Current Liabilities and Contingencies153 Questions

Exam 14: Bonds and Long-Term Notes167 Questions

Exam 15: Leases160 Questions

Exam 16: Accounting for Income Taxes145 Questions

Exam 17: Pensions and Other Postretirement Benefits197 Questions

Exam 18: Shareholders Equity Key213 Questions

Exam 19: Share-Based Compensation and Earnings Per Share178 Questions

Exam 20: Accounting Changes and Error Corrections119 Questions

Exam 21: The Statement of Cash Flows Revisited155 Questions

Select questions type

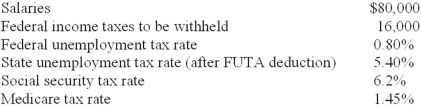

Barbara Muller Services (BMS) pays its employees monthly. The payroll information listed below is for January 2013, the first month of BMS's fiscal year.  The journal entry to record payroll for the January 2013 pay period will include a debit to payroll tax expense of:

The journal entry to record payroll for the January 2013 pay period will include a debit to payroll tax expense of:

(Multiple Choice)

4.9/5  (35)

(35)

During the year, L&M Leather Goods sold 1,000,000 reversible belts under a new sales promotional program. Each belt carried one coupon, which entitles the customer to a $4.00 cash rebate. L&M estimates that 70% of the coupons will be redeemed, even though only 500,000 coupons had been processed during the year. At December 31, L&M should report a liability for unredeemed coupons of:

(Multiple Choice)

5.0/5 (37)

The following selected transactions relate to liabilities of Chicago Glass Corporation for 2013. Chicago's fiscal year ends on December 31.

1. On January 15, Chicago received $7,000 from Henry Construction toward the purchase of $66,000 of plate glass to be delivered on February 6.

2. On February 3, Chicago received $6,700 of refundable deposits relating to containers used to transport glass components.

3. On February 6, Chicago delivered the plate glass to Henry Construction and received the balance of the purchase price.

4. First quarter credit sales totaled $700,000. The state sales tax rate is 4% and the local sales tax rate is 2%.

Required:

Prepare journal entries for the above transactions.

(Essay)

4.9/5 (42)

M Corp. has an employee benefit plan for compensated absences that gives each employee 15 paid vacation days. Vacation days can be carried over indefinitely. Employees can elect to receive payment in lieu of vacation days. At December 31, 2013, M's unadjusted balance of liability for compensated absences was $30,000. M estimated that there were 200 total vacation days available at December 31, 2013. M's employees earn an average of $150 per day. In its December 31, 2013, balance sheet, what amount of liability for compensated absences is M required to report?

(Multiple Choice)

4.8/5 (38)

A customer of RoughEdge Sharpeners alleges that RoughEdge's new razor sharpener had a defect that resulted in serious injury to the customer. RoughEdge believes the customer has a 51% chance of winning the case, and that if the customer wins the case, there is a range of losses of between $1,000,000 and $3,000,000 in which any number is equally likely to occur. Under U.S. GAAP, RoughEdge should accrue a liability in the amount of:

(Multiple Choice)

4.8/5 (37)

Yummy Rice Cereal offers an all-star bowl in exchange for three return box tops. Yummy Rice estimates that 30% will be redeemed. The bowls cost Yummy Rice $1 each. In 2013, 5,000,000 boxes of cereal were sold. By year-end 900,000 box tops had been redeemed.

Required:

Calculate the liability that Yummy Rice should report at December 31, 2013.

(Essay)

4.8/5 (39)

Branch Company, a building materials supplier, has $18,000,000 of notes payable due April 12, 2014. At December 31, 2013, Branch signed an agreement with First Bank to borrow up to $18,000,000 to refinance the notes on a long-term basis. The agreement specified that borrowings would not exceed 75% of the value of the collateral that Branch provided. At the date of issue of the December 31, 2013, financial statements, the value of Branch's collateral was $20,000,000. On its December 31, 2013, balance sheet, Branch should classify the notes as follows:

(Multiple Choice)

4.9/5 (43)

A loss contingency should be accrued in a company's financial statements only if the likelihood that a liability has been incurred is:

(Multiple Choice)

4.8/5 (37)

What is the effective interest rate (rounded) on a 3-month, noninterest-bearing note with a stated rate of 12% and a maturity value of $200,000?

(Multiple Choice)

4.9/5 (25)

Oklahoma Oil Corp. paid interest of $785,000 during 2013, and the interest payable account decreased by $125,000. What was interest expense for the year?

(Multiple Choice)

4.9/5 (39)

What was General's coupon liability as of December 31, 2013?

(Multiple Choice)

4.8/5 (33)

On October 31, 2013, Simeon Builders borrowed $16 million cash and issued a 7-month, noninterest-bearing note. The loan was made by Star Finance Co. The stated discount rate is 8%. Sky's effective interest rate on this loan is:

(Multiple Choice)

4.7/5 (29)

Ontario Resources, a natural energy supplier, borrowed $80 million cash on November 1, 2013, to fund a geological survey. The loan was made by Quebec Banque under a short-term credit line. Ontario Resources issued a 9-month, 12% promissory note with interest payable at maturity. Ontario Resources' fiscal period is the calendar year.

Required:

1. Prepare the journal entry for the issuance of the note by Ontario Resources.

2. Prepare the appropriate adjusting entry for the note by Ontario Resources on December 31, 2013. Show calculations.

3. Prepare the journal entry for the payment of the note at maturity. Show calculations.

(Essay)

4.8/5 (42)

On November 1, 2013, Ziegler Products issued a $200,000, 9-month, noninterest-bearing note to the bank. Interest was discounted at a 12% discount rate.

Required:

1. Prepare the appropriate journal entry by Ziegler to record the issuance of the note.

2. Determine the effective interest rate.

3. Suppose the note had been structured as a 12% note with interest and principal payable at maturity. Prepare the appropriate journal entry to record the issuance of the note by Ziegler.

4. Prepare the appropriate journal entry on December 31, 2013, to accrue interest expense on the note described in number 3 for the 2013 financial statements.

(Essay)

4.9/5 (42)

No disclosure is required because an EPA claim is as yet unasserted, and an assessment is not probable. Even if an unfavorable outcome is thought to be probable in the event of an assessment and the amount is estimable, disclosure is not required at this time unless an unasserted claim is probable.

2. This is a gain contingency. Gain contingencies are not accrued even if the gain is probable and reasonably estimable. The gain should be recognized only when realized.

If the amount is deemed material, Barone will disclose information in notes to the financial statements and ensure the wording is not misleading as to the eventual outcome.

(Essay)

4.8/5 (44)

Liabilities payable within the coming year are classified as long-term liabilities if refinancing is completed before date of issuance of the financial statements under:

(Multiple Choice)

4.7/5 (42)

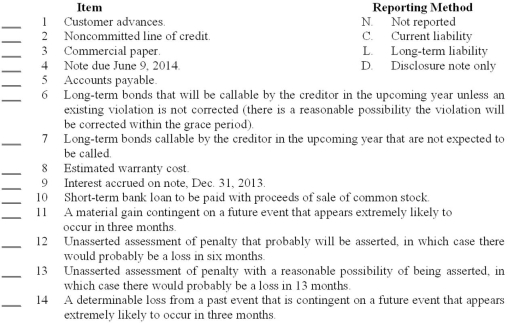

Indicate (by letter) the way each of the items listed below should be reported in a balance sheet at December 31, 2013.

(Essay)

4.7/5 (40)

Bank loans are often arranged in advance as lines of credit. What is a line of credit? How do a committed and a noncommitted line of credit differ?

(Essay)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)