Exam 11: Property, Plant, and Equipment and Intangible Assets: Utilization and Impairment

Exam 1: Environment and Theoretical Structure of Financial Accounting135 Questions

Exam 2: Review of the Accounting Process126 Questions

Exam 3: The Balance Sheet and Financial Disclosures102 Questions

Exam 4: The Income Statement, Comprehensive Income, and the Statement of Cash Flows103 Questions

Exam 5: Income Measurement and Profitability Analysis210 Questions

Exam 6: Time Value of Money Concepts114 Questions

Exam 7: Cash and Receivables164 Questions

Exam 8: Inventories: Measurement126 Questions

Exam 9: Property, Plant, and Equipment and Intangible Assets: Acquisition and Disposition120 Questions

Exam 10: Property, Plant, and Equipment and Intangible Assets: Acquisition and Disposition128 Questions

Exam 11: Property, Plant, and Equipment and Intangible Assets: Utilization and Impairment146 Questions

Exam 12: Investments186 Questions

Exam 13: Current Liabilities and Contingencies153 Questions

Exam 14: Bonds and Long-Term Notes167 Questions

Exam 15: Leases160 Questions

Exam 16: Accounting for Income Taxes145 Questions

Exam 17: Pensions and Other Postretirement Benefits197 Questions

Exam 18: Shareholders Equity Key213 Questions

Exam 19: Share-Based Compensation and Earnings Per Share178 Questions

Exam 20: Accounting Changes and Error Corrections119 Questions

Exam 21: The Statement of Cash Flows Revisited155 Questions

Select questions type

Belotti would record depletion in 2013 of:

Free

(Multiple Choice)

4.8/5  (43)

(43)

Correct Answer: Verified

Verified

B

Changes in the estimates involved in depreciation, depletion, and amortization require retroactive restatement of financial statements.

Free

(True/False)

4.8/5 (41)

Correct Answer:Verified

False

Granite Enterprises acquired a patent from Southern Research Corporation on January 1, 2013, for $4 million. The patent will be used for 5 years, even though its legal life is 20 years. Rocky Corporation has made a commitment to purchase the patent from Granite for $200,000 at the end of five years. Compute Granite's patent amortization for 2013, assuming the straight-line method is used.

Free

(Multiple Choice)

4.7/5 (31)

Correct Answer:Verified

C

Assuming an asset is used evenly over a four-year service life, which method of depreciation will always result in the largest amount of depreciation in the first year?

(Multiple Choice)

4.8/5 (34)

Kentfield Corporation has $260 million of goodwill on its book from the 2010 acquisition of Seaford Shipping. At the end of its 2013 fiscal year, management has provided the following information for a required goodwill impairment test ($ in millions):  Required:

Assuming that Seaford is considered a reporting unit for U.S. GAAP and a cash-generating unit for IFRS, determine the amount of goodwill impairment loss that Kentfield should recognize according to U.S. GAAP and International Financial Reporting Standards.

Required:

Assuming that Seaford is considered a reporting unit for U.S. GAAP and a cash-generating unit for IFRS, determine the amount of goodwill impairment loss that Kentfield should recognize according to U.S. GAAP and International Financial Reporting Standards.

(Essay)

4.8/5 (40)

Nanki Corporation purchased equipment on January 1, 2011, for $650,000. In 2011 and 2012, Nanki depreciated the asset on a straight-line basis with an estimated useful life of eight years and a $10,000 residual value. In 2013, due to changes in technology, Nanki revised the useful life to a total of six years with no residual value. What depreciation would Nanki record for the year 2013 on this equipment?

(Multiple Choice)

4.9/5 (25)

According to International Financial Reporting Standards, the costs to successfully defend an intangible right normally are capitalized and amortized.

(True/False)

4.8/5 (28)

Using the straight-line method, the book value at December 31, 2013, would be:

(Multiple Choice)

4.9/5 (34)

A change from the straight-line method to the sum-of-years'-digits method of depreciation is handled as:

(Multiple Choice)

4.7/5 (45)

Property, plant, and equipment and finite-life intangible assets must be tested for impairment at least once a year.

(True/False)

4.8/5 (32)

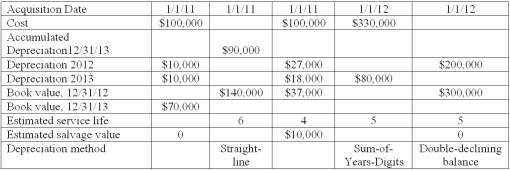

The table below contains data on depreciation for equipment.

Required:

Fill in the missing data in the table.

(Essay)

4.8/5 (38)

Canliss Mining uses the replacement method to determine depreciation on its office equipment. During 2011, its first year of operations, office equipment was purchased at a cost of $14,000. Useful life of the equipment averages four years and no salvage value is anticipated. In 2013, equipment costing $5,000 was sold for $600 and replaced with new equipment costing $6,000. Canliss would record 2013 depreciation of:

(Multiple Choice)

4.7/5 (40)

Fryer Inc. owns equipment for which it paid $90 million. At the end of 2013, it had accumulated depreciation on the equipment of $27 million. Due to adverse economic conditions, Fryer's management determined that it should assess whether an impairment loss should be recognized for the equipment. The estimated undiscounted future cash flows to be provided by the equipment total $60 million, and the equipment's fair value at that point is $40 million. Under these circumstances, Fryer:

(Multiple Choice)

4.9/5 (34)

An impairment loss is indicated because the estimated undiscounted sum of future cash flows of $30 million is less than the book value of $32.1 million.

The amount of the loss to be reported is calculated using the estimated fair value rather than the undiscounted future cash flows:

(Essay)

4.9/5 (34)

The replacement of a major component increased the productive capacity of production equipment from 10 units per hour to 18 units per hour. The expenditure should be debited to:

(Multiple Choice)

4.8/5 (38)

A major expenditure increased a truck's life beyond the original estimate of life. GAAP permits the expenditure to be debited to:

(Multiple Choice)

4.9/5 (39)

2013 depreciation:

Equipment: $100,000 ÷ 5 years = $20,000

Land improvements: $50,000 ÷ 20 years = $2,500

(Essay)

4.7/5 (29)

One of the advantages of group and composite methods is that gains and losses on the disposal of individual assets need not be computed.

(True/False)

4.9/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)