Exam 8: Process Costing Systems

Exam 1: The Role of Accounting Information in Management Decision Making53 Questions

Exam 2: Cost Concepts, Behaviour and Estimation71 Questions

Exam 3: A Costing Framework and Cost Allocation68 Questions

Exam 4: Costvolumeprofit Cvp Analysis66 Questions

Exam 5: Planning Budgeting and Behaviour70 Questions

Exam 6: Operational Budgets69 Questions

Exam 7: Job Costing Systems72 Questions

Exam 8: Process Costing Systems67 Questions

Exam 9: Absorption and Variable Costing69 Questions

Exam 10: Flexible Budgets, Standard Costs and Variance Analysis69 Questions

Exam 11: Variance Analysis: Revenue and Cost68 Questions

Exam 12: Activity Analysis: Costing and Management63 Questions

Exam 13: Relevant Costs for Decision Making71 Questions

Exam 14: Strategy and Control72 Questions

Exam 15: Capital Budgeting and Strategic Investment Decisions58 Questions

Exam 16: The Strategic Management of Costs and Revenues55 Questions

Exam 17: Strategic Management Control: a Lean Perspective54 Questions

Exam 18: Responsibility Accounting, Performance Evaluation and Transfer Pricing50 Questions

Exam 19: The Balanced Scorecard and Strategy Maps54 Questions

Select questions type

Angel Corporation uses activity-based costing to determine product costs for external financial reports. The company has provided the following data concerning its activity-based costing system:

Estimated Activity Cost Pools (and Activity Meseasure overhead Cost Machine related (machine-hours). £81,600 Batch setup (setups). £387,000 General factory (direct labour-hours). £274,800

Activity Cost Pools Total Product X Product Y Machine related. 8,000 3,000 5,000 Batch setup. 10,000 2,000 8,000 General factory 12,000 7,000 5,000

Assuming that actual activity turns out to be the same as expected activity, the total amount of overhead cost allocated to Product X would be closest to:

(Multiple Choice)

4.8/5  (30)

(30)

Outline the advantages and disadvantages of using the simplified ABC approach.

(Essay)

4.9/5 (43)

Bristol Electronics produces wide range of electronic products. The company has a labour based costing system that was introduced in the 1970s and is now considering implementing an activity based costing (ABC) system. Managers are concerned about how they should compare the ABC data with the existing costing system.

Selected data from the management accounts for the year ending 31st December 2000

Cost data Total manufacturing overhead for year £1,000,000 Total hours for year 60,000 hours Direct labour cost per hour £10

Data for 3 products only

Product A F roduct B Product C Annual production 1,000 units 2,000 units 5,000 units Material cost per unit £5.00 £6.00 £7.00 Direct labour hours per unit 1.00 1.50 0.50 ABC data for all products Cost pool / driver Annual costs (£s) Annual volume Number of set-ups 200,000 1,000 Inspection time (hours) 500,000 3,000 Machine maintenance (hours) 100,000 5,000 Number of purchases 100,000 500 Number of shipments 100,000 500 1,000,000

ABC data 3 products Froduct A Froduct B Froduct C Number of set-ups 20 180 30 Inspection time (hours) 20 50 300 Machine maintenance (hours) 30 40 20 Number of purchases 3 4 5 Number of shipments 3 4 6

-Determine the total unit cost for product B using the number of hours to apply overhead

(Multiple Choice)

4.9/5 (37)

Distinguish between unit, batch, product and customer level activities.

(Essay)

4.8/5 (49)

Bristol Electronics produces wide range of electronic products. The company has a labour based costing system that was introduced in the 1970s and is now considering implementing an activity based costing (ABC) system. Managers are concerned about how they should compare the ABC data with the existing costing system.

Selected data from the management accounts for the year ending 31st December 2000

Cost data Total manufacturing overhead for year £1,000,000 Total hours for year 60,000 hours Direct labour cost per hour £10

Data for 3 products only

Product A F roduct B Product C Annual production 1,000 units 2,000 units 5,000 units Material cost per unit £5.00 £6.00 £7.00 Direct labour hours per unit 1.00 1.50 0.50 ABC data for all products Cost pool / driver Annual costs (£s) Annual volume Number of set-ups 200,000 1,000 Inspection time (hours) 500,000 3,000 Machine maintenance (hours) 100,000 5,000 Number of purchases 100,000 500 Number of shipments 100,000 500 1,000,000

ABC data 3 products Froduct A Froduct B Froduct C Number of set-ups 20 180 30 Inspection time (hours) 20 50 300 Machine maintenance (hours) 30 40 20 Number of purchases 3 4 5 Number of shipments 3 4 6

-Determine the total overhead cost for product A using the using the activity based data

(Multiple Choice)

4.8/5 (35)

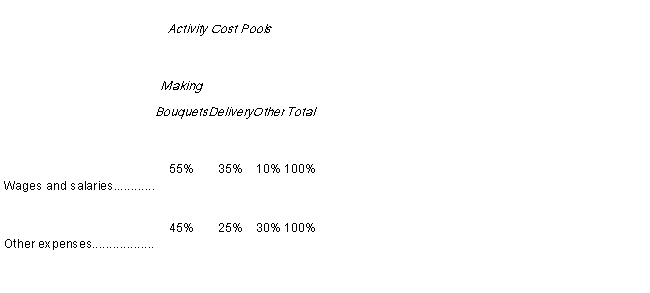

Forrest Florist specialises in large floral bouquets for hotels and other commercial spaces. The company has provided the following data concerning its annual overhead costs and its activity based costing system:

Overhead costs: Wages and salaries £70,000 Other expenses. £40,000 Total. £110,000

Distribution of resource consumption: The 'Other' activity cost pool consists of the costs of idle capacity and organisation-sustaining costs.

The amount of activity for the year is as follows: Activity Cost Pool Activity Making bouquets 20,000 bouquets Delivery. 1,000 deliveries

- What would be the total overhead cost per bouquet according to the activity based costing system? In other words, what would be the overall activity rate for the making bouquets activity cost pool? (Round your answer to the nearest whole pence.)

The 'Other' activity cost pool consists of the costs of idle capacity and organisation-sustaining costs.

The amount of activity for the year is as follows: Activity Cost Pool Activity Making bouquets 20,000 bouquets Delivery. 1,000 deliveries

- What would be the total overhead cost per bouquet according to the activity based costing system? In other words, what would be the overall activity rate for the making bouquets activity cost pool? (Round your answer to the nearest whole pence.)

(Multiple Choice)

4.8/5 (32)

An activity-based costing system that is designed for internal decision-making will not conform to generally accepted accounting principles because:

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)