Exam 11: Criticisms of Absorption Cost Systems: Inaccurate Product Costs

This is a comprehensive problem comparing absorption costing and ABC. It is suggested that as you progress through the problem, keep track of the correct solutions, because these values will be used again later in the problem set. Dehli Inkstone specializes in inkstone creation. Each finished inkstone needs 1½ pounds of special materials which cost $20 a pound. (One pound contains 16 ounces.) Drilling requires 1 direct labor hours, for which workers are paid $10 per hour, and 40 minutes of machine time. The preliminary product (a 'basic') is inspected to ensure that it is sound. Fifteen percent of the basics are rejected. It is not possible to rework these, and they have no salvage value. Each approved stone is handed to a master craftsperson who spends two hours making a 'Standard' product or three hours creating a 'Masterpiece'. Standards use half an hour of machine time and Masterpieces one hour. Finished inkstones are inspected again before packing. Four percent of finished products fail the final quality control assessment and are destroyed. Crafts persons are paid $18 per hour. It takes a 'basic' worker six minutes to package each inkstone in bubble wrap and a shipping carton, which cost 50 cents in materials and weigh 6 ounces in total.

Total overheads are estimated to be $587,400 per year and 97,900 direct labor hours are budgeted. Production plans for the year call for 60% of output to be Standard inkstones and the balance Masterpieces.

Dehli Inkstone recently employed a cost analyst, who recommended the adoption of an ABC system to obtain a more accurate understanding of the costs of the Standard and Masterpiece products. She has classified the overheads into the following four cost pools and identified the appropriate cost drivers: Cost Pool Dollars Cost Driwer Wlaterials handling \ 121,000 Pounds of raw materials Inspection \ 48,400 Inspections Mlachine operation \& maint. \ 163,350 Machine hours Labor-related costs Direct Labor dollars \ 587,400 Independent of your answers above, assume total planned output is 25,595 units. What is the correct materials handling cost rate?

C

Different Overhead Allocation Bases

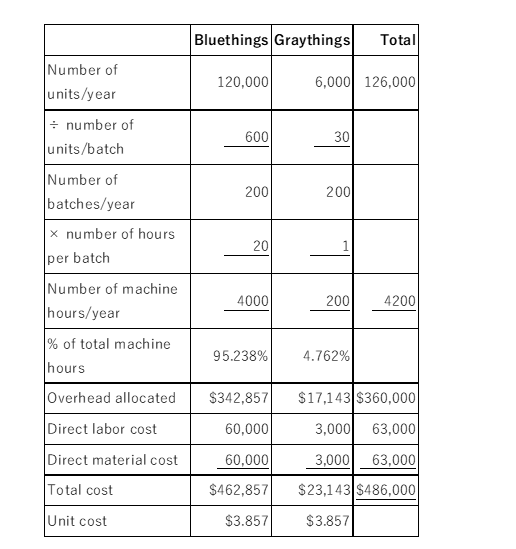

Step Up Inc. produces blue things and gray things. Blue things are in much greater demand in the market and the firm sells 120,000 blue things a year. Step Up Inc. sells 6,000 gray things per year in small boutiques. Things have a short shelf life. They must be distributed, sold, and consumed within two months of manufacture.

Both things use the identical production process and production facilities. Direct labor is $0.50 per thing and direct material is $0.50 per thing. Things are produced in batches. Blue things are produced in batches of 600 units and gray things in batches of 30. Each batch of things goes through the thingamajig, which is the machine that converts raw inputs into things. Each batch requires engineers to reset the machine for the next batch, calibrate settings, and test the first 10 things for product quality and conformity to standards. Even if sequential batches of the same things are made, setups must be performed for each new batch. All the overhead costs are incurred in setups. Indirect labor, indirect materials, and supplies consumed during setup cost $360,000 per year. The only costs of producing things are direct labor, direct materials, and the overhead of setups. The company is currently allocating setup costs to things based on direct labor cost.

The firm has been selling blue things for $4 per unit and gray things for $6 per unit. But foreign competition for blue things is starting to put pressure on the $4 price. Some competitors are selling blue things for as low as $3 per unit. Management is considering putting more emphasis on selling gray things, whose margins are higher. On the other hand, management worries that the current system for allocating overhead costs is misrepresenting the costs of the two products because direct labor costs are not representative of the time spent by each product on the thingamajig. Management is considering allocating setup costs using machine hours on the thingamajig. A batch of gray things requires one hour of machine time and a batch of blue things requires 20 hours of machine time.

Required:

Analyze the present situation. Is there anything wrong with the costing system? If so, should management change to the proposed allocation base of machine hours?

In this problem, there are three possible overhead allocation bases: direct labor (present system), machine hours (the proposed system), and number of batches. First, calculate product costs under each of the three allocation schemes:

1. Direct labor cost as the allocation base (present system):

2. Machine hours as the allocation base (proposed system):

3. Number of batches as the allocation base:

Notice that allocating overhead by either direct labor or machine hours produces identical product costs. Thus, the proposed system change will not affect decision making.

There are two cost drivers in Step Up Company. Unit volume drives direct materials and direct labor, but set-ups (number of batches) appear to drive overhead costs. Allocating overhead using direct labor gives an incorrect impression of how overhead costs vary and distorts product costs. Overhead costs are incurred in set-ups. While run times per unit of thing is the same for blues and grays, batch sizes vary considerably. In fact, bluethings and graythings each required 200 batches. Therefore, each product line (as opposed to each unit of product) should be allocated an equal dollar amount of overhead. If this is done, then graythings become massive losers and bluethings are seen to be profitable, even with market price of $3 per unit.

But these allocated costs using number of batches still do not necessarily represent opportunity costs. If the thing-a-majig and set-up crews are not operating at full capacity, then the opportunity cost of a batch of graythings is $30 (just variable cost). However, if the firm is reducing the number of bluethings it can produce to make graythings (production is at capacity), then the opportunity cost of a graything is the forgone margin on a batch of bluethings plus the variable costs of the graythings. Or,

The decision to continue to make graythings depends on i) how overhead costs vary with batches and ii) whether additional bluethings can be sold if graythings are not produced. If the size and cost of the set-up crew is invariant to the number of batches, then direct labor is probably not too bad an allocation base. If more bluethings cannot be sold, again it is not optimum to drop graythings. Graythings are covering variable cost. Just because all overhead costs are incurred in set-ups does not make set-up costs variable with number of batches. Some of the overhead costs are sunk costs and do not vary with batches (e.g., depreciation of the "thing-a-majig").

For Dehli Inkstone, is it worth implementing a full-fledged ABC system, based upon the findings for these two products?

E

Describe ABC

Required:

a. What is activity-based costing and how does it differ from traditional absorption costing?

b. Describe the advantages and disadvantages of activity-based costing systems.

This is a comprehensive problem comparing absorption costing and ABC. It is suggested that as you progress through the problem, keep track of the correct solutions, because these values will be used again later in the problem set. Dehli Inkstone specializes in inkstone creation. Each finished inkstone needs 1½ pounds of special materials which cost $20 a pound. (One pound contains 16 ounces.) Drilling requires 1 direct labor hours, for which workers are paid $10 per hour, and 40 minutes of machine time. The preliminary product (a 'basic') is inspected to ensure that it is sound. Fifteen percent of the basics are rejected. It is not possible to rework these, and they have no salvage value. Each approved stone is handed to a master craftsperson who spends two hours making a 'Standard' product or three hours creating a 'Masterpiece'. Standards use half an hour of machine time and Masterpieces one hour. Finished inkstones are inspected again before packing. Four percent of finished products fail the final quality control assessment and are destroyed. Crafts persons are paid $18 per hour. It takes a 'basic' worker six minutes to package each inkstone in bubble wrap and a shipping carton, which cost 50 cents in materials and weigh 6 ounces in total.

Total overheads are estimated to be $587,400 per year and 97,900 direct labor hours are budgeted. Production plans for the year call for 60% of output to be Standard inkstones and the balance Masterpieces.

Which is the full (absorption) cost of a Standard inkstone, if machine hours are used as the cost driver? (Allow a little for rounding errors).

This is a comprehensive problem comparing absorption costing and ABC. It is suggested that as you progress through the problem, keep track of the correct solutions, because these values will be used again later in the problem set. Dehli Inkstone specializes in inkstone creation. Each finished inkstone needs 1½ pounds of special materials which cost $20 a pound. (One pound contains 16 ounces.) Drilling requires 1 direct labor hours, for which workers are paid $10 per hour, and 40 minutes of machine time. The preliminary product (a 'basic') is inspected to ensure that it is sound. Fifteen percent of the basics are rejected. It is not possible to rework these, and they have no salvage value. Each approved stone is handed to a master craftsperson who spends two hours making a 'Standard' product or three hours creating a 'Masterpiece'. Standards use half an hour of machine time and Masterpieces one hour. Finished inkstones are inspected again before packing. Four percent of finished products fail the final quality control assessment and are destroyed. Crafts persons are paid $18 per hour. It takes a 'basic' worker six minutes to package each inkstone in bubble wrap and a shipping carton, which cost 50 cents in materials and weigh 6 ounces in total.

Total overheads are estimated to be $587,400 per year and 97,900 direct labor hours are budgeted. Production plans for the year call for 60% of output to be Standard inkstones and the balance Masterpieces.

Which is the full (absorption) cost of a Masterpiece inkstone, if direct labor hours are used as the cost driver? (Allow a little for rounding errors).

Honey Lake Summer Camp

For many years the Honey Lake Summer Camp had used the number of campers per week to estimate weekly costs. The summer camp is open for ten weeks during the summer with a different number of campers each week. July is busiest with June and the end of August least busy. Costs from the last week of summer camp in Year 1 are used to estimate costs for Year 2 for pricing purposes. The following costs occurred during the last week of Year 1 and the costs of each cost category are expected to be the same for Year 2: Wreekly Cost Supervisor's salary \ 400 Cook's salary 300 Camp counselor salaries (1 for each occupied cabin, each of which hold 10 campers) (5 counselors 1,000 \times\ 200/ counselor) Food (50 campers \times\ 100/ camper) 5,000 Supplies (50 campers \times\ 20/ camper) 1,000 Utilities (50 campers \times\ 10/ camper) 500 Insurance (50 campers \times\ 20/ camper) 1,000 Property tax ( \1 0,000/10 weeks) 1,000 Weekly total \ Cost per camper: $12,200/50 campers = $244/camper

The Honey Lake Summer Camp expects 75 campers during the second week of July.

Required:

a. What is the expected cost of that week using the average cost?

b. What is the expected cost of that week using ABC?

This is a comprehensive problem comparing absorption costing and ABC. It is suggested that as you progress through the problem, keep track of the correct solutions, because these values will be used again later in the problem set. Dehli Inkstone specializes in inkstone creation. Each finished inkstone needs 1½ pounds of special materials which cost $20 a pound. (One pound contains 16 ounces.) Drilling requires 1 direct labor hours, for which workers are paid $10 per hour, and 40 minutes of machine time. The preliminary product (a 'basic') is inspected to ensure that it is sound. Fifteen percent of the basics are rejected. It is not possible to rework these, and they have no salvage value. Each approved stone is handed to a master craftsperson who spends two hours making a 'Standard' product or three hours creating a 'Masterpiece'. Standards use half an hour of machine time and Masterpieces one hour. Finished inkstones are inspected again before packing. Four percent of finished products fail the final quality control assessment and are destroyed. Crafts persons are paid $18 per hour. It takes a 'basic' worker six minutes to package each inkstone in bubble wrap and a shipping carton, which cost 50 cents in materials and weigh 6 ounces in total.

Total overheads are estimated to be $587,400 per year and 97,900 direct labor hours are budgeted. Production plans for the year call for 60% of output to be Standard inkstones and the balance Masterpieces.

What is true when ABC is used in Dehli Inkstone?

ABC Systems Can Still Produce Inaccurate Product Costs

Accurate Cost Manufacturing, Inc., manufactures and sells large business equipment for the office and business markets. The primary function of Manufacturing is to provide components and subassemblies for the profit centers within the company. To maintain competitiveness, each profit center can purchase parts either from Manufacturing or from outside firms. Manufacturing operates as a cost center and charges the profit centers for the full cost of the parts. Costs are computed once a year using full absorption costing. The volume of parts used to calculate costs is provided by the profit centers to Manufacturing in August; the fiscal year begins in January. With these numbers, Manufacturing projects costs per part for the year. These cost estimates are then used throughout the year to charge the profit centers. Any over/under-absorbed overhead goes directly to the bottom line of the company, not to any of the profit centers.

Within Manufacturing there is a department called finishing. The finishing department provides a service to other Manufacturing departments and profit centers as well as generating some external sales. Types of finishing include painting and plating. The facility has large investments in fixed assets in both automation and environmental compliance for finishing. The finishing operation believes it provides value to customers through its high quality and its close location to the manufacturing departments.

During the past year, the profit centers have begun taking work away from Manufacturing and giving it to outside vendors with lower quoted costs. Manufacturing then has lower volumes and has to raise the prices on the products it is producing, causing the profit centers to send even more work out. Manufacturing feels it is caught in a death spiral.

The death spiral situation has affected finishing the most. The finishing department is currently operating at 30 percent of capacity and has facilities that are too large for the low volume of work. Table 1 summarizes the data pertaining to finishing. Fixed costs make up 71 percent of the current cost structure. Other manufacturing departments are beginning to tell finishing that they will be sending their work out to get plating and painting so as not to lose any work because of the high internal cost of finishing.

Finishing is trying to attract business from outside Accurate Cost Manufacturing. The external sales guidelines require a 35 percent profit margin applied to the full cost for all external work. With the current low level of work and high fixed costs, finishing cannot attract external sales due to cost.

In an effort to gain control of the true cost drivers of the business, the manager of the finishing operation has implemented activity-based costing. Tables 2 and 3 project the cost for products and volumes for one plating operation. The problem that the finishing manager now faces is that the manufacturing departments are about to send the 12-inch and 18-inch work to an outside shop due to lower costs.

In implementing activity-based costing, the manager thinks he has truly identified the proper system. The larger parts tend to run in smaller lot sizes and generate more paperwork. Smaller parts tend to be run in larger lot sizes and generate less paperwork.

In a recent meeting with the management of the manufacturing department and profit centers, it was stated that the installation of activity-based costing is in direct conflict with the change in the mix of work from small parts to large parts and the need to run smaller lot sizes. The manufacturing department and profit centers would like to pursue just-in-time manufacturing and further reduce the lot sizes for both small and large parts. During this meeting, the profit centers and manufacturing departments said the implementation of activity-based costing would force them to move their work out of the finishing department to outside shops. Table 1

Finishing Annual Cost Structure

Annual\nobreakspaceCost Fixed asset depreciation \ 400,000 \ 4,000,000 machine purchased 2 years a go Tank operations costs 250,000 Cost to operate tanks- fixed cost, not volume dependent Tank material cost 50,000 Cost to operate tanks- \ 0.007575/ inch Variable labor cost 210,000 \ 10/ hour \times21,000 hours of operation Total \ 910,000

Table 2

Finishing Costs before and after Activity-Based Costing

Volume of Pieces per Year Old Cost per Piece Activity- Based Cost per Piece Outside Cost per Piece parts 1,000,000 \ 0.50 \ 0.31 \ 0.30 200,000 1.00 1.00 1.10 parts 1 parts 50,000 1.20 2.00 0.90 1 100,000 1.50 3.00 1.20 parts

Table 3 Forecasted Costs

Old Cost Activity-Based Cost Outside Cost parts \ 500,000 \ 310,000 \ 300,000 parts 200,000 200,000 220,000 1 parts 60,000 100,000 45,000 1 parts 150,000 300,000 120,000 Total per year \ 910,000 \ 910,000 \ 685,000 Required:

a. Analyze the current situation in this company. What should be done?

b. Compare and comment on the costs before and after ABC is implemented.

c. Has finishing management made a mistake by installing activity-based costing?

This is a comprehensive problem comparing absorption costing and ABC. It is suggested that as you progress through the problem, keep track of the correct solutions, because these values will be used again later in the problem set. Dehli Inkstone specializes in inkstone creation. Each finished inkstone needs 1½ pounds of special materials which cost $20 a pound. (One pound contains 16 ounces.) Drilling requires 1 direct labor hours, for which workers are paid $10 per hour, and 40 minutes of machine time. The preliminary product (a 'basic') is inspected to ensure that it is sound. Fifteen percent of the basics are rejected. It is not possible to rework these, and they have no salvage value. Each approved stone is handed to a master craftsperson who spends two hours making a 'Standard' product or three hours creating a 'Masterpiece'. Standards use half an hour of machine time and Masterpieces one hour. Finished inkstones are inspected again before packing. Four percent of finished products fail the final quality control assessment and are destroyed. Crafts persons are paid $18 per hour. It takes a 'basic' worker six minutes to package each inkstone in bubble wrap and a shipping carton, which cost 50 cents in materials and weigh 6 ounces in total.

Total overheads are estimated to be $587,400 per year and 97,900 direct labor hours are budgeted. Production plans for the year call for 60% of output to be Standard inkstones and the balance Masterpieces.

For a Masterpiece inkstone, which is true of the direct labor hours (DLH) needed (to 3 decimal places)?

ABC versus Traditional Absorption Costing

Last year CCB Medical Technologies (CCB) introduced a proprietary orthopedic surgical saw that is used in a variety of orthopedic applications. However, its largest demand is in hip replacement surgeries. The electric reciprocating saw's patented technology (including the blade) reduces noise and vibration and increases precision cutting, thereby reducing postoperative complications. CCB manufactures and sells both the saw and blades. CCB blades are designed and engineered specifically for the CCB saw, and CCB saws are designed to only be used with CCB blades. When an orthopedic surgeon performs a surgery, each blade is dedicated to one particular patient and, once used, the blade is discarded. Surgeons often use two or three blades during surgery on a patient. CCB saws sell for $2,000 each and CCB blades sell for $450 per blade.

CCB manufactures both the saw and blades in the same factory. The following table summarizes the variable and direct costs of the saws and blades and the number of units of each product produced and sold last year. Saws Blades Units produced 330 12,00 Units sold 300 9.000 Beginning inventory 0 0 Direct labor per unit \ 54.00 \ 12.00 Direct materials per unit \ 185.00 \ 38.00 Variable manufacturing overhead per unit \ 22.00 \ 8.00 CCB uses an activity-based costing system to assign fixed manufacturing overhead to the saws and blades. There are three fixed manufacturing overhead cost pools in the ABC system: batch costs, product-line engineering costs, and other factory overhead. The following describes the ABC methodology:

• Batch costs ($173,000 last year): Batch costs are allocated to the two product lines based on the number of batches manufactured during the year. Saws are produced in batch sizes of 10 saws per batch and blades are manufactured in batch sizes of 500 blades per batch.

• Product-line engineering costs ($724,000 last year): Product-line engineering costs are assigned to the two product lines (saws and blades) after a survey of the engineers inquiring how they spent their time. Based on last year's survey, $289,000 was assigned to saws and $435,000 was assigned to blades.

• Other factory overhead ($330,000): Other factory overhead consists of all other fixed manufacturing overhead not included in either batch costs or product-line engineering costs. These costs are allocated to the saws and blades based on direct labor cost.

Required:

a. Compute CCB's unit manufacturing costs and operating margins (revenues less cost of goods sold) for last year for the saws and blades using the activity-based costing methodology described above.

b. Having seen the ABC income statements prepared in part (a), CCB management wants to see how the operating margins (revenues less cost of goods sold) for the saws and blades would look if traditional absorption costing is used where the total fixed factory overhead is allocated to the saws and blades using direct labor dollars.

c. Make a recommendation to management as to whether ABC (part a) or traditional absorption costing (part b) should be used. Justify your recommendation.

This is a comprehensive problem comparing absorption costing and ABC. It is suggested that as you progress through the problem, keep track of the correct solutions, because these values will be used again later in the problem set. Dehli Inkstone specializes in inkstone creation. Each finished inkstone needs 1½ pounds of special materials which cost $20 a pound. (One pound contains 16 ounces.) Drilling requires 1 direct labor hours, for which workers are paid $10 per hour, and 40 minutes of machine time. The preliminary product (a 'basic') is inspected to ensure that it is sound. Fifteen percent of the basics are rejected. It is not possible to rework these, and they have no salvage value. Each approved stone is handed to a master craftsperson who spends two hours making a 'Standard' product or three hours creating a 'Masterpiece'. Standards use half an hour of machine time and Masterpieces one hour. Finished inkstones are inspected again before packing. Four percent of finished products fail the final quality control assessment and are destroyed. Crafts persons are paid $18 per hour. It takes a 'basic' worker six minutes to package each inkstone in bubble wrap and a shipping carton, which cost 50 cents in materials and weigh 6 ounces in total.

Total overheads are estimated to be $587,400 per year and 97,900 direct labor hours are budgeted. Production plans for the year call for 60% of output to be Standard inkstones and the balance Masterpieces.

For a Standard inkstone, which is true of the materials input needed (to 3 significant figures)?

When traditional absorption costing is employed, which of the following is false?

This is a comprehensive problem comparing absorption costing and ABC. It is suggested that as you progress through the problem, keep track of the correct solutions, because these values will be used again later in the problem set. Dehli Inkstone specializes in inkstone creation. Each finished inkstone needs 1½ pounds of special materials which cost $20 a pound. (One pound contains 16 ounces.) Drilling requires 1 direct labor hours, for which workers are paid $10 per hour, and 40 minutes of machine time. The preliminary product (a 'basic') is inspected to ensure that it is sound. Fifteen percent of the basics are rejected. It is not possible to rework these, and they have no salvage value. Each approved stone is handed to a master craftsperson who spends two hours making a 'Standard' product or three hours creating a 'Masterpiece'. Standards use half an hour of machine time and Masterpieces one hour. Finished inkstones are inspected again before packing. Four percent of finished products fail the final quality control assessment and are destroyed. Crafts persons are paid $18 per hour. It takes a 'basic' worker six minutes to package each inkstone in bubble wrap and a shipping carton, which cost 50 cents in materials and weigh 6 ounces in total.

Total overheads are estimated to be $587,400 per year and 97,900 direct labor hours are budgeted. Production plans for the year call for 60% of output to be Standard inkstones and the balance Masterpieces.

For a Standard inkstone, which is true of the machine hours (MH) needed (to 3 decimal places)?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)