Exam 7: Cost Allocation: Theory

The maintenance department's costs are allocated to other departments based on the number of hours of maintenance use by each department. The maintenance department has fixed costs of $500,000 and variable costs of $30 per hour of maintenance provided. The variable costs include the salaries of the maintenance workers. More maintenance workers can be added if greater maintenance is demanded by the other departments without affecting the fixed costs of the maintenance department. The maintenance department expects to provide 10,000 hours of maintenance.

Required:

a. What is the application rate for the maintenance department?

b. What is the additional cost to the maintenance department of providing another hour of maintenance?

c. What problem exists if the managers of other departments can choose how much maintenance to be performed?

d. What problem exists if the other departments are allowed to go outside the organization to buy maintenance services?

a. Total expected costs are $500,000 + ($30/hour) (10,000 hours) = $800,000

The application rate is $800,000/10,000 hours = $80/hour

b. The additional cost to the maintenance department of providing another hour of maintenance is the variable cost of $30/hour.

c. The other departments will under-use the maintenance department because the application rate of $80/hour is much greater than the additional costs of providing maintenance.

d. If departments are allowed to go outside the organization to buy maintenance services, fewer in-house maintenance hours will be used. This will cause the application rate to become even higher if the fixed cost is included.

The Independent Underwriters Insurance Co. (IUI) established a systems department two years ago to implement and operate its information technology system. IUI believed that its own system would be more cost-effective than the service bureau it had been using.

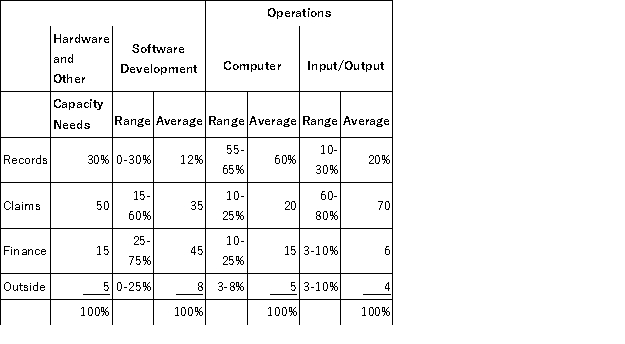

IUI's three departments - claims, records, and finance - have different requirements with respect to hardware and other capacity-related resources and operating resources. The system was designed to recognize these differing demands. It was also designed to meet IUI's long-term capacity. The excess capacity designed into the system is being sold to outside users until IUI needs it. The estimated resource requirements used to design and implement the system are shown in the following schedule. Hardware and Other Capacity- Related Resources Dperating Resources Records 30\% 60\% Claims 50 20 Finance 15 15 Expansion (outside use) 5 5 Total 100\% 100\% IUI currently sells the equivalent of its expansion capacity to a few outside clients.

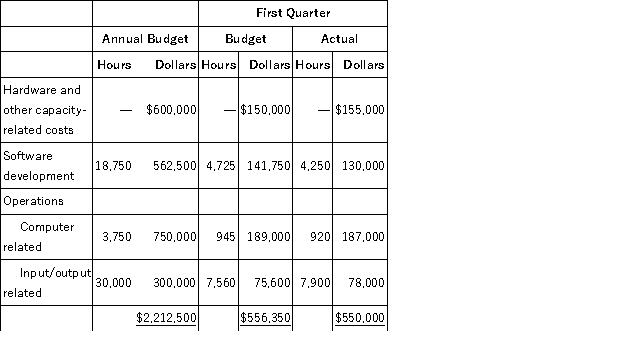

When the system became operational, management decided to redistribute total expenses of the systems department to the user departments based upon actual computer time used. The actual costs for the first quarter of the current fiscal year were distributed to the user departments as follows: Department Percentage Utilization Amount Records 60\% \ 330,000 Claims 20 110,000 Finance 15 82,500 Outside 5 27,500 Total 100\% \ 550,000 The three user departments have complained about the cost distribution since the systems department was established. The records department's monthly costs have been as much as three times the costs experienced with the service bureau. The finance department is concerned about the costs distributed to the outside user category, because these allocated costs form the basis for the fees billed to outside clients.

James Dale, IUI's controller, decided to review the distribution method by which the systems department's costs have been allocated for the past two years. The additional information he gathered for his review is reported in Tables 1, 2, and 3. Dale has concluded that the method of cost distribution should be changed to reflect more directly the actual benefits received by the departments. He believes that hardware and capacity-related costs should be allocated to the user departments in proportion to their planned, long-term needs. Any difference between actual and budgeted hardware costs should remain with the systems department.

The remaining costs for software development and operations would be charged to the user departments based upon actual hours used. A predetermined hourly rate based upon the annual budget data would be used. The hourly rates proposed for the current fiscal year are as follows: Function Hourly Rate Software development \ 30 Operations Computer related \ 200 Input/output related \ 10 Dale plans to use first-quarter activity and cost data to illustrate his recommendations. The recommendations will be presented to the systems department and the user departments for their comments and reactions. He then expects to present his recommendations to management for approval.

Required:

a. Prepare a schedule to show how the actual first-quarter costs of the systems department will be charged to the users if James Dale's recommended method is adopted.

b. Explain whether James Dale's recommended system for charging costs to the user departments will

(i) Improve cost control in the systems department.

(ii) Improve planning and cost control in the user departments.

(iii) Be a more equitable basis for charging costs to user departments.

Table1

SystemsDepartmentCostsandActivityLevels  Table2

HistoricalUtilizationbyUsers

Table2

HistoricalUtilizationbyUsers  Table3

UtilizationofSystemsDepartment'sServicesforFirstQuarter

(in Hours)

Software Computer Input/Output Development Related Records 425 552 1,580 Claims 1.700 184 5,530 Finance 1.700 138 395 Outside 425 46 395 Total 4,250 920 7,900 This problem, while couched as a cost allocation issue, is in effect a transfer pricing problem.

Table3

UtilizationofSystemsDepartment'sServicesforFirstQuarter

(in Hours)

Software Computer Input/Output Development Related Records 425 552 1,580 Claims 1.700 184 5,530 Finance 1.700 138 395 Outside 425 46 395 Total 4,250 920 7,900 This problem, while couched as a cost allocation issue, is in effect a transfer pricing problem.

a.

b. (i) The new charging system is a form of transfer pricing and should improve cost control in the Systems Department (if the rates are valid) because inefficiencies can no longer be passed on to the user departments. Thus, the Systems Department would be forced to watch its costs more closely.

(ii) The recommended system for charging costs to user departments should improve planning and cost control in the user departments. The users will request service only if its benefits exceed its cost because the user charge is dependent upon services received and not Service Department costs.

(iii) The recommended system for charging costs to user departments appears more equitable than the present system because it is an insulating allocation scheme. No longer will the cost of serving one user affect the charge to other users. However, this reduces the incentives for the users to cooperate.

The old aggregate allocation basis used a single allocation base (computer time) to allocate the costs. In a multi-operational department such as the Systems Department, the use of pre-determined rates for different services (software, input/output, etc.) each requiring different skill levels can be more reasonable in some circumstances (see Chapter 11).

Encryption, Inc. (EI), sells and maintains fax encryption hardware and software. EI hardware and software are attached to both sending and receiving fax machines that encode/decode data, preventing anyone from wiretapping the phone line to receive a copy of the fax.

Two EI product groups (Federal Systems and International) manufacture and sell the hardware and software in different markets. Both are profit centers. Federal Systems contracts with federal government agencies to manufacture, install, and service EI products. Existing contracts call for revenues of $1 million per quarter for the next eight quarters.

International is currently seeking foreign buyers. Expected quarterly revenues will be $1 million, but with equal likelihood revenues can be $1.5 or $0.5 million in any given quarter.

Federal Systems and International each have their own products that differ in some ways but share a common underlying technology. Fax encryption is a new technology and offers new markets. Transferring manufacturing and marketing ideas across products and customers provides important synergies.

The variable cost of Federal Systems and International is 50 percent of revenues. The only fixed cost in EI is its Engineering Design group.

Engineering Design is EI's R…D group. It designs new hardware and software that Federal Systems and International sell. Quarterly expenses for Engineering Design will be $0.60 million for the next two years. These expenses do not vary with revenues or production costs.

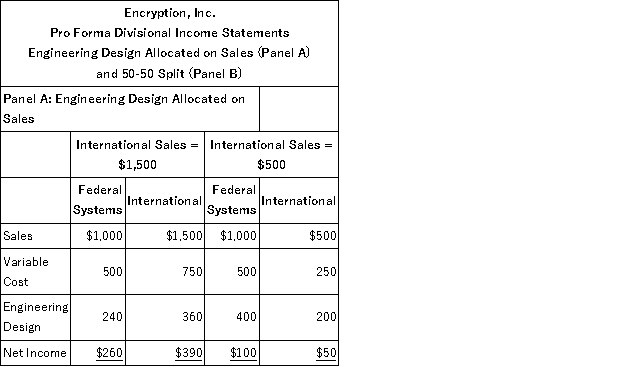

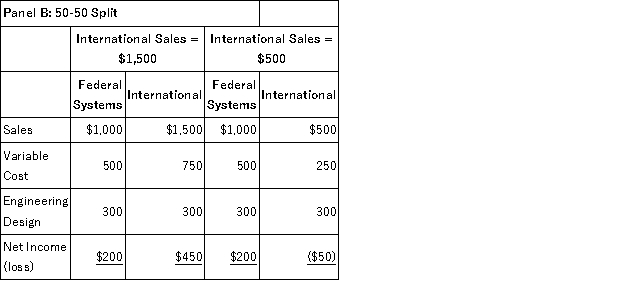

Engineering Design costs are to be included in calculating profits for the Federal Systems and International groups. Two ways of assigning the Engineering Design costs to Federal Systems and International are (1) group revenues, and (2) an even 50-50 split.

Required:

a. Prepare financial statements for Federal Systems and International illustrating the effects of the alternative ways of handling Engineering Design costs.

b. Which method of assigning Engineering Design costs do you favor? Why?

a. The following financial statement calculates the profits of the two divisions using the two alternative cost allocations schemes:

b. I prefer to allocate Engineer Design costs based on sales (Panel A). First, it is a non-insulating allocation scheme, meaning that each divisions' profits vary inversely with the other's profits. For example, Federal System's profits will either be $260 or $100, even though their sales and costs remain constant over time. With an even split (Panel B), Federal System's profits do not vary, they remain at $200. Non-insulating schemes encourage cooperation among divisions by giving each division an incentive to improve other divisions' sales and thereby their own profits. Second, the non-insulating scheme reduces the risk International bears and is likely to result in more efficient risk sharing. For example, consider the range of profits each division faces under the two schemes:

b. I prefer to allocate Engineer Design costs based on sales (Panel A). First, it is a non-insulating allocation scheme, meaning that each divisions' profits vary inversely with the other's profits. For example, Federal System's profits will either be $260 or $100, even though their sales and costs remain constant over time. With an even split (Panel B), Federal System's profits do not vary, they remain at $200. Non-insulating schemes encourage cooperation among divisions by giving each division an incentive to improve other divisions' sales and thereby their own profits. Second, the non-insulating scheme reduces the risk International bears and is likely to result in more efficient risk sharing. For example, consider the range of profits each division faces under the two schemes:

In panel A, Federal System's net income is either $260 or $100, a range of $160. Whereas in Panel B, Federal System's net income is always $200, a range of zero. The insulating method (panel B) imposes all the risk on International. The non-insulating method spreads some of the risk to Federal Systems. Some may argue that it is not "fair" to Federal to bear some of International's risk. Certainly, Federal will have to be paid to bear this risk via a risk premium. However, by imposing this risk on Federal it creates incentives for Federal to cooperate with International by sharing production, marketing, and selling ideas.

Allocating Overhead versus Direct Tracing

Nixon & Ross, a law firm, is about to install a new accounting system that will allow the firm to track more of the overhead costs to individual cases. Overheads are currently allocated to individual client cases based on billable professional staff salaries. Attorneys working on client cases charge their time to "billable professional staff salaries." Attorney time spent in training, law firm administrative meetings, and the like is charged to an overhead account titled "unbilled staff salaries."

The following is a summary of the costs for the current year: Billable professional staff salaries \ 4,000,000 Overhead 8,000,000 Total costs \ 12,000,000 The overhead costs were as follows: Secretarial costs \ 1,500,000 Staff benefits 2,750,000 Office rent 1,250,000 Telephone and mailing costs 1,500,000 Unbilled staff salaries 1,000,000 Total costs \ 8,000,000 Under the new accounting system, the firm will be able to trace secretarial costs, staff benefits, and telephone and mailing costs to specific clients.

The following are the costs incurred on the Lawson Company case: Billable professional staff salaries \ 150,000 Secretarial costs 25,000 Staff benefits 13,500 Telephone and mailing costs 8,000 Total costs \ 196,500 Required:

a. Calculate the current year's overhead application rate under the old cost accounting system.

b. How would this application rate change if the secretarial costs, staff benefits, and telephone and mailing costs were reclassified as direct costs instead of overhead, and overhead was assigned based on direct costs (instead of staff salaries)? Direct costs are defined as billable staff salaries plus secretarial costs, staff benefits, and telephone and mailing costs.

c. Use the overhead application rates from (a) and (b) to compute the cost of the Lawson case.

d. Nixon & Ross bills clients 150 percent of the total costs of the job. What will be the total billings to the Lawson Co. if the old overhead application scheme is replaced with the new overhead scheme?

e. Steve Nixon, managing partner, has commented that replacing the old allocation system with the direct charge method of the new accounting system will result in more accurate costing and pricing of cases. Evaluate the new system.

Five departments of National Training Institute, a nonprofit organization, share a rented building. Four of the departments provide services to educational agencies and have little or no competition for their services. The fifth department, Technical Training, provides educational services to the business community in a competitive market with other nonprofit and private organizations. Each department is a cost center. Revenues received by Technical Training are based on a fee for services, identified as tuition.

All five departments have dedicated space as listed in the accompanying table. Common shared space, including hallways, restrooms, meeting rooms, and dining areas, is not included in these allocations. National Training Institute rents space at $10 per square foot. Allocation Table Department Square Percentage Revenue Footage of Space Administration 13.500 9.0\% \ 3.600,000 Support services 46,500 31.0 11,000,000 Computer services 12,000 8.0 8.800,000 Technical training 6,000 4.0 1,900,000 Transportation 72,000 48.0 4,700,000 Total allocated 150,000 100.0\% \ 30,000,000 Common space 50,000

In addition to its assigned space, the technical training department offers training during off-hours using many of the areas allocated to other departments. Technical Training also uses off-site facilities for the same purpose. About 50 percent of its training activities are in off-site facilities, which have excess capacity, charge no rent, and are available only during off-hours.

John Daniels, the administration department's business manager, proposed a rental allocation plan based on each department's percentage of dedicated square footage plus the same percentage of the common space. The technical training department would be charged an additional amount for the space it uses during off-hours that is dedicated to other departments. This additional amount would be based on planned usage per year.

Jane Richards, director of technical training, claims this allocation method will cause her to increase the price of services. As a result, she will lose business to competition. She would rather see the allocation method use the percentage of department revenue in relation to total revenue.

Required:

Comment on Daniels's and Richards's proposed rent allocation plans. Make appropriate recommendations.

Eastern University prides itself on providing faculty and staff a competitive compensation package. One aspect of this package is a faculty and staff child tuition benefit of $4,000 per child per year for up to four years to offset the cost of a college education. The faculty or staff member's child can attend any college or university, including Eastern University, and receive the tuition benefit. If a staff member has three children in college one year, the staff member receives a $12,000 tuition benefit. This money is not taxed to the individual staff or faculty member.

Eastern University pays the benefit directly to the university where the staff/faculty member's child is enrolled or if the student is attending Eastern, it reduces the amount of tuition owed by the faculty/staff member. The university then charges this payment to a benefits account. This benefits account is then allocated back to the various colleges and departments based on total salaries in the college or department.

Required:

Evaluate the pros and cons of the present university accounting for tuition benefits. What changes would you recommend making?

Pluton makes particular plastics for sale to the public and the government. Basic cost data for a 100-pound drum of one particular product called Xentra appears below: Qty Cost Chemical Xeta, gals 15 \ 25.00 Chemical Thenta, gals 35 \ 27.50 Base material, lbs 20 \ 1.00 100 -Ib lined drum 1 \ 51.83 Variable factory overheads are estimated to be $1,200,000 per month, when 1,000,000 pounds of various products are produced. The plant employs 20 chemical workers who typically work 175 hours each per month and are paid $24 per hour. Other workers are classified as indirect and are included in fixed overheads. The highly automated plant typically runs 21,000 machine hours per month. The preparation of one 100 lbs batch of Xentra needs ten minutes of direct labor and 75 minutes of machine time. Fixed manufacturing overheads total $3,500,000 per month. Forty percent of these fixed manufacturing overheads are labor-related costs and the balance are machine-related costs. A government agency wants to purchase 200 drums of Xentra at cost plus a flat fee. Which allocation method gives the profit-maximizing result?

Bio Labs is a genetic engineering firm manufacturing a variety of gene-spliced, agricultural-based seed products. The firm has five separate laboratories producing different product lines. Each lab is treated as a profit center and all five labs are located in the same facility. The wheat seed lab and corn seed lab manufacture two of the five product lines. These two labs are located next to each other and are of roughly equal size in terms of sales. The two departments have close interaction, often sharing equipment and lab technicians. Both use very similar technology and science and usually attend the same scientific meetings.

Recent discoveries have shown how low-power lasers can be used to significantly improve product quality. The wheat seed and corn seed managers are proposing the creation of a laser testing department to employ this new technology. Leasing the equipment and hiring the personnel cost $350,000 per year. Supplies, power, and other variable costs are $25 per testing hour. The testing department is expected to provide 2,000 testing hours per year. The wheat seed manager expects to use 700 testing hours per year of the laser testing department and the corn seed manager expects to use 800 testing hours. The remaining 500 hours of testing capacity can be used by the other three labs if the technology applies or can be left idle for future expected growth of the two departments. Initially, only wheat and corn are expected to use laser testing.

The executive committee of Bio Labs has approved the proposal but is now grappling with how to treat the costs of the laser testing department. The committee wants to charge the costs to the wheat seed and corn seed labs but is unsure of how to proceed.

At the end of the first year of operating the laser, wheat seed used 650 testing hours, corn seed used 900 hours, and 450 hours were idle.

Required:

a. Design two alternative cost allocation systems.

b. Give numerical illustrations of the charges the corn and wheat seed labs will incur in the first year of operations under your two alternatives.

c. Discuss the advantages and disadvantages of each.

Cost Allocations can Change the Relative Profitability of Products

Woodley Furniture is a small boutique manufacturer of high quality contemporary wood tables. They make two models: end tables and coffee tables in a variety of different woods and finishes. Current annual production of end tables is 8,000 units that sell for $250 and have variable cost of $120 each. Current annual production of coffee tables is 6,000 units that sell for $475 and have variable cost of $285 each. Woodley has fixed costs of $2.4 million. Woodley sells all the tables they produce each year.

Required:

a. Calculate total firm-wide profits and product-line profits for the end tables and coffee tables after allocating the fixed costs to the two product lines using sales revenues as the allocation base.

b. Which of the two products is the most profitable based on total profits (after allocating fixed costs)? Is Woodley making an adequate profit?

c. Woodley management decides to add a dining table to its product offerings. The plant currently has excess capacity, so no additional fixed costs are required to produce the dining tables. The new dining table will not affect the number of units sold or prices of the existing coffee and end tables. They expect to sell 4,000 dining tables at a price of $620 each, and variable cost per table is $500. Calculate total firm-wide profits and product-line profits for the end tables, coffee tables, and dining tables after allocating the fixed costs to the three product lines using sales revenues as the allocation base.

d. Analyze the profitability of the three products and firm-wide profits calculated in part (c) compared to the profitability of the two products alone and firm-wide profits in part (a).

e. Recalculate your answers to parts (a) and (c), but, instead of allocating the $2.4 million of fixed costs using sales revenues as in parts (a) and (c), allocate the $2.4 million of fixed costs using the total contribution margin of each product (total sales revenue less total variable cost).

f. Discuss the relative advantages and disadvantages of using total contribution margin to allocate the fixed costs in part (e) relative to using sales revenues to allocate the fixed costs, as in parts (a) and (c).

Cost Allocations Can Distort Pricing Decisions

Kraft Foods Group used to sponsor a car in the NASCAR races. Like other major corporations that sponsor sports events, Kraft believes that the public's awareness of its products is enhanced by sponsoring a NASCAR. For the right to have "Kraft" displayed prominently on the automobile, Kraft pays the racing team an annual fee.

Kraft is organized around a number of business units that are profit centers. Senior management at Kraft believes that since the various business units at Kraft receive the benefits of the NASCAR exposure through greater name recognition, and hence greater sales, the costs of the program should be allocated back to the business units and ultimately to all Kraft products. The cost of the NASCAR program is allocated back to the Kraft business units based on sales revenue. Suppose the allocation is 10 percent of revenues. That is, for every $1 of revenue, the business unit is allocated $0.10 of cost from the NASCAR car.

One of Kraft's business units sells Velveeta processed cheese in cartons containing 200 32 ounce packages. The following table summarizes possible pricing levels, cartons sold at that price, and costs for the various number of cartons. Price Number of Cartons Sold Total Cost \ 564 218 \ 71,800 562 219 71,900 560 220 72,000 558 221 72,100 556 222 72,200 554 223 72,300 552 224 72,400 550 225 72,500 548 226 72,600 Required:

a. What price-quantity combination maximizes the profits of the Velvetta, ignoring the allocation of NASCAR?

b. If $0.10 of the NASCAR is allocated for every dollar of Velvetta revenue, what price-quantity combination of Velvetta maximizes profits after allocating NASCAR costs?

c. What price-quantity combination of Velvetta maximizes profits after allocating NASCAR costs using total costs (instead of revenues), where for every dollar of total costs, $0.20 of NASCAR costs are allocated?

d. Instead of allocating the NASCAR based on revenues, it is allocated based on profits before allocated costs. For every $1.00 of profits before allocated costs, $0.30 of NASCAR costs are allocated. Now what price-quantity combination maximizes Velvetta profits after allocating NASCAR costs?

e. Should NASCAR costs be allocated to the business units, and if so, what allocation scheme should be used (revenues, costs, or profits)?

Pluton makes particular plastics for sale to the public and the government. Basic cost data for a 100-pound drum of one particular product called Xentra appears below: Qty Cost Chemical Xeta, gals 15 \ 25.00 Chemical Thenta, gals 35 \ 27.50 Base material, lbs 20 \ 1.00 100 -Ib lined drum 1 \ 51.83 Variable factory overheads are estimated to be $1,200,000 per month, when 1,000,000 pounds of various products are produced. The plant employs 20 chemical workers who typically work 175 hours each per month and are paid $24 per hour. Other workers are classified as indirect and are included in fixed overheads. The highly automated plant typically runs 21,000 machine hours per month. The preparation of one 100 lbs batch of Xentra needs ten minutes of direct labor and 75 minutes of machine time. Fixed manufacturing overheads total $3,500,000 per month. Forty percent of these fixed manufacturing overheads are labor-related costs and the balance are machine-related costs. Assuming normal production levels, what is the conversion cost (direct labor and overhead) per drum?

Pluton makes particular plastics for sale to the public and the government. Basic cost data for a 100-pound drum of one particular product called Xentra appears below: Qty Cost Chemical Xeta, gals 15 \ 25.00 Chemical Thenta, gals 35 \ 27.50 Base material, lbs 20 \ 1.00 100 -Ib lined drum 1 \ 51.83 Variable factory overheads are estimated to be $1,200,000 per month, when 1,000,000 pounds of various products are produced. The plant employs 20 chemical workers who typically work 175 hours each per month and are paid $24 per hour. Other workers are classified as indirect and are included in fixed overheads. The highly automated plant typically runs 21,000 machine hours per month. The preparation of one 100 lbs batch of Xentra needs ten minutes of direct labor and 75 minutes of machine time. Fixed manufacturing overheads total $3,500,000 per month. Forty percent of these fixed manufacturing overheads are labor-related costs and the balance are machine-related costs. Assuming normal production levels, what is the full cost per drum?

Peluso Company, a manufacturer of snowmobiles, is operating at 70 percent of plant capacity. Peluso's plant manager is considering manufacturing headlights, which are now being purchased for $11 each (a price that is not expected to change in the near future). The Peluso plant has the equipment and labor force required to manufacture the headlights. The design engineer estimates that each headlight requires $4 of direct materials and $3 of direct labor. Peluso's plant overhead rate is 200 percent of direct labor dollars, and 40 percent of the overhead is fixed cost.

Required:

If Peluso Co. manufactures the headlights, how much of a gain (loss) for each headlight will result?

Telstar Electronics manufactures and imports a wide variety of consumer and industrial electronics, including stereos, televisions, camcorders, telephones, and VCRs. Each line of business (LOB) handles a single product group (e.g., televisions) and is organized as a profit center. The delivery of the product to the wholesaler or retailer is handled by Telstar's distribution division, a cost center. Previously, Telstar was organized functionally, with manufacturing, marketing, and distribution as separate cost centers. Two years ago, it reorganized to the present arrangement.

Distribution assembles products from the various LOBs into larger shipments to the same geographic area to capture economies of scale. The division is also responsible for inbound shipments and storage of imported products. It has its own fleet of trucks, which handles about two-thirds of the shipments, and uses common carriers for the remainder. Currently, the costs of the distribution division are not allocated to the LOBs, but LOBs do pay the cost for any special rush shipment using an overnight or fast delivery service, such as Federal Express or UPS. For example, if a customer must have overnight delivery, the LOB ships directly without using Telstar's distribution center and the LOB is charged for the special delivery.

The corporate controller is mulling over the issue of allocating the costs of distribution. Several allocation schemes are possible:

1. Allocate all distribution division costs based on gross sales of the LOBs.

2. Allocate all distribution division costs based on LOB profits.

3. Allocate the direct costs of each shipment (driver, fuel, truck depreciation, tolls) using the gross weight of each LOB's product in the shipment. Then allocate the other costs of the distribution division (schedulers, management, telephones, etc.) using the total direct shipping costs assigned to each LOB.

One argument against allocating is that it will distort relative profitability. The controller says, "Because allocations are arbitrary, the resulting LOB profitabilities become arbitrary." Another argument is that it is not fair to charge managers for costs they cannot control. LOBs cannot control shipping costs. For example, there are savings when two small separate shipments are combined into a single large shipment. LOBs will tend to avoid opening up new sales territories when other Telstar products are not being shipped to that area.

Required:

Write a memo addressing the controller's concerns. Should Telstar begin allocating distribution costs to the LOBs? If so, which allocation scheme should it use?

King Khan Corporation (KKC) manufactures kongs and kangs, the production of which requires considerable energy. Power generation department costs amounted to $4 million this month, for a total of 50 million kilowatt hours (kwh) supplied to the plant. Analysis shows that 40% of power generation costs are fixed. This month the Kang Dept. made 5 million kangs, each using 4 kwh, and the Kang Dept. made 4 million kangs, each using 6 kwh. In the following month, the power generation department costs amounted to $4.3 million for 51 million kwh. Kong Dept.'s usage was the same, but the Kang Dept. increased output to 4.1 million kangs, each using the standard power allowance. If KKC employs an insulating cost allocation mechanism, and fixed costs are shared equally, which is true?

A lawyer allocates overhead costs based on his hours working with different clients. The lawyer expects to have $200,000 in overhead during the year and expects to work on clients' cases 2,000 hours during the year. In addition, she wants to pay herself $50 per hour for working with clients. In other words, the lawyer's billing rate is the sum of her hourly fee ($50) and a fee to recover the expected overhead spread over 2,000 hours. The lawyer, however, does not bill all of her clients based on covering overhead costs and her own salary. Some clients pay her on contingency fees. If the lawyer works with a client on a contingency fee basis, the lawyer receives half of any settlement for her client. During the year the lawyer works 1,200 hours that are billable to clients. The remaining hours are worked on a contingency basis. The lawyer wins $300,000 in settlements for his clients of which she receives half. Actual overhead was $210,000.

Required:

What does the lawyer earn during the year after expenses?

King Khan Corporation (KKC) manufactures kongs and kangs, the production of which requires considerable energy. Power generation department costs amounted to $4 million this month, for a total of 50 million kilowatt hours (kwh) supplied to the plant. Analysis shows that 40% of power generation costs are fixed. This month the Kang Dept. made 5 million kangs, each using 4 kwh, and the Kang Dept. made 4 million kangs, each using 6 kwh. If KKC uses the simplest algorithm to allocate power costs, which is not true?

Which is not a reason for allocating internal costs to cost objects?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)