Exam 11: Differential Analysis: The Key to Decision Making

Exam 1: Managerial Accounting and Cost Concepts166 Questions

Exam 2: Job-Order Costing154 Questions

Exam 3: Process Costing109 Questions

Exam 4: Cost-Volume-Profit Relationships241 Questions

Exam 5: Variable Costing and Segment Reporting: Tools for Management200 Questions

Exam 6: Activity-Based Costing: a Tool to Aid Decision Making138 Questions

Exam 7: Profit Planning106 Questions

Exam 8: Flexible Budgets and Performance Analysis295 Questions

Exam 9: Standard Costs and Variances178 Questions

Exam 10: Performance Measurement in Decentralized Organizations93 Questions

Exam 11: Differential Analysis: The Key to Decision Making153 Questions

Exam 12: Capital Budgeting Decisions144 Questions

Exam 13: Statement of Cash Flows108 Questions

Exam 14: Financial Statement Analysis211 Questions

Exam 15: Least-Squares Regression Computations22 Questions

Exam 16: Appendix B: Cost of Quality42 Questions

Exam 17: The Predetermined Overhead Rate and Capacity27 Questions

Exam 18: Further Classification of Labor Costs20 Questions

Exam 19: Fifo Method79 Questions

Exam 20: Service Department Allocations46 Questions

Exam 21: Abc Action Analysis15 Questions

Exam 22: Using a Modified Form of Activity-Based Costing to Determine Product Costs for External Reports16 Questions

Exam 23: Predetermined Overhead Rates and Overhead Analysis in a Standard Costing System105 Questions

Exam 24: Journal Entries to Record Variances52 Questions

Exam 25: Transfer Pricing21 Questions

Exam 26: Service Department Charges41 Questions

Exam 27: The Concept of Present Value12 Questions

Exam 28: Income Taxes in Capital Budgeting Decisions36 Questions

Exam 29: The Direct Method of Determining the Net Cash Provided by Operating Activities48 Questions

Exam 30: Pricing Products and Services67 Questions

Exam 31: Profitability Analysis71 Questions

Select questions type

The book value of a machine,as shown on the balance sheet,is relevant in a decision concerning the replacement of that machine by another machine.

(True/False)

4.9/5  (43)

(43)

Costs which are always relevant in decision making are those costs which are:

(Multiple Choice)

4.7/5 (43)

Marrin Corporation makes three products that use the current constraint-a particular type of machine. Data concerning those products appear below:  -Rank the products in order of their current profitability from most profitable to least profitable.In other words,rank the products in the order in which they should be emphasized.

-Rank the products in order of their current profitability from most profitable to least profitable.In other words,rank the products in the order in which they should be emphasized.

(Multiple Choice)

4.8/5 (35)

Schemm Inc.regularly uses material F04E and currently has in stock 460 liters of the material for which it paid $2,622 several weeks ago.If this were to be sold as is on the open market as surplus material,it would fetch $5.25 per liter.New stocks of the material can be purchased on the open market for $5.85 per liter,but it must be purchased in lots of 1,000 liters.You have been asked to determine the relevant cost of 800 liters of the material to be used in a job for a customer.The relevant cost of the 800 liters of material F04E is:

(Multiple Choice)

4.8/5 (41)

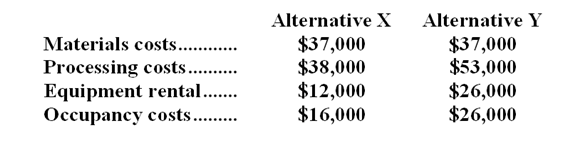

Two alternatives, code-named X and Y, are under consideration at Afalava Corporation. Costs associated with the alternatives are listed below.  -What is the differential cost of Alternative Y over Alternative X,including all of the relevant costs?

-What is the differential cost of Alternative Y over Alternative X,including all of the relevant costs?

(Multiple Choice)

4.8/5 (38)

The constraint at Dalbey Corporation is time on a particular machine. The company makes three products that use this machine. Data concerning those products appear below:  -Rank the products in order of their current profitability from most profitable to least profitable.In other words,rank the products in the order in which they should be emphasized.

-Rank the products in order of their current profitability from most profitable to least profitable.In other words,rank the products in the order in which they should be emphasized.

(Multiple Choice)

4.7/5 (39)

Beilke Corporation processes sugar beets in batches that it purchases from farmers for $53 a batch.A batch of sugar beets costs $12 to crush in the company's plant.Two intermediate products,beet fiber and beet juice,emerge from the crushing process.The beet fiber can be sold as is for $20 or processed further for $10 to make the end product industrial fiber that is sold for $26.The beet juice can be sold as is for $30 or processed further for $29 to make the end product refined sugar that is sold for $79.Which of the intermediate products should be processed further?

(Multiple Choice)

4.9/5 (31)

If by dropping a product a firm can avoid more in fixed costs than it loses in contribution margin,then the firm is better off economically if the product is dropped.

(True/False)

4.8/5 (37)

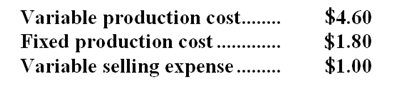

The Immanuel Company has just obtained a request for a special order of 6,000 jigs to be shipped at the end of the month at a selling price of $7 each. The company has a production capacity of 90,000 jigs per month with total fixed production costs of $144,000. At present, the company is selling 80,000 jigs per month through regular channels at a selling price of $11 each. For these regular sales, the cost for one jig is:  If the special order is accepted, Immanuel will not incur any selling expense; however, it will incur shipping costs of $0.30 per unit. Total fixed production cost would not be affected by this order.

-Suppose that regular sales of jigs total 85,000 units per month.All other conditions remain the same.If Immanuel accepts the special order,the change in monthly net operating income will be:

If the special order is accepted, Immanuel will not incur any selling expense; however, it will incur shipping costs of $0.30 per unit. Total fixed production cost would not be affected by this order.

-Suppose that regular sales of jigs total 85,000 units per month.All other conditions remain the same.If Immanuel accepts the special order,the change in monthly net operating income will be:

(Multiple Choice)

4.8/5 (33)

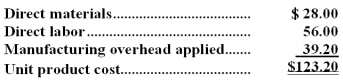

Bady Inc.makes a range of products.The company's predetermined overhead rate is $14 per direct labor-hour,which was calculated using the following budgeted data:  Component M3 is used in one of the company's products.The unit cost of the component according to the company's cost accounting system is determined as follows:

Component M3 is used in one of the company's products.The unit cost of the component according to the company's cost accounting system is determined as follows:  An outside supplier has offered to supply component M3 for $108 each.The outside supplier is known for quality and reliability.Assume that direct labor is a variable cost,variable manufacturing overhead is really driven by direct labor-hours,and total fixed manufacturing overhead would not be affected by this decision.Bady chronically has idle capacity.

Required:

Is the offer from the outside supplier financially attractive? Why?

An outside supplier has offered to supply component M3 for $108 each.The outside supplier is known for quality and reliability.Assume that direct labor is a variable cost,variable manufacturing overhead is really driven by direct labor-hours,and total fixed manufacturing overhead would not be affected by this decision.Bady chronically has idle capacity.

Required:

Is the offer from the outside supplier financially attractive? Why?

(Essay)

4.9/5 (30)

Payne Company makes two products, M and N, in a joint process. At the split-off point, 40,000 units of M and 50,000 units of N are available each month. Monthly joint production costs are $270,000.

Product M can be sold at the split-off point for $4.20 per unit. Product N can either be sold at the split-off point for $3.20 per unit or it can be processed further and sold for $6.30 per unit. If N is processed further, additional processing costs of $2.50 per unit will be incurred.

-What would the selling price per unit of product N need to be after further processing in order for Payne Company to be economically indifferent between selling N at the split-off point or processing N further?

(Multiple Choice)

4.9/5 (29)

Lampshire Inc.is considering using stocks of an old raw material in a special project.The special project would require all 160 kilograms of the raw material that are in stock and that originally cost the company $1,136 in total.If the company were to buy new supplies of this raw material on the open market,it would cost $7.25 per kilogram.However,the company has no other use for this raw material and would sell it at the discounted price of $6.50 per kilogram if it were not used in the special project.The sale of the raw material would involve delivery to the purchaser at a total cost of $75 for all 160 kilograms.What is the relevant cost of the 160 kilograms of the raw material when deciding whether to proceed with the special project?

(Multiple Choice)

4.7/5 (40)

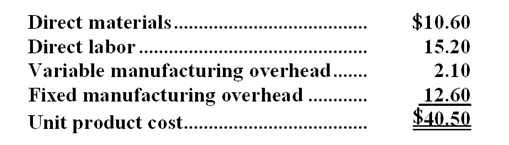

Ahsan Company makes 60,000 units per year of a part it uses in the products it manufactures. The unit product cost of this part is computed as follows:  An outside supplier has offered to sell the company all of these parts it needs for $45.70 a unit. If the company accepts this offer, the facilities now being used to make the part could be used to make more units of a product that is in high demand. The additional contribution margin on this other product would be $318,000 per year.

If the part were purchased from the outside supplier, all of the direct labor cost of the part would be avoided. However, $3.50 of the fixed manufacturing overhead cost being applied to the part would continue even if the part were purchased from the outside supplier. This fixed manufacturing overhead cost would be applied to the company's remaining products.

-How much of the unit product cost of $40.50 is relevant in the decision of whether to make or buy the part?

An outside supplier has offered to sell the company all of these parts it needs for $45.70 a unit. If the company accepts this offer, the facilities now being used to make the part could be used to make more units of a product that is in high demand. The additional contribution margin on this other product would be $318,000 per year.

If the part were purchased from the outside supplier, all of the direct labor cost of the part would be avoided. However, $3.50 of the fixed manufacturing overhead cost being applied to the part would continue even if the part were purchased from the outside supplier. This fixed manufacturing overhead cost would be applied to the company's remaining products.

-How much of the unit product cost of $40.50 is relevant in the decision of whether to make or buy the part?

(Multiple Choice)

4.8/5 (53)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)