Exam 6: The Supply Curve and the Behavior of Firms

Exam 1: The Central Idea154 Questions

Exam 2: Observing and Explaining the Economy107 Questions

Exam 3: The Supply and Demand Model170 Questions

Exam 4: Subtleties of the Supply and Demand Model: Price Floors,price Ceilings,and Elasticity181 Questions

Exam 5: The Demand Curve and the Behavior of Consumers136 Questions

Exam 6: The Supply Curve and the Behavior of Firms182 Questions

Exam 7: The Interaction of People in Markets158 Questions

Exam 8: Costs and the Changes at Firms Over Time172 Questions

Exam 9: The Rise and Fall of Industries139 Questions

Exam 10: Monopoly183 Questions

Exam 11: Product Differentiation, monopolistic Competition, and Oligopoly169 Questions

Exam 12: Antitrust Policy and Regulation152 Questions

Exam 13: Labor Markets179 Questions

Exam 14: Taxes, transfers, and Income Distribution180 Questions

Exam 15: Public Goods, externalities, and Government Behavior198 Questions

Exam 16: Capital and Financial Markets173 Questions

Exam 17: Macroeconomics: the Big Picture152 Questions

Exam 18: Measuring the Production, income, and Spending of Nations160 Questions

Exam 19: The Spending Allocation Model168 Questions

Exam 20: Unemployment and Employment207 Questions

Exam 21: Productivity and Economic Growth158 Questions

Exam 22: Money and Inflation149 Questions

Exam 23: The Nature and Causes of Economic Fluctuations162 Questions

Exam 24: The Economic Fluctuations Model207 Questions

Exam 25: Using the Economic Fluctuations Model177 Questions

Exam 26: Fiscal Policy137 Questions

Exam 27: Monetary Policy168 Questions

Exam 28: Economic Growth and Globalization162 Questions

Exam 29: International Trade248 Questions

Exam 30: International Finance123 Questions

Exam 31: Reading,understanding,and Creating Graphs34 Questions

Exam 32: Consumer Theory With Indifference Curves39 Questions

Exam 33: Producer Theory With Isoquants19 Questions

Exam 34: Present Discounted Value16 Questions

Exam 35: The Miracle of Compound Growth11 Questions

Exam 36:Deriving the Growth Accounting Formula13 Questions

Exam 37: Deriving the Formula for the Keynesian Multiplier and the Forward-Looking Consumption Model28 Questions

Select questions type

Where does producer surplus get its name? That is,why do economists call it a surplus?

(Essay)

4.8/5  (38)

(38)

The approach based on the relationship between price and marginal cost brings about the same supply curve as what is implied by the approach based on profit maximization.

(True/False)

4.9/5 (40)

What is the profit-maximization rule? Explain why profit is maximized when the rule is met.

(Essay)

4.8/5 (42)

If marginal cost increases,then the market supply curve shifts to the left.

(True/False)

4.8/5 (35)

If the marginal cost curves of all the firms in an industry are horizontally summed,one obtains

(Multiple Choice)

4.8/5 (38)

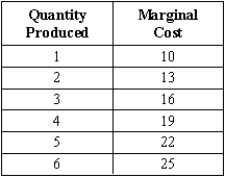

Exhibit 6-7  -Refer to Exhibit 6-7.If market price is $18,producer surplus for the profit-maximizing firm is

-Refer to Exhibit 6-7.If market price is $18,producer surplus for the profit-maximizing firm is

(Multiple Choice)

4.9/5 (37)

Partnerships differ from sole proprietorships because partnerships

(Multiple Choice)

4.8/5 (40)

Draw a graph of total revenue and total cost for a competitive firm that is maximizing profit but just breaking even.Mark the profit-maximizing output level.

(Essay)

4.8/5 (30)

Producer surplus is just an economist's technical name for profit.

(True/False)

4.9/5 (32)

Profit maximization is the basic assumption for all types of corporations,but not for sole proprietorships.

(True/False)

4.9/5 (29)

If the market wage increases,marginal cost shifts ____ and market supply ____.

(Multiple Choice)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)